Picture by Kirsty O’Connor / HM Treasury.

The British Pound can recover as UK fiscal fears fade ahead of another potential flare-up in the Autumn.

Global and UK bond yields are falling, signalling diminishing fiscal risks to the Pound, which can help conspire a recovery.

Much of this is being driven by the decline in Japanese government bonds, but according to the ONS on Tuesday, UK Public Sector Net Borrowing was £14BN in June, and £20.684BN when adjusted for seasonality. (The £14.0bn is the raw number; the £20.684bn reflects adjusted data to give a more meaningful monthly comparison.)

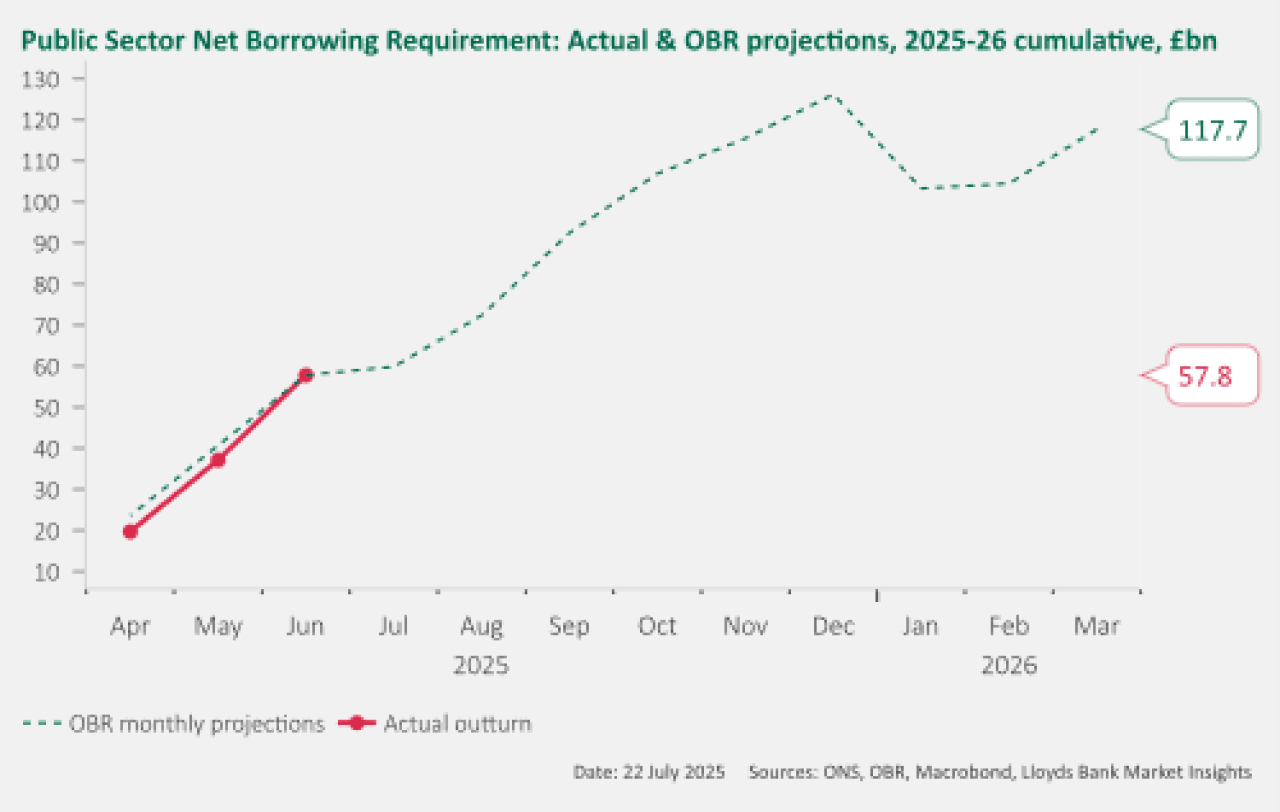

"Whilst this outturn was more than £3bn above market expectations, when looking cumulatively at the deficit for the first quarter of the 2025-26 fiscal year, borrowing of £57.8bn is right in line with the Office for Budget Responsibility’s monthly profile," says Sam Hill, Head of Market Insights at Lloyds Bank.

