Image © Adobe Images

Pound sterling under pressure as falling wages tee up interest rate cuts.

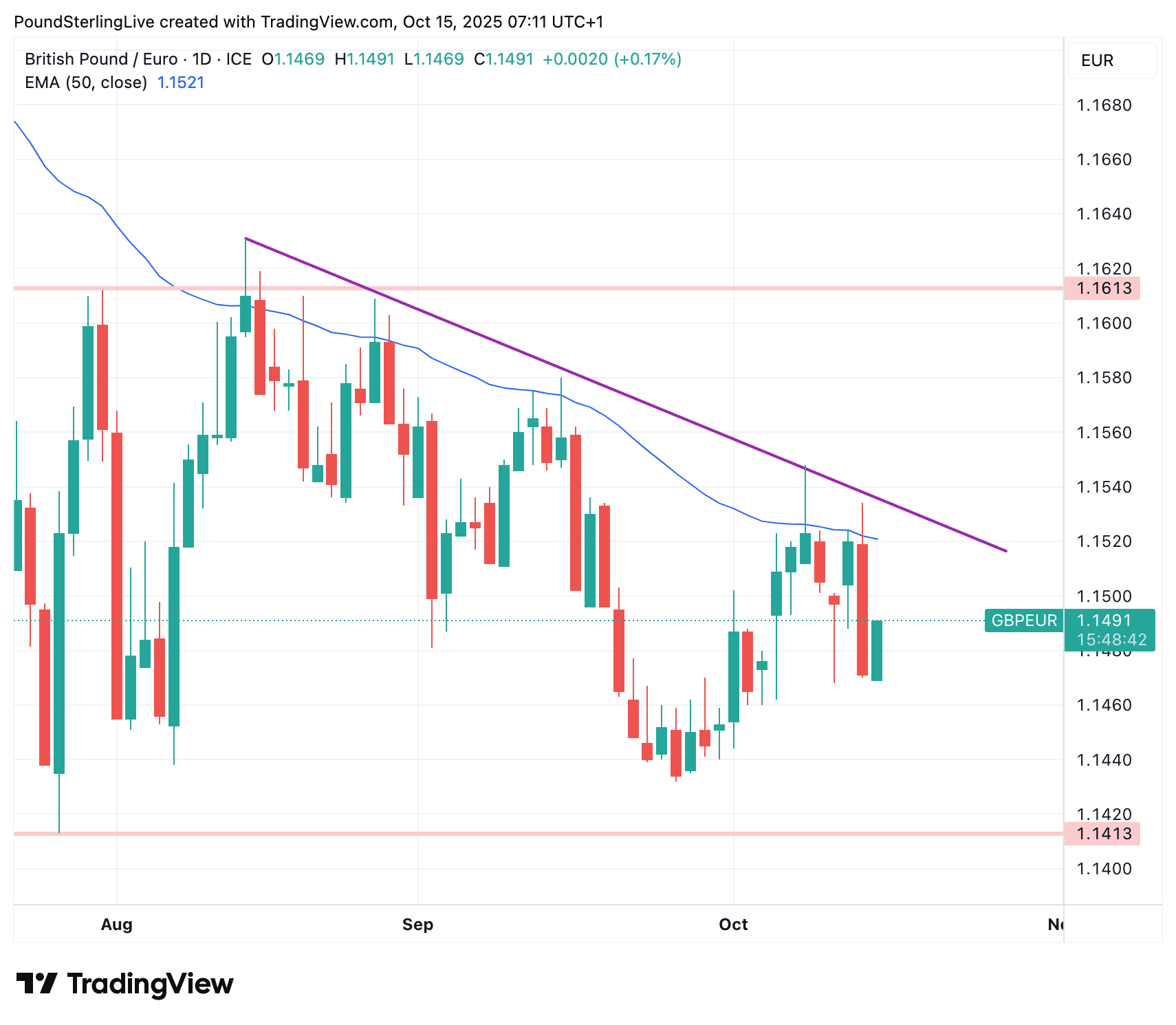

The pound to euro exchange rate (GBP/EUR) is 0.15% higher at the time of writing in midweek trade, suggesting some retracement of the previous day's declines is underway.

An 'up-day' is possible; however, there is nothing in the technical or fundamental setup that would suggest a major trend-turn is about to occur, and gains should be shallow.

This means a rise to 1.1520 today is unlikely; instead, some consolidation around 1.15 is possible ahead of a move to preferred targets over the coming days to the late September consolidation zone at 1.1440, ahead of September lows at 1.1414.

Those with payment requirements can lock in current rates ahead of a further slide, or discuss our industry-beating exchange rates with our dealing desk.

The chart shows a clear short-term downtrend is in place, the inevitable outcome of which is a fall to new cycle lows.

Capping gains is a downward-trending trendline (shown in purple), which captures the burnout levels of a number of spikes. The 50-day moving average is also prominent (blue line), above which the exchange rate does not close on a daily basis.

The downtrend was reinforced by the pound's 0.43% drop against the euro on Tuesday when it was revealed that UK unemployment was rising and wages were falling, and follow-on weakness is likely in the near term as investors inevitably raise the odds of a November interest rate cut.

At present, the market sees a less than 50% chance of a cut next month, however it is clear that the likelihood of a move is much closer to a 50-50 coin toss on account of entrenched positions on the Monetary Policy Committee. If the Bank doesn't cut in November, owing to the proximity of the budget, it will almost certainly cut in December,

Yesterday MPC Alan Taylor made it clear the Bank is already behind the curve when it comes to rate cuts and he seems to be in a hurry to lower rates. Pushing back is the Bank's Chief Economist, Huw Pill, who warned last week that inflation was still too high to cut rates.

In fact, there is a line running right down the middle of the MPC on the matter and the vote of Governor Andrew Bailey will carry the day in November and December. For his part, Bailey said in a speech Thursday he believes 'spare capacity' in the economy is opening up, which is just a fancy way of saying there is scope to cut interest rates without pushing inflation higher.

A cut became more likely after the UK on Tuesday reported 10k jobs were lost in September and, crucially, annual pay growth slid to 4.4% in August, down from 6% at the start of the year.

A better indication of the deceleration in wages is provided by the three-month annualised run rate, which shows private sector pay growth now sits at 2.4%.

The Bank of England will therefore feel more comfortable with the idea that wages will start to pull inflation lower over the coming months and some further monetary accommodation is therefore needed.

However, economists point out the Bank might want to wait the contents of the budget to judge how inflationary/dis-inflationary the government intends to be.

"December is in play, given that this meeting falls after the budget. And assuming we see further falls in wage growth, coupled with a bit of undershooting on the Bank’s services inflation forecasts, then a Christmas rate cut is possible," says James Smith, Developed Markets Economist at ING Bank.

The pound will fall further as markets adjust for a year-end rate cut and a number of follow-on cuts in early 2026. The currency will face additional headwinds from the November 26 budget, which promises to be a tax-hiking bonanza as the government scrambles for billions of pounds to cover unexpectedly high spending, debt repayments and disappointing productivity.