Image © Pound Sterling Live

The British Pound lost value against the euro and dollar after the ONS said UK economic growth flatlined in July, with increases in services and construction offset by a fall in production.

This 0% monthly outcome was as expected and follows the impressive 0.4% increase in June.

Looking beyond the volatile monthly figures shows the quarterly run rate (three months to July) was 0.2%, down from growth of 0.3% in the three months to June 2025. This was the weakest rolling 3m figure in six months, indicating waning economic momentum.

Indeed, the ONS has said it recognises the noise presented by the monthly data and it will soon lead with the three-month run rate when updating GDP data on a monthly basis.

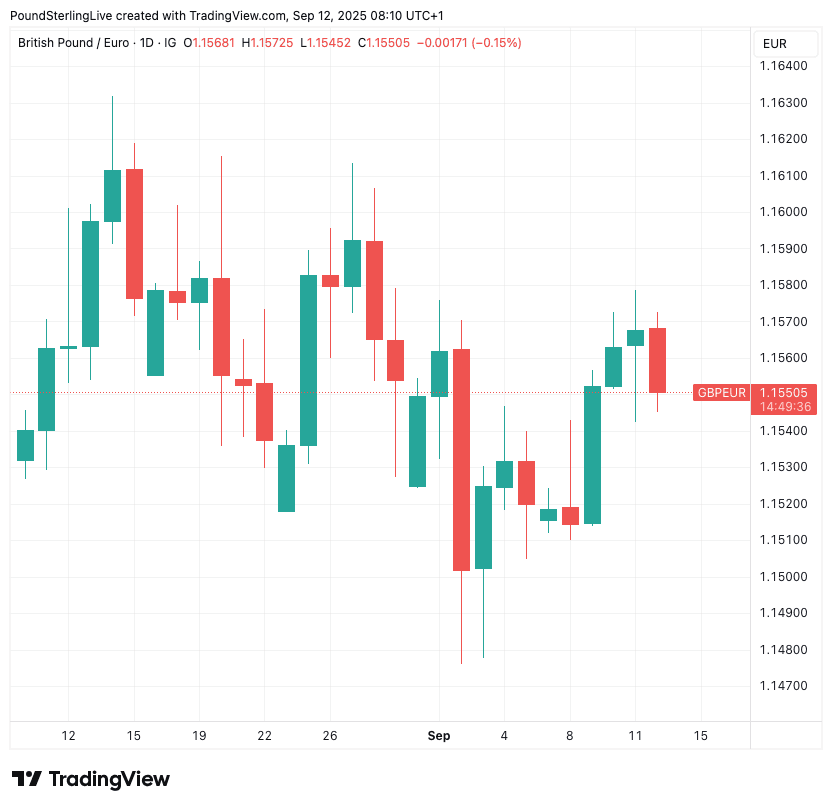

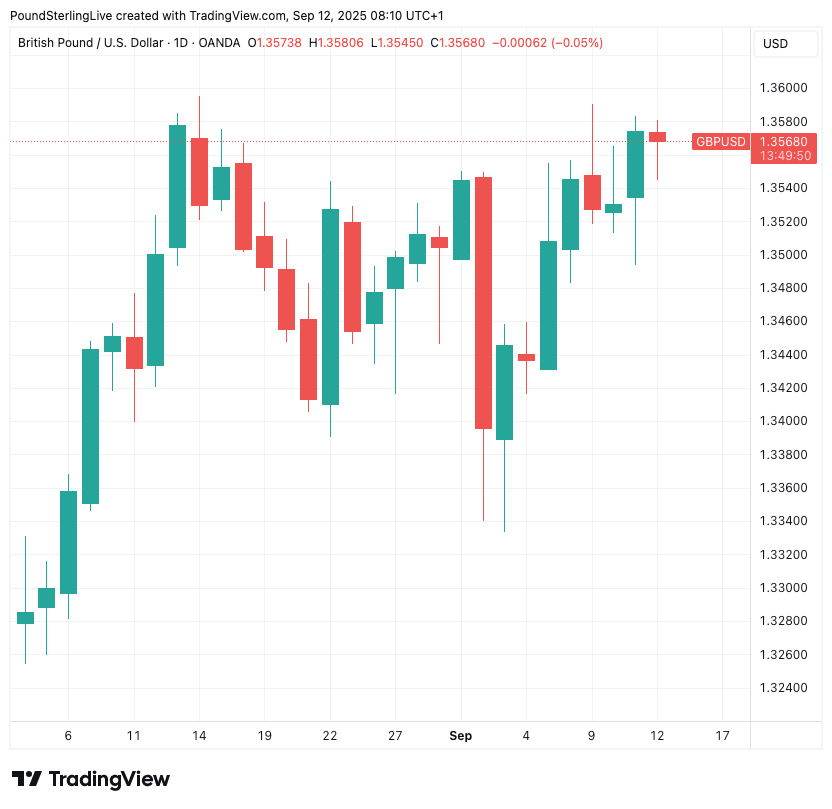

Following the release, the pound to euro exchange rate (GBP/EUR) slipped into the red, going to 1.1550. The pound to dollar exchange rate (GBP/USD) fell to 1.3550.

The slowing growth pulse comes at a crucial time for the economy as the clock counts down to the November budget. Chancellor Rachel Reeves needs growth to pick up in order to convince the Office for Budget Responsibility not to cut their growth forecasts.

These growth forecasts are crucial, as they will determine the size of the fiscal black hole she will need to fill with tax rises.

Markets are therefore likely to be sensitive to UK growth dynamics in the coming weeks and months, with September's GDP series not helping in this regard.

"July’s stagnation underlines the hurdles the economy faces. Inflation remains uncomfortably sticky, interest rates are still in restrictive territory and talk of fiscal ‘black holes’ and likely tax rises in November’s Budget risks weighing on confidence," says Martin Beck, Chief Economist at WPI Strategy.

The British Chambers of Commerce reacts to the data by saying the business landscape remains challenging, particularly for SMEs, with cost pressures impacting investment, recruitment and trade.

While the CBI's latest economic forecast suggests growth of 1.3% this year, "that’s largely down to stronger-than-expected activity in Q1, before the impact of national insurance and tariffs."

The UK enjoyed the strongest H1 GDP growth in the G7, growing by 1.9% on an annualised basis, which coincided with GBP outperformance against the EUR and USD.