Image courtesy of Lloyds Bank.

That borrowing is meeting the OBR's forecasts is good news to Chancellor Rachel Reeves, even if it doesn't fundamentally change the UK's poor debt dynamics. After all, this was still the 4th highest June borrowing since monthly records began in 1993.

However, when combined with Monday's broad-based fall in global bond yields, centred on relief pertaining to the outcome of Japan's weekend elections, and Monday's well-subscribed UK government bond auction, the data should further quell the recently rough seas on the bond markets.

Fears for the outlook of the UK's finances have at times caused significant stress to both Reeves and the Pound over recent weeks; calmer summer waters can see some of that risk premium evaporate ahead of Autumn storms.

"We think a rising fiscal risk premium is the main driver of the recent outperformance of EUR/GBP," says a recent note from Goldman Sachs.

"While risks remain, our base case is that this fiscal premium gradually recedes over the summer, supported by what should be a quieter calendar for domestic fiscal announcements through to the Autumn budget in Q4, and a more benign backdrop for Gilt market net supply dynamics," adds the Goldman Sachs research note.

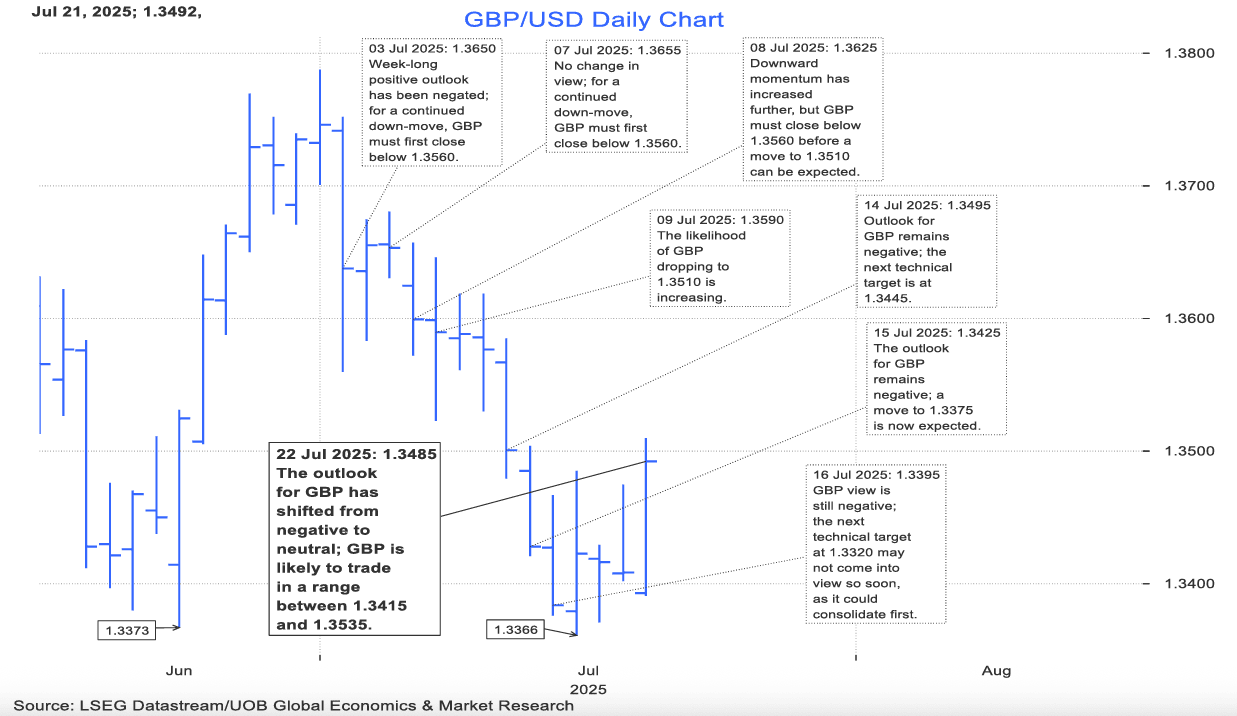

EUR/GBP rose to 0.87 last week amidst ongoing Pound Sterling weakness, but it has since faded back to 0.8678, meaning GBP/EUR is left better supported and able to consolidate around 1.1523. The GBP/USD exchange rate has recovered to 1.35, having been as low as 1.3364.

"The outlook for GBP has shifted from negative to neutral," says Quek Ser Leang, Senior Technical Strategist at UOB, adding:

"GBP soared yesterday and broke above our ‘strong resistance’ level at 1.3490. The breach of the ‘strong resistance’ indicates that the outlook for GBP has shifted from negative to neutral. From here, GBP is likely to trade in a range between 1.3415 and 1.3535. Given the buildup in short-term momentum, the risk of GBP breaking above 1.3535 is higher, potentially paving the way for a more sustained advance."

