Image © Adobe Images

Pound sterling faces the Bank of England on Thursday.

Our headline view is pound sterling can rebound a little further in the near term as a consolidation of the recent selloff ensues.

The pound to euro exchange rate (GBP/EUR) fell 0.40% last week to plug its lowest level in two years, amidst rising odds of an interest rate cut at the Bank of England before the end of 2025.

The question of interest rates comes to a head on Thursday when the Bank delivers the final Monetary Policy Report (MPR) of the year.

The previous three MPRs have accompanied a rate cut, but this one could be different, as the Bank could opt to leave rates unchanged.

That would be supportive of pound sterling, all else equal. But, and here is the crucial point for readers to take away this Monday: if the Bank skips a cut this week, it'll almost certainly cut in December.

So what happens on Thursday isn't necessarily the game-changer it would appear to be at first sight, as the direction of travel points to one more cut before the year's end.

On this basis, we think the recent recalibration in interest rate expectations has already taken its toll on the pound and is why we see reduced downside risks into Thursday and enhanced relief-rally risks: the forward-looking marketplace has adjusted to what's coming and the pound is weaker as a result.

In fact, we wouldn't be surprised to see some buying happening ahead of the decision as a "buy the fact" mentality takes hold.

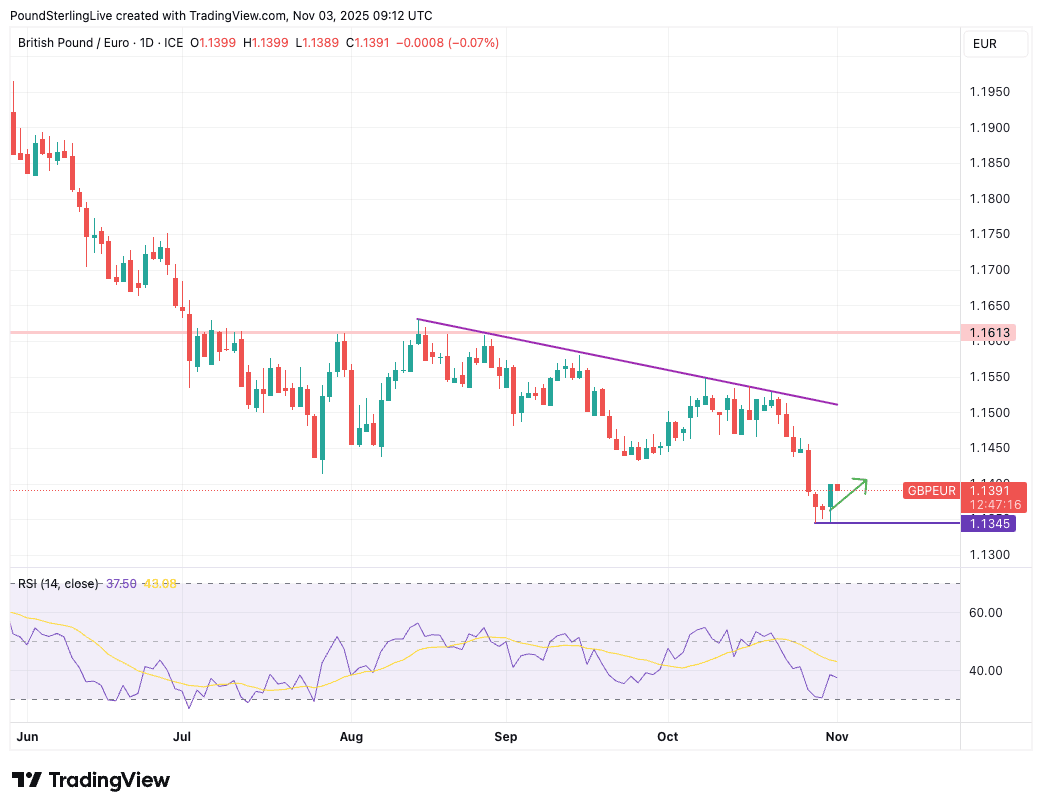

GBP/EUR reached oversold levels last week as it hit a low of 1.1345, first on Wednesday, then Thursday and then again on Friday. So as the chart suggests, this is a mini support zone:

The pace of losses left it looking oversold and we wrote Thursday that a rebound was required. We drew the green annotation on Thursday to suggest these levels were where the rebound would occur, and we're sticking with the view on Monday.

To be sure, momentum is still overwhelmingly in favour of further downside, which is why we think that gains from here will be shallow and more of a consolidative pattern than an outright recovery.

In this environment, 1.15 would be a reasonable tactical target.

Sterling strength should remain shallow owing to the two remaining high-impact Bank of England decisions remaining this year, and of course there remains the issue of the budget on November 26.

Talk of significant tax increases is stirring a pot of uncertainty amongst businesses and households, and as we used to say in the Brexit days, the pound hates nothing more than uncertainty.

When those tax increases are finally announced uncertainty will lift, and that could help propel the pound higher into year-end as 'short' positioning is unwound.

However, the steady uplift in taxes will squeeze the economy in the coming years, which reinforces the view that rallies are unlikely to be sustainable on a longer lasting basis.

"We stay negative on GBP," says a note from Danske Bank. "While a significant tightening of fiscal policy would alleviate some pressure in terms of the negative impact from unsustainable public finances, we highlight the negative growth impact."