- Euro can benefit from investor rotation

- Bullishness on European growth and equities rises

- Financials top sector pick amid recovery hopes

Image © Thyssenkrupp Steel Europe facilities. Image European Union, 2025. Photographer: Pau Barrena

Investor confidence in global and European economic growth has improved markedly amid receding trade tensions, according to Bank of America’s latest European Fund Manager Survey.

Faith in a European macroeconomic decoupling has strengthened, with a net 31% of respondents anticipating accelerated growth in the region, driven primarily by hopes for fiscal support in Germany.

With expectations for European economic growth strengthening and relative optimism about inflation, international investors may find European equities increasingly attractive, especially given the contrast with underweight positioning in U.S. equities.

This suggests a tactical opportunity to rotate into European stocks and the potential for relative outperformance of European markets if growth surprises to the upside.

Such developments advocate for international capital flow dynamics that would bid up the Euro.

"We remain optimistic on the Euro," says Nick Kennedy, FX Strategist at Lloyds Bank. "Europe's big step forward - which carved out fiscal space (for higher defence spending), alongside an even more powerful German fiscal programme (worth approximately €100BN per annum over the next decade) - provides a constructive and timely push."

Donald Trump's tariffs and domestic policies have dented the U.S. exceptionalism trade, which has weighed on the Dollar in 2025. The Euro has been a major beneficiary, and this can continue if investors continue to see value in Europe, as per Bank of America's survey.

The share of respondents expecting the global economy to slow over the next 12 months fell to 59% in May, down from 82% a month earlier. Expectations for a global recession collapsed from a two-year high of 42% to near zero, while 61% now see a soft landing as the most likely outcome, reversing last month’s majority view for a hard landing.

The survey, conducted between May 2 and 8, came ahead of a new U.S.-China trade agreement, suggesting further room for optimism in future growth expectations.

European inflation expectations remained mixed. While 28% of investors expect inflation in the region to fall over the next year, a net 30% expect global inflation to rise.

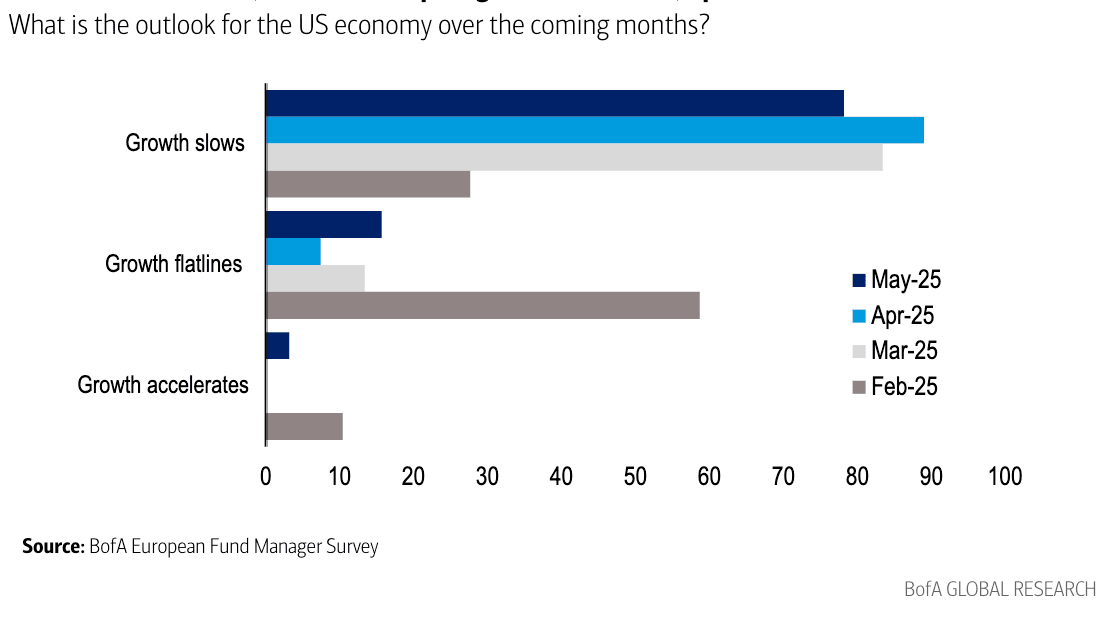

Above: "78% of European investors expect US growth to slow over the coming months, down from 89% last month, while 16% expect growth to flatline, up from 7% last month" - Bank of America.

Bullish Sentiment Boosts EU Equities

Investor sentiment toward European equities has turned increasingly positive. Some 59% of respondents now see upside potential for the region’s stock markets, up from 51% in April. None of the investors surveyed forecast significant downside, compared with 11% the previous month.

A net 35% of respondents reported overweight positions in European equities, close to recent highs, while a net 38% said they were underweight U.S. equities—a two-year peak.

The biggest perceived risk to portfolio positioning is reducing equity exposure too aggressively, cited by 28% of participants.

Banks Lead Sector Preferences

As macroeconomic concerns recede, financials have regained favor among investors. A plurality of 22% identified the sector as the likely top performer this year, followed by industrials at 19%. Banks are now the top consensus overweight, at 28%, with insurance (25%) and utilities (19%) also prominent. Autos, chemicals, and basic resources were the most underweighted sectors.

Geographically, Germany remains the most favored market, ahead of the UK, while Switzerland is the largest underweight by a wide margin.

Meanwhile, 56% of respondents expect high-quality stocks to outperform lower-quality names over the next year—the highest reading in nine months.