Looking ahead, Goldman Sachs are wary that the issue of under-pressure UK public finances will flare up again, particularly as the Autumn budget where Reeves will have to lay out new tax and spending plans, approaches.

"We expect it will pay to wait for some of the elevated fiscal premium in the currency to recede, before targeting Sterling downside on European crosses at better levels," say strategists at the Wall Street bank.

The UK's deficit now stands at 5.7% of GDP, which is the 3rd highest among 28 advanced European economies. Total public debt stands at 94% of GDP, the 6th highest among advanced economies.

The 10-year bond yield recently rose to 4.7%, the 3rd highest among advanced economies, but has since fallen back to 4.60%.

This yield is potentially the most important barometer of the health of the UK, as it shows how much investors demand in compensation for lending to the government. The higher it goes, the more risk they see in terms of inflation and the government's ability to pay their money back when the bond is up for redemption.

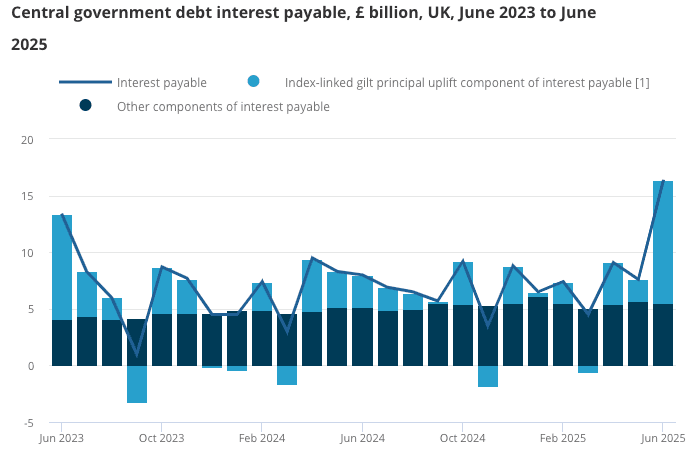

The rising yield also means the government has to pay more and more of its earnings on financing debt, heaping pressure on Reeves. In June 2025, £10.1BN was spent on financing debt, up from £8.8BN in June 2024.

"Recent events have shown how hard it is for the government to bring spending down. Welfare reform was heavily watered down, while winter fuel payments have been reinstated for millions. As we approach the summer recess this is all going to result in additional speculation of what tax rises will be coming down the line given the need to plug the holes," says Richard Carter, head of fixed interest research at Quilter Cheviot.

"Bond markets are craving some fiscal discipline, so without any spending cuts, taxes will have to rise," he adds.

According to analysis from Goldman Sachs, recent fears over the UK's debt trajectory mean the Pound has been unable to capitalise on supportive developments elsewhere.

However, if fiscal fears recede for the time being, these potentially positive drivers could be engaged, helping the Pound higher in the interim.