- GBP/AUD is looking more bullish

- Lines up a move above key tech line

- UK inflation, RBA rate decision in focus

- But it will be global sentiment that ultimately determines trade

Image © Adobe Images

It's time for the Pound to break into the air above 2.08.

The coming week will be an interesting one for both the UK and Australia, with an interest rate decision due from the Reserve Bank of Australia (RBA) and inflation figures and PMI survey results to be released by the UK.

With some decent calendar action on tap, there is a genuine chance that idiosyncratic developments unique to the GBP/AUD can drive some volatility.

And volatility will surely be welcome for a Pound to Australian Dollar exchange rate (GBP/AUD) that hasn't offered much excitement of late.

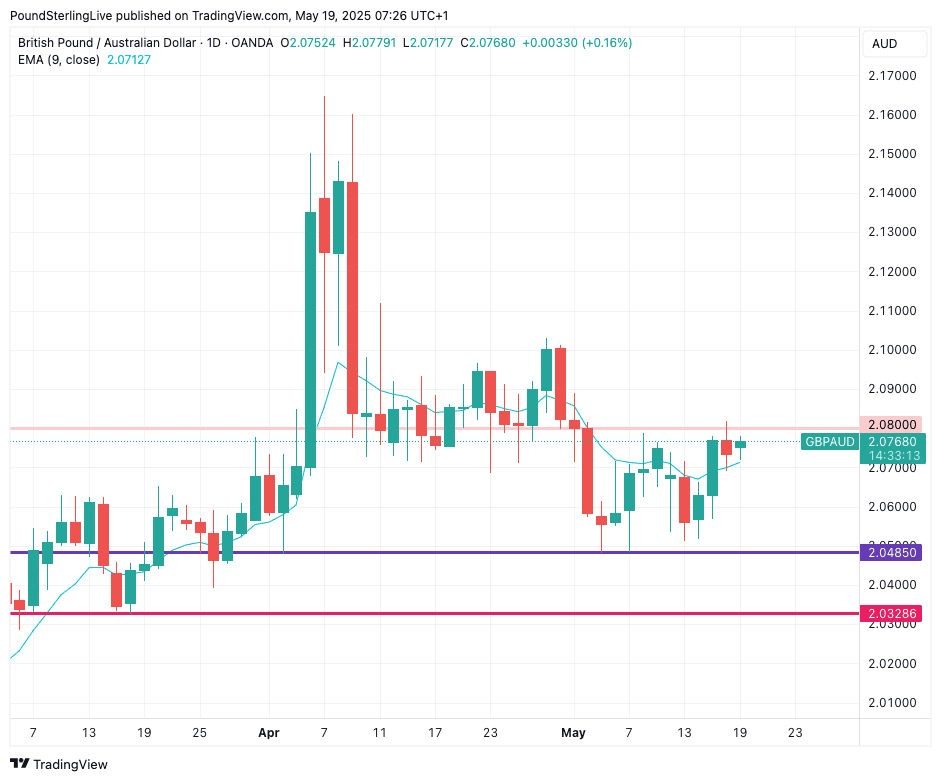

Above: GBP/AUD at daily intervals.

As the chart shows, GBP/AUD has spent May confined between 2.08 and 2.0480. Last week saw momentum return to GBP, and the pair has since pushed above the nine-day exponential moving average (EMA), located at 2.0711 at the time of writing. This is the turquoise line in the chart.

As a rule of thumb, our Week Ahead Forecast model says that when above this short-term momentum indicator, trade will remain constructive.

With this rule in mind, we forecast another test of 2.08 ahead of a move towards the upper end of the April consolidation at 2.10. For now, we think progress will be slow, so don't set any ambitious targets on a one- to two-week timeframe.

Turning to the calendar, Tuesday's RBA decision is the obvious Aussie highlight of the week, and a 25 basis point interest rate cut is well embedded in the price of GBP. This means the decision to cut won't in itself bother GBP/AUD.

However, the guidance will matter, and we are hearing suggestions that we will get a 'hawkish' cut. What this means is that the RBA will cut and warn it is not minded to cut again anytime soon, disappointing those wanting cheaper borrowing rates.

