President Christine Lagarde and Vice President Luis de Guindos present the latest monetary policy decisions and answer questions from journalists, Frankfurt, 24 July 2025. Image copyright ECB.

Euro will benefit from the ECB's policy stance.

'Long' positioning in the Euro is being washed out of the system following the sealing of a new EU-U.S. trade accord, but a host of analysts say the currency's spell of weakness should be a temporary state of affairs.

This is because the market will switch focus from trade wars to interest rate dynamics, ensuring the European Central Bank (ECB) will become a source of support for the currency over the remainder of this year.

"With the EU and U.S. having reached a trade deal, there is less reason for the ECB to cut policy rates further, especially with the economy proving more resilient this year and monetary transmission working effectively," says Mark Wall, Chief Economist at Deutsche Bank. "Further easing is now a risk scenario rather than baseline, and arguably a greater risk in December/March than in September."

The Euro has outperformed the Dollar and other peer currencies amidst the heightened trade tensions of 2025; U.S. President Donald Trump's reset of U.S. trade relationships rightly captured investor attention, allowing FX markets to veer away from traditional drivers.

One of those traditional drivers is interest rate differentials, which have not traditionally favoured the Euro as the ECB has been quick to cut interest rates in the current cycle.

But, this is changing: the ECB's recent decision to hold interest rates suggests the Eurozone's central bank is about to end the cutting cycle ahead of the Bank of England and Federal Reserve.

"At its July meeting, ECB President Christine Lagarde effectively indicated a pause ahead, while hinting that the council may even be done cutting rates altogether," says Matthew Ryan, Head of Market Strategy at Ebury.

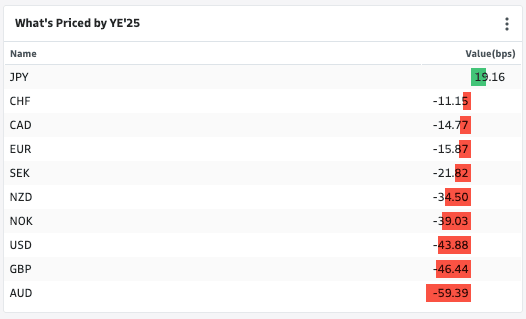

Above: Scale of further interest rate cuts still to come, suggesting 50/50 odds the ECB is done.

This should steady Eurozone interest rates relative to those in the UK and U.S., to the benefit of the Euro.

Nomura's strategists have been buyers of the Euro against the Pound since early June, on ongoing monetary policy divergence and fiscal issues, "but the scale of the change in tone was surprising," says Nomura FX Strategist Dominic Bunning of the ECB's July guidance.

"With market pricing still implying close to one further cut this cycle, there should be more rates driven upside for the EUR. As a follow up to this we raise our target to 0.8975 – aligned with the highs seen in early 2023," he adds.

EUR/GBP at 0.8975 gives a GBP/EUR target of 1.1140.

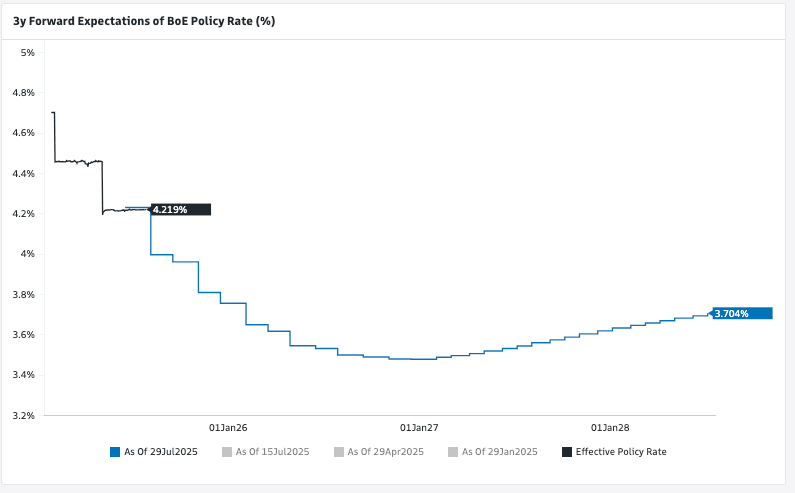

Money market pricing shows the Bank of England is expected to cut interest rates on three more occasions, twice more in 2025 and once more in 2026. This represents a 75 basis point curve of cuts, which is similar to the pricing for the Federal Reserve.

"We maintain our bullish EUR/USD thesis – a hawkish ECB only further bolsters a robust case for EUR appreciation based on both US-RoW rate convergence as well as technical factors," says Morgan Stanley.

Above: Money market pricing shows the Bank of England will cut three more times to take the base rate to 3.5%. Image courtesy of Goldman Sachs.

Both are deeper than the mere 25 priced for the ECB. In fact, the market currently prices 15 basis points for the ECB over the remainder of the year, meaning a good portion of the market thinks the cycle is complete.

"The upshot is the trade deal defuses a major external downside risk to the Eurozone economy and reinforces the case for the ECB to stay on hold. The implication is there is room for the swaps curve to shift higher in favour of EUR," says Elias Haddad, Senior Markets Strategist at Brown Brothers Harriman.

He says the ECB’s pause, coupled with political pressure on the Fed to ease, offers EUR/USD support. "We see EUR/USD carving out a bottom around 1.1500." Beyond the near-term, Brown Brothers Harriman says the underlying EUR/USD uptrend is intact.

Risks to the bullish EUR view include deeper falls in Eurozone inflationary pressures than current ECB projections allow for.

Another is that the 15% tariffs agreed with the U.S. prove to be a bigger burden on European businesses than expected, culminating in a slowdown that prompts the ECB to deliver further cuts.

"Trade optimism is running high after a trade deal was struck between the US and EU over the weekend... But with markets already pricing a positive outcome, bouts of volatility remain possible," says Mark Haefele, Chief Investment Officer at UBS Global Wealth Management.