Image © Adobe Stock

The Pound will come out of today's Bank of England relatively unscathed.

The Bank of England's policy decision will be closely watched on Thursday, where interest rates will be left unchanged, but policymakers will keep the door open to the next cut coming in August.

We don't expect a significant amount of movement from the June update, as the decision and narrow guidance pathway are already well understood by the market, leaving the geopolitical sphere as the most pressing issue for now.

"Data has surprised to the downside since the past meeting, with the job market showing more pronounced signs of cooling. We think this will support the notion of further quarterly cuts," says Frederik Romedahl, Chief Analyst for FI research at Danske Bank.

The Pound has softened over the course of the past ten days owing to a labour market report that pointed to increased levels of joblessness as the Labour Party's policies start to bite. Also, monthly GDP data released last week showed an unexpectedly large slowdown.

"This could be one of the more interesting ‘pause’ meetings in the cycle after recent data showed a shift toward softer labour market conditions and weaker growth momentum," says Henry Cook, analyst at MUFG. "Recent domestic data has opened the door to some subtle shifts in messaging after a somewhat hawkish tone last time out. The vote split may also reflect greater confidence in the underlying disinflation process."

This week's inflation data, meanwhile, offered no massive surprises, which suggested the Bank can still bring inflation back down to 2.0% at some point next year on its current trajectory.

That trajectory involves the Bank cutting rates once every quarter, putting the August decision in play.

Ahead of the run of weak data prints, the market had given up hope for an August cut, judging the economy to be too robust and noting inflation continues to rise.

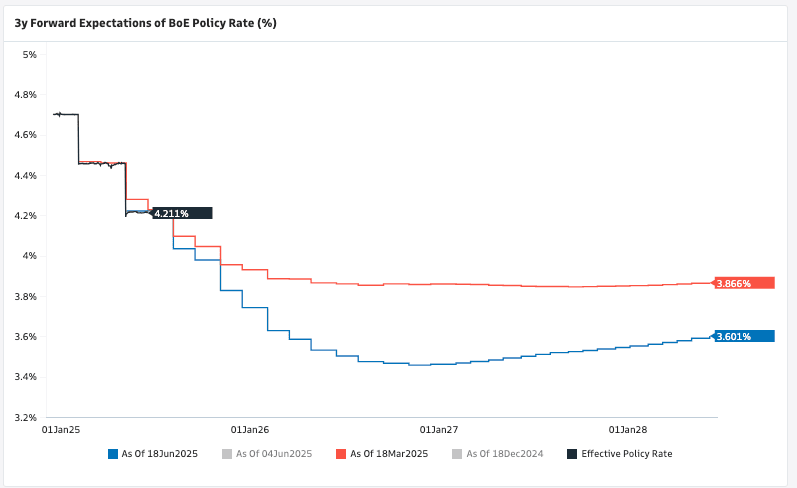

Above: Markets have moved to anticipate deeper cuts since March, stemming GBP outperformance.

However, a repricing in favour of an August move has weighed heavily on the Pound. GBP/EUR has extended its decline to 1.1691, and the Pound to Dollar exchange rate is lower at 1.3392, having been as high as 1.3620 at the close of last week.

Danske Bank expects a muted market reaction to the Bank of England, expecting it to refrain from altering its current guidance.

"More broadly, we stay negative on GBP targeting a move higher towards 0.87 on a 6-12-month horizon," says Romedahl

An initial signal to markets will come from the composition of the vote for the rate cut, with the rule of thumb being that the larger the vote for a cut, the higher the likelihood of the cut being realised at the next meeting.

"If the MPC votes 6-3 to leave rates on hold with three dissents in favour of a another cut it should provide a trigger for the GBP to weaken further. However, the scale of GBP sell-off would be curtailed if there is no significant change in tone or guidance," explains Lee Hardman, FX analyst at MUFG.

However, Andrew Wishart, an economist at Berenberg, thinks the Bank of England simply cannot avoid the rise in inflation that is underway, which will curtail the Bank's desire to cut interest rates.

He says the Bank is now on pause until 2026.

"We expect cost-push inflation to force the BoE to keep Bank Rate at 4.25% until the end of the year. Healthy household finances, increasing real incomes and rising government expenditures will ensure that domestic spending growth remains robust so that companies can pass on the large increase in their costs to customers in the form of higher prices," says Wishart.

If this assessment is correct, then an ample repricing in interest rate expectations awaits, which could turn the tide on GBP weakness.