However, for AUD, this would provide a decent boost, as it would shore up Australia's interest rates relative to elsewhere, creating an appeal for international investors.

With interest rate differentials being a key driver of FX, any such outcome would boost AUD and frustrate GBP/AUD, which could pull back into the May range that is etched onto the above chart.

"There remains a solid positive impulse to underlying inflation. So while the fall in inflation will allow the RBA to cut rates next week, it will be a hawkish cut," says David Forrester, Senior FX Strategist at Crédit Agricole.

UK Inflation, PMIs

On Wednesday, UK inflation is released, and this should provide a catalyst for gains by the Pound.

The market consensus forecast is that prices surged 1.1% month-on-month in April, launching the annual rate far beyond the Bank of England's 2.0% target to 3.3%.

The Bank cut interest rates in early May, arguing that this surge in inflation is merely temporary and inflation will fall below target in the near future. But the market will be scouring the report's details for any signal that this evergreen optimism displayed by the Bank of England is unfounded and that the ingredients for embedded above-target inflation dynamics litter the finer details.

Image © Adobe Images

If elements of the report, such as services inflation, make for uncomfortable reading, then the higher-for-longer UK interest rate theme will remain intact, helping Pound Sterling extend recent gains.

However, any undershoot in the figures would likely prompt markets to bet that the Bank of England's optimism is well placed, and that they might soon signal they can accelerate the rate cutting process in the coming months.

This outcome would weigh on the Pound.

The Pound has shown a weak reaction function to domestic data of late, and it would take an eye-opening surprise to really get the FX market's juices flowing and deliver some nice moves in the Pound.

Perhaps PMI data for May, due out the following day, will be the bigger event.

After all, it is the market's go-to snapshot for immediate data that can tell us how an economy is responding to recent events.

These PMI data will help investors interrogate the UK's significant employment tax and minimum wage hikes of April, as well as the impact fading tariff fears have had on the economy. It will also cover any sentiment response to the UK-U.S. trade agreement.

The PMI survey also offers a leading indicator of inflation, and could answer some of those questions markets will be searching for in the official figures released a day prior. Also remember that employment dynamics and price setting intentions will offer insights into future inflationary developments.

Global Drivers = Big GBP/AUD Upside Risks

Keep in mind there are growing anxieties about the U.S. debt dynamics, with the Republicans set to push through a major bill this week that will only cause the country's debt pile to continue growing.

Any downturn in stock markets that would result from concerns would weigh heavily on the Australian Dollar, which has a high sensitivity to global risk sentiment that is, in turn, highly dependent on what happens in U.S. stock markets.

Above: House Speaker Johnson (right) is to push through new spending plans that will grow the U.S. debt burden. DOD photo by U.S. Navy Petty Officer 1st Class Alexander Kubitza.

In fact, the RBA and UK domestic data will be a sideshow if we see any major sentiment shifts in global investor sentiment, meaning it is the global picture that will ultimately determine where GBP/AUD trades.

Moody's lowered its U.S. debt rating after markets closed last week, cutting it one notch to Aa1 from Aaa, while its outlook was changed to stable from negative. Fitch and S&P, the other main agencies, had previously removed the US’s pristine rating.

The U.S. has significant 'twin deficits', i.e. a spending deficit and a trade deficit, both of which are interlinked.

Despite burgeoning debt, the Republicans are this week looking to pass a bill that will embed 2017's tax cuts, while offering little by way of meaningful spending cuts.

This means the U.S. debt burden is set to grow, and there are whispers that a market that is more sceptical about the U.S. in the Trump era might be less willing to fund this spending by buying U.S. debt (bonds).

Markets are focusing on the issue this week as the Republicans attempt to get their budget bill through Congress, and any market wobbles around the U.S. debt situation would first be evident in U.S. Treasury yield dynamics.

From here, they would spill into stock markets and FX. It's a low-burn concern for now, but if it does become a problem, it will become a problem in a big way, and for AUD this is unhelpful.