Image © Adobe Images

The British pound fell after the UK reported weaker job numbers.

Britain added 91K jobs in the three months to August, down from the 232K increase recorded in the previous three-month period, said the ONS on Tuesday.

This means the number of payrolled employees dropped by 93K between August 2024 and August 2025. The unemployment rate edged higher to 4.8%.

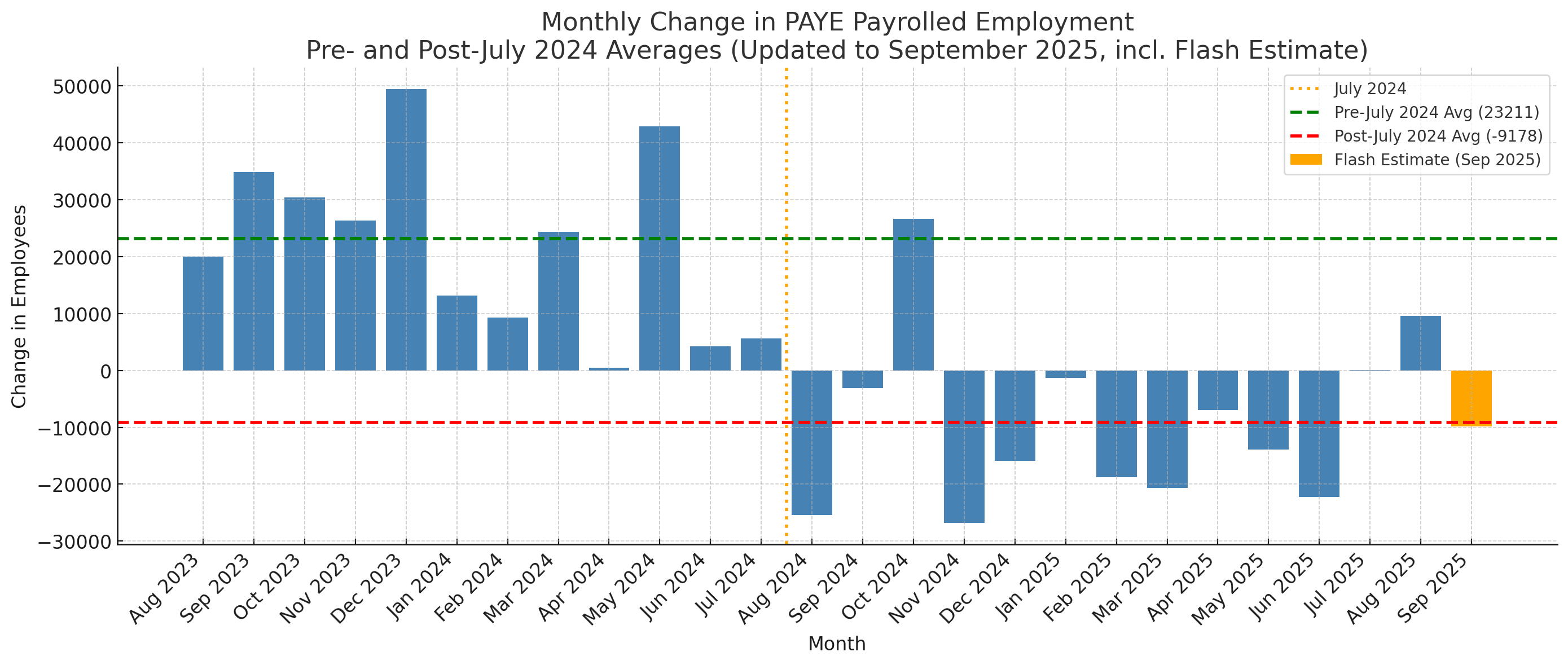

A separate, perhaps more accurate, measure of labour market change is provided by HMRC's PAYE payroll monitor. It showed a fall of 10k jobs in September, making for the 11th monthly decline of the past 13 months.

"While the initial adjustment to last year's hike in employer National Insurance contributions appears now to have finally worked its way through the system, uncertainty ahead of this year's Budget is now clearly acting as a notable drag on economic activity," says Michael Brown, Senior Research Strategist at Pepperstone.

The ongoing softening in the labour market raises the prospect of an interest rate cut early next month.

