GBP/EUR's post-budget recovery is still, technically, alive. File image of Rachel Reeves. Picture by Simon Walker / HM Treasury.

Pound sterling is trending higher against the euro, albeit at a glacial pace.

Pound sterling rallies against the euro as survey data suggests the UK is weathering the Iran fallout better than the Eurozone.

The pound-euro exchange rate rose to 1.1550 on Thursday in the wake of the release of April survey data that pointed to a surprisingly strong recovery in Britain's private sector.

The composite flash PMI recovered to 52 in April from 49.8, with the services and manufacturing sectors pointing to solid growth (52 and 53.6, respectively).

By contrast, the Eurozone's composite read at 48.6, which means it slipped below the 50 level that marks the boundary between expansion and contraction. "April EMU PMI was as feared. The EMU economy is heading toward stagflation," says a note from KBC Bank in Brussels.

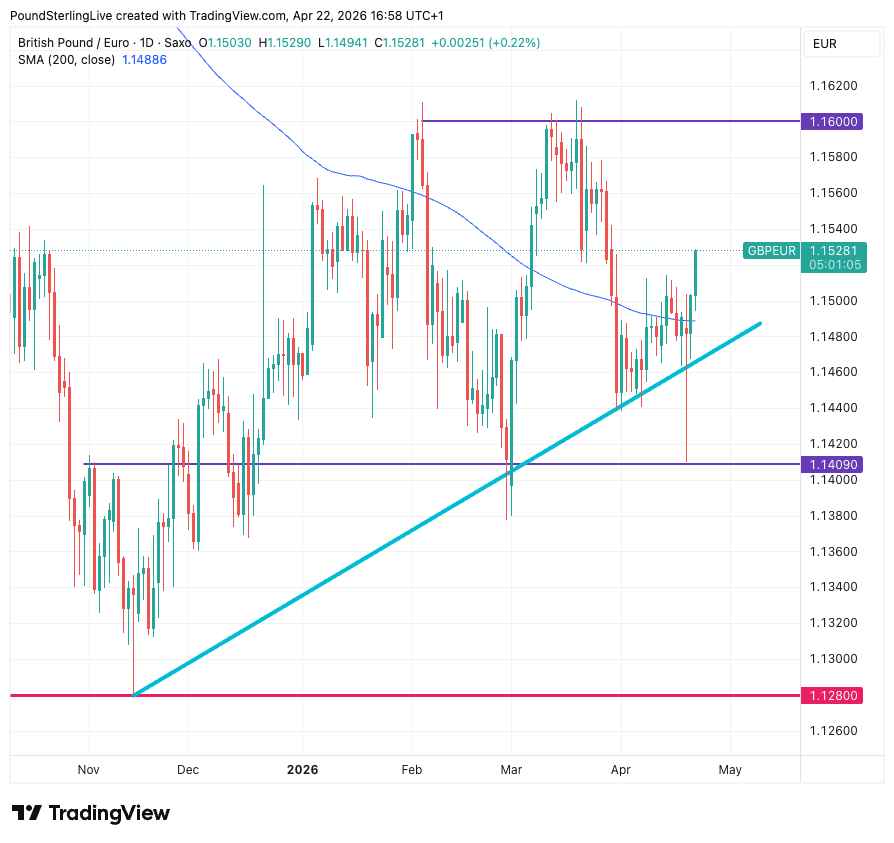

That divergent outcome was enough to send GBP/EUR to its highest level since March 27 at 1.1545.

This means money transfer rates at all-in zero-fee providers are close to 1.15 at these levels, and we encourage those with looming payments to benchmark their current provider against specialists to ensure they get optimal rates and service.

Above: The turquoise line denotes the broad outlines of an uptrend. Solid resistance lies ahead at 1.16.

Wednesday's advance to 1.1550 could be the start of a breakout phase from a sluggish period of consolidation and a continuation of a recovery trend that was initially triggered back in November when financial markets breathed a sigh of relief that Rachel Reeves' budget wasn't a train wreck.

The move stalled in February, while another attempt to restart the rally failed again in March, on both occasions at 1.16. The most recent pullback looks to have ended and if the trend truly is pound sterling's friend, GBP/EUR could be aiming for another retest of 1.16.

We would suggest those with payment requirements set orders to capture anything near here, as history has shown these levels don't tend to stick and only automated orders tend to be triggered.

"Overall we would be wary of chasing GBP higher purely on the headline beat, indeed we would prefer to fade the post data Cable bounce," says Jeremy Stretch, Chief International Strategist at CIBC Capital Markets.

Our survey of investment banks, out this week, meanwhile, shows anything near 1.16 would put it well above a consensus estimate that looks for it to trend slightly lower over the remainder of the year.

Helping the pound higher is a steady rise in UK bond yields, underpinned by Tuesday's above-consensus labour market data and Wednesday's +3% inflation print.

The inflation print was interesting in that it was solid, but it wasn't alarming, meaning it hit a sweet spot that supports bond yields while not scaring the market with stagflation vibes.

"UK job market conditions were updated and the outcome motivated a mild increase in expectations for cumulative policy tightening by the Bank of England this year. Year-end OIS meeting pricing for Bank Rate moved up by 8bps to one-and-a-half quarter point hikes and a couple of points of priced tightening was added for the June meeting which is now roughly 50-50," says Derek Holt, Head of Capital Markets Economics at Scotibank.

"The labour market was loosening only gradually before the war," says Robert Wood, UK Economist at Pantheon Macroeconomics. "Let's see how this develops, but we think the early signs on job growth are arguably a bit better than expected."

UK inflation read at 3.3 in March, meeting expectations. That's enough to ensure the Bank of England doesn't cut interest rates anytime soon, while also not signalling there's a need to rush into a rate hike, which would risk upsetting the economy.

The pound fell through 2025 as markets increasingly bet on Bank of England interest rates cuts, which were duly delivered. Should that phase of cutting be cut short, then GBP can find itself better supported.

Another risk event the pound was watching this week was Prime Minister Keir Starmer's grip on power, with the Mandelson affair threatening to topple him.

Markets are nervous of this as there's a good chance that a left-winger will replace him and engage frivilous spending plans.

But Starmer looks to have navigated the latest episode and is unlikely to leave anytime soon. That puts political risks on the back burner.

"The Prime Minister is facing calls to resign over Mandelson's appointment and ahead of local elections on May 7, but investors—and punters in prediction markets—see this as unlikely, with most expecting the current leadership to remain in place for now," says Karl Schamotta, analyst at Corpay.

With things going OK for pound sterling, its edging higher against the euro.