Image © Adobe Images

Pound Sterling risks further losses in the coming days.

The Pound to Euro exchange rate (GBP/EUR) is forecast to remain under pressure over the course of the next five days, although French politics and a European Central Bank policy decision could offer some volatility that challenges this view.

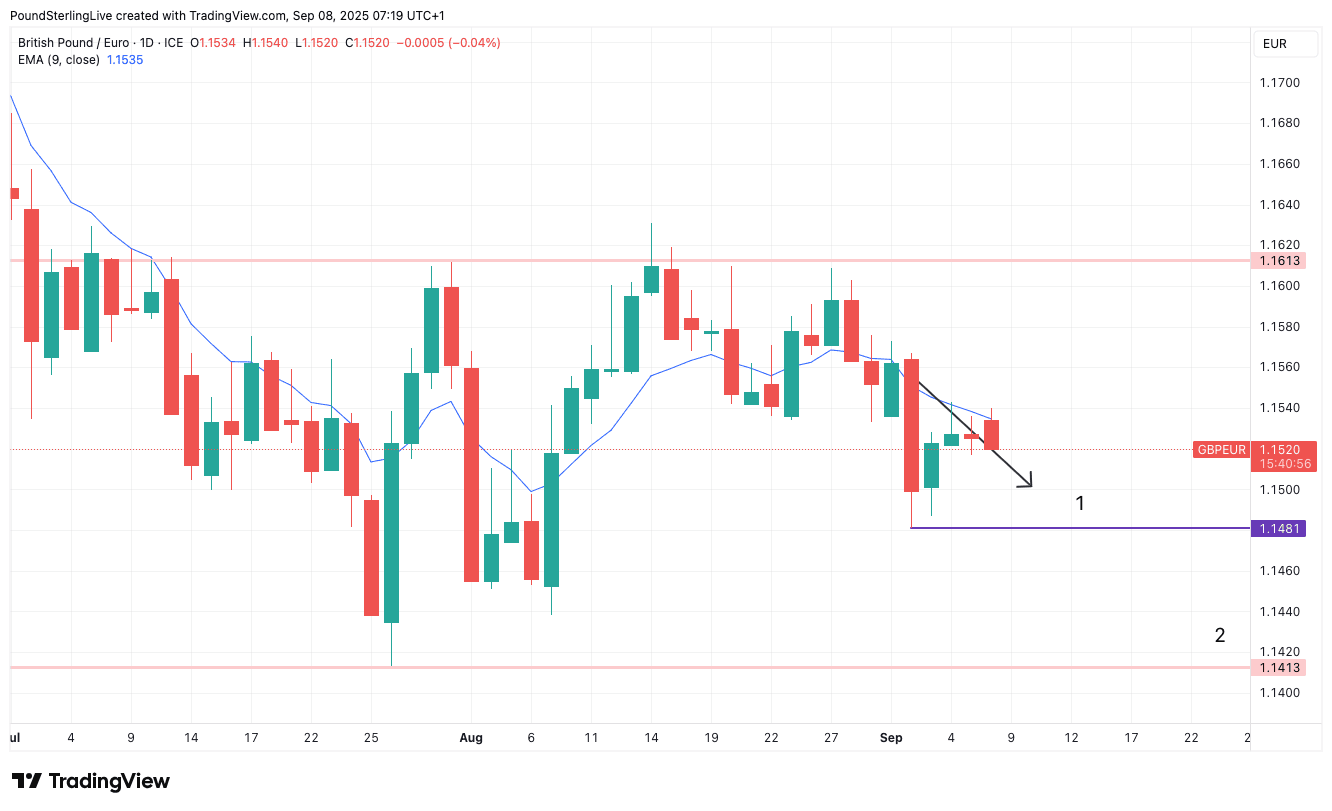

Last Monday's Week Ahead Forecast proved to be spot on, with the exchange rate declining to finish the week at 1.1525, and today we are inclined to stick with the annotations we made to the daily chart seven days ago in our new updated chart:

The chart shows the arrow annotation made last Monday, which is intended to give readers a sense of directionality and where potential targets might lie.

The implication of maintaining the previous week's view is that we think the market is still in this phase of weakness and there is nothing evident in the chart that would suggest the Pound is in a position to break off its shackles and rally.

As can be seen, GBP/EUR is stuck below the nine-day exponential moving average (EMA), which prompts our Week Ahead Forecast model to point lower, verifying the expectation for ongoing softness in GBP/EUR.

The first target on the chart, which is entirely reachable in the coming days, is at 1.1481, which is the low struck last Tuesday, when the Pound was sold heavily amidst an unexpected selloff in UK government bonds.

Beyond here are the range lows at 1.1413, which is a potential prospect for some point during the remainder of September. Those with imminent FX payments should consider locking in current rates for future use if a weaker GBP is not desirable, or contact our dealing desk to set an automatic order to ensure your ideal rate is not missed.

Although the charts tell a story of ongoing GBP/EUR softness, there is the potential for unexpected volatility in either direction as French politics and the ECB will have implications for EUR direction, while a UK GDP release offers up some excitement ahead of the weekend.

French MPs will debate a vote of no confidence in the country's current government, lead by Francois Bayrou, on Monday afternoon.

If the government loses, French President Emmanuel Macron will have to try and find the country's fifth prime minister in two years, or call another election.

France's latest bout of political instability has nevertheless had a limited impact on the euro, as markets know what to expect, thanks to the template provided by the Michel Barnier ouster of December.

This leaves investors relatively sanguine on the issue, anticipating that the country will find a solution and muddle through.

However, there is also scope for surprise, particularly if President Macron calls a new election and polling starts to throw up some unsavoury potential outcomes that lessen the chances of the country getting on top of its finances.

However, for now, this is a low-probability outcome.

File image of Francois Bayrou. Image: Jacques Paquier, licensed as CC BY 2.0.

Friday's UK GDP data is the highlight of the UK's domestic calendar, with an uninspiring 0% month-on-month print anticipated for July.

"We expect official figures to show the UK economy began Q3 with flat monthly growth in July, largely reflecting a reversal of June’s unexpectedly strong 0.4% rise," says a note from Lloyds Bank.

Manufacturing and industrial production data will also be released. "The bright spot is manufacturing, where output is expected to rise for a second month. June’s strength creates a statistical carry-over effect, supporting Q3 growth of around 0.2%q/q even if output remains flat in August and September," says Lloyds.

Ahead of Friday's UK print is Thursday's European Central Bank (ECB) decision, which will likely yield a decision to hold interest rates, confirming an end to the cutting cycle.

This should stabilise short-term European interest rates (bond yields), which will naturally underpin the Euro, particularly against currencies belonging to central banks that might be inclined to cut interest rates further.

There are risks that the Bank of England cuts interest rates again in November, ahead of further cuts next year, as the central bank responds to a deteriorating local labour market.

However, for now, it appears that the Bank is increasingly concerned about the trajectory of domestic inflation, with Governor Andrew Bailey telling lawmakers last week that there was less certainty that it could continue with its recent run rate of a cut a quarter.

This realisation has helped underpin short-term UK bond yields relative to those of Europe, which should ensure the pound retains some near-term support on the interest rate front.

Elswhere, the U.S. inflation print due on Thursday is the global highlight of the week. Here, an above-consensus print risks unsettling markets and prompting a strong USD rebound that could also weigh on GBP/EUR.

This is because GBP/EUR is sensitive to shifts in investor sentiment, tending to fall when market volatility rises.