"But we regard this as an anomaly rather a sign that the UK economy has emerged from years in the doldrums. The competition was scarcely fierce – three of the other countries scraped above 1% and the remaining three were well below," says Andrew Goodwin, economist at Oxford Economics.

"The UK economy remains exceptionally fragile; subdued growth and high inflation (mild stagflation), and a weak fiscal position are set to persist as a sustainable driver of UK growth has yet to emerge," he adds.

Like the economy, the pound has lost momentum, dropping against the euro and underperforming against the dollar through mid-year and into Q3. Where it once led the charge against dollar weakness, it is now more subdued, watching other currency peers spearhead the advance.

Pound vs. Euro

Despite the disappointing GDP read, Sterling still looks to be on course to register a weekly gain, although the gain is slim and could yet slip by the close of play.

The euro found the European Central Bank's Thursday policy decision and guidance to be supportive: there's little sign the central bank thinks it needs to cut interest rates further.

At the same time, the odds of the Bank of England cutting interest rates next week are virtually nil, meaning the pound will continue to benefit from the UK's elevated base rate.

In fact, the UK has the second-highest policy rate in the G10, and it will become the highest after next week's Federal Reserve rate cut.

So interest rates are the one thing the pound has in its corner, which appears to be protecting it from losses.

Pound vs. Dollar

The dollar is in charge here, and Thursday's on-target U.S. inflation report effectively greenlit next week's interest rate cut.

It also opens the door to further cuts as interest rates in the U.S. are at restrictive levels. Inflation is relatively elevated but it's not steaming higher.

At the same time inflation expectations actually remain relatively well anchored, indicating unhelpful surprises in the data won't show up in the coming months.

With the Fed set to outcut, the dollar can stay pressured.

"To stoke GDP growth back to or above trend, substantial easing will be required," says a note from Westpac, out Friday. "This leads us to expect the US dollar DXY index to slowly retreat."