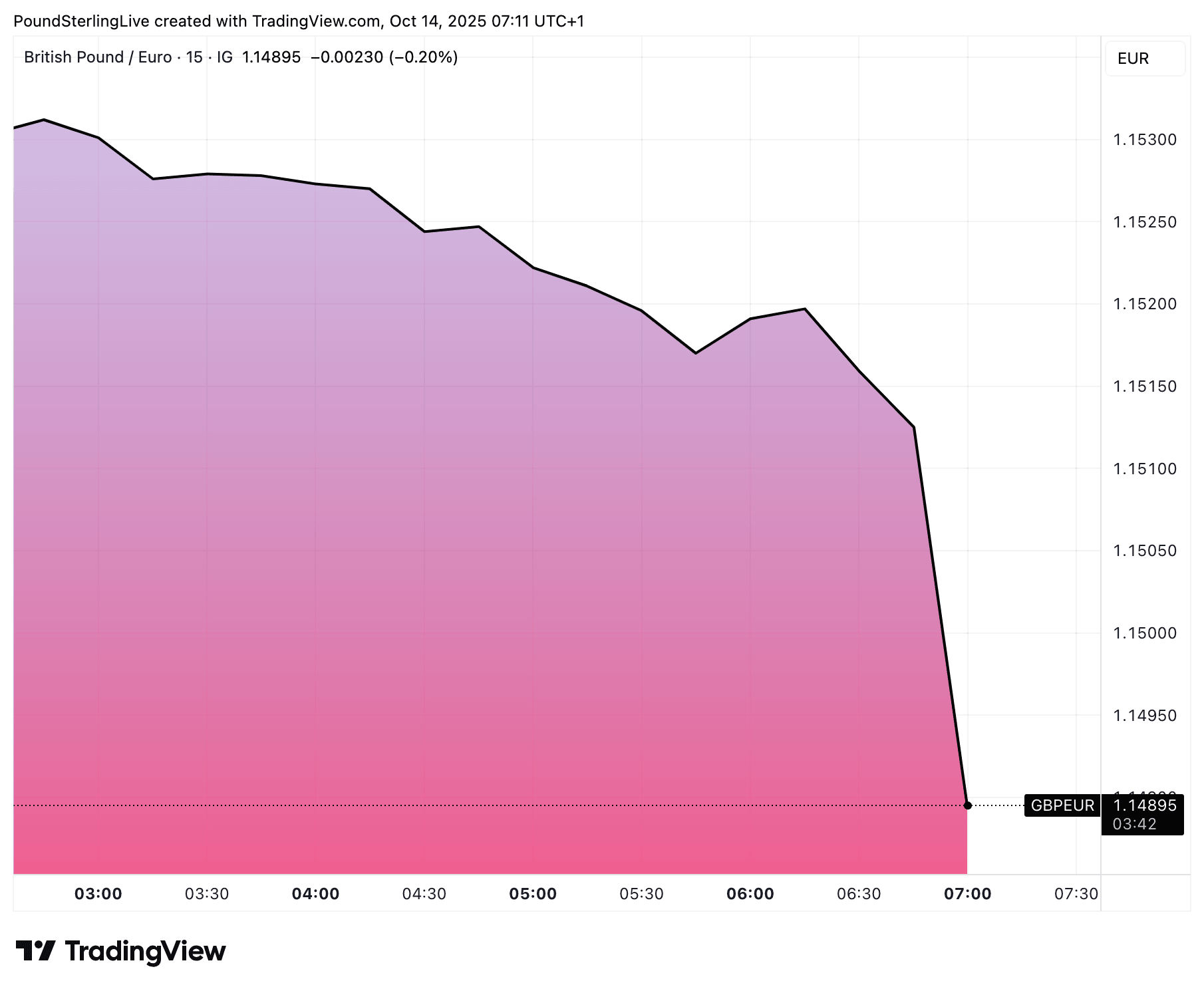

Given this shift, the pound trades lower against its peers:

The pound to euro exchange rate (GBP/EUR) trades 0.30% lower on the day at 1.1489, the pound to dollar exchange rate (GBP/USD) trades down 0.20% at 1.3323.

The British pound has been under sustained pressure against the euro since June and economists say this underperformance is due to the slowing economy and rising fears about the upcoming budget.

The Chancellor, Rachel Reeves, is expected to announce a fresh round of tax increases, with economists saying an additional £20-40BN must be found to ensure the country's financial outlook remains on a stable footing.

Last year, she announced a tax on employment via a rise in the National Insurance tax employers pay on the staff they employ. An unintended side effect of this tax is a steady decline in employment.

With businesses likely to remain 'on hold' until the contents of the November budget are known, it's hard to see this situation improving.

The market has raised the odds of a November rate cut on the back of these data, but the Bank would be wise to consider its steps carefully.

Today's data reveals that private sector pay rose 4.4% in August (down from 4.7%) while public sector pay advanced 6.0%, up from 5.6%.

Such a rate of pay increases is consistent with inflation staying anchored above the Bank's 2.0% target. The public sector pay increases underpin why the government can take some direct responsibility for the UK holding the highest inflation rate in the G7.