Picture by Kirsty O'Connor / Treasury

There's a definite sense of nervousness amongst investors ahead of the weekend.

Pound sterling is selling off across the board on Friday, and this move will be linked to the spike in global bond yields.

Bond yields are rising for all countries, which effectively means the cost of government borrowing is on the move, but it's more acute for UK gilts, and that's what's bothering the pound.

"Long-term European and U.S. bond yields add up to 4 bps. During the second half of the week, focus turned from (discounted) central bank rate hikes to (inflation) risk premia and the sense that higher rates might stick for longer," says Mathias Van der Jeugt, economist at KBC Bank.

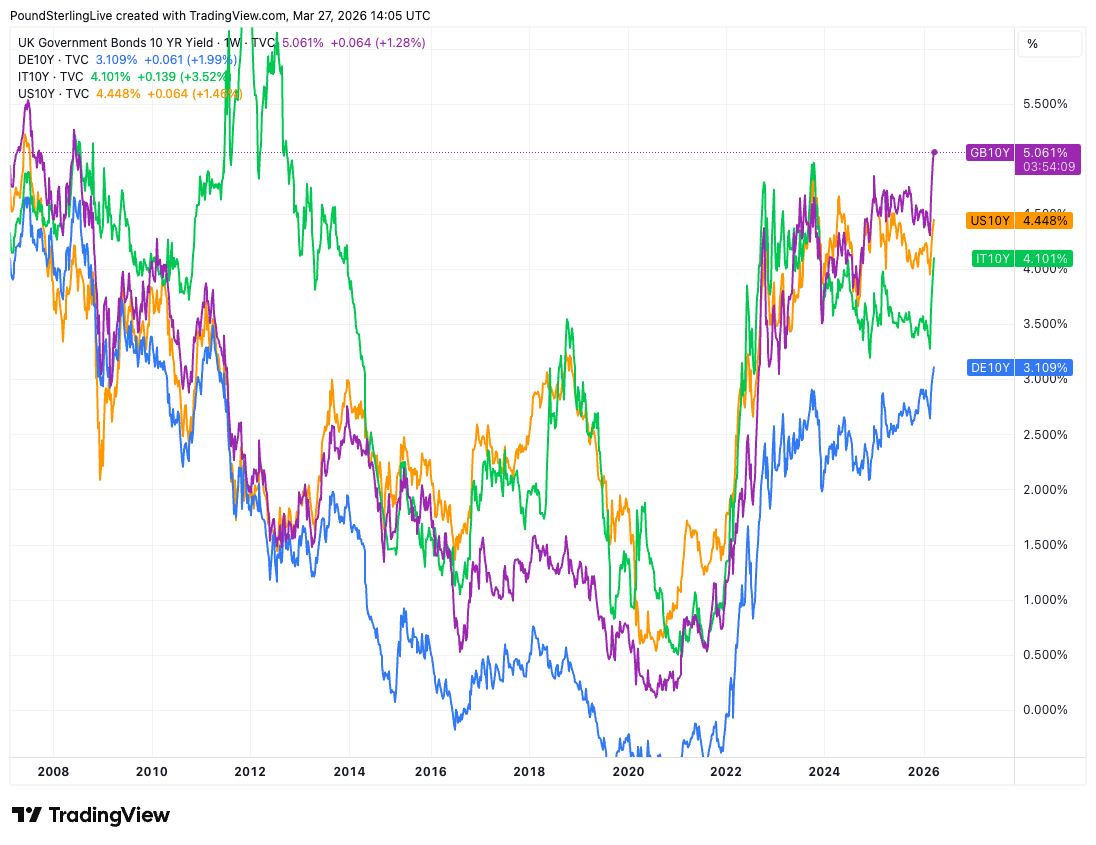

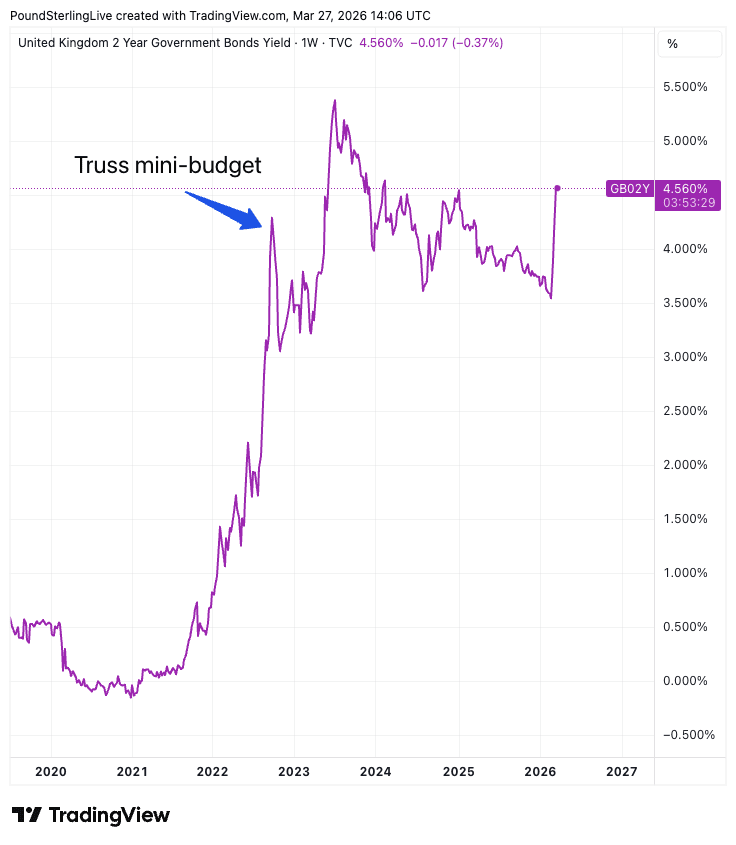

The UK ten-year gilt yield is up at 5.066% and on course to register its highest close since July 2008; the two-year gilt yield is at 4.53%, the highest since December.

Financial newswires say the uplift is due to concerns that a protracted war in Iran will keep oil prices elevated, fueling an increase in inflation and a slowdown in growth.

U.S. President Donald Trump has given Iran ten more days to make concessions or face an escalation, and markets are probably telling us that won't happen.

"A revised five-day deadline has been extended by ten more days. Trump appears to be stuck in a self-made bind with no off-ramp allowing him to claim a credible win. Negotiations are ongoing, but prospects for a near-term resolution remain limited," says Ulf Andersson, Chief Economist at DNB Carnegie.

The promise of higher inflation makes it less desirable to own government bonds as their coupon payments will inevitably be gobbled up by inflation, and as their price falls, their yield must rise.

Bonds are what governments issue to borrow money from the private markets and they hint at underlying assumptions about the issuing country.

The bad news for the pound is that markets are demanding more of a premium to hold British debt. Just look at this selection of ten-year bond yields: once it was Italy that was the concern, now it is the UK where the premium lies:

Above: Select ten-year bond yields, highlighting UK premium.

In good low-volatility times, rising bond yields tend to support a currency, and we would expect pound sterling exchange rates to march higher.

But when the backdrop is fraught, and anxieties build, the pound is at risk of international investors dumping their gilt holdings, creating outflows of currency.

Over the past two years, we have seen a number of occasions where gilts and the pound have fallen in tandem. The most famous episode was Liz Truss' mini budget, but we did see it last year when markets worried that Rachel Reeves would be replaced with a Labour Party left-winger.

Above: UK two-year bond yields.

In 2026, there have been a few similar episodes, but they have tended to fade quickly, and GBP/EUR and other GBP exchange rates managed to regain composure relatively quickly.

So, we could see sterling regain lost ground on Monday, particularly if there are some positive news headlines regarding the war to start the week.

However, if Trump finds he has no offramp, he might have little choice but to send in the troops to secure the Strait of Hormuz to guarantee safe passage of fuel tankers.

That escalation could prove messy for global markets, and the pound in particular.

"Hostilities continue unabated. The result is persistent uncertainty and elevated market volatility. The longer the Strait of Hormuz remains closed, the greater the disruption to global crude and LNG supply - pushing energy prices higher and amplifying inflationary pressures, initially in headline prints but increasingly feeding into core over time," says Andersson.

"Trump appears to be losing his grip on the markets. Investors no longer seem to take his statements at face value—if anything, they’re beginning to trade against them, waiting for tangible proof before reacting. That's an uncomfortable position for any policymaker to be in," says Fawad Razaqzada, Market Analyst at FOREX.com.