Above: File image of Andy Burnham. Copyright by World Economic Forum / Faruk Pinjo. Licensing and source.

The favourite for the Makerfield win is expected to flesh out policy aims, and that's where the risk is.

After his expected win in the Makerfield by-election this Thursday, Andy Burnham will make his pitch to fellow Labour Party MPs as to why they should back him in overthrowing Keir Starmer.

We've already reported that the result of Thursday's vote is not the immediate concern for the pound, as it's been fully anticipated by market participants for some time and is therefore accounted for; instead, it's the policy utterances that will matter most.

And that's why the pound's on Burnham watch: what he says in the days following his win about spending, borrowing and taxing will have potential ramifications for the economy and markets.

"Beyond macro, political risk also comes into view. The Makerfield by-election on Thursday could carry broader implications. A win for Andy Burnham would mark a return to Westminster and potentially revive questions around Labour leadership, adding to pressure on Keir Starmer. Any pickup in political uncertainty risks feeding into higher risk premia, with potential downside implications for both sterling and gilts," says George Vessey, FX analyst at Convera.

The Win is in the Price, His Policies Are Not

The Makerfield by-election was triggered by the resignation of its previous Labour MP in order to help his friend, Andy Burnham, re-enter parliament and overthrow Prime Minister Keir Starmer.

Despite the cynical moves, Burnham looks to be on course to comfortably win the vote, which poses a fresh set of risks for the pound. Polymarket has him regularly at 70-80% favourite to win, odds the FX and bond market will be positioned for.

But what the market isn't positioned for is what Burnham does in office.

"Given that Burnham has recently softened his stance regarding loosening fiscal rules, it is likely not until when he would become PM, and potentially change his stance, that a more material reaction in GBP may be had," says Noah Buffam at CIBC Capital Markets.

A Welfare Spending Blowout

On Monday there was a report that he could give "vulnerable people" a 'basic income' that's five times what they receive on benefits if he becomes PM.

The context of that extra benefits spending comes up against a massive and expanding welfare bill: for 2025-26, the government is expected to spend approximately £323BN on welfare and social security, equivalent to around 10.6% of GDP and 23.6% of all government spending.

Welfare accounts for roughly 26% of all government revenue, 24% of all government spending, more than four times defence spending and about 1.6x NHS England's budget. It's expensive, and it's going to get more expensive unless Burnham pays for his projects by cutting elsewhere in the welfare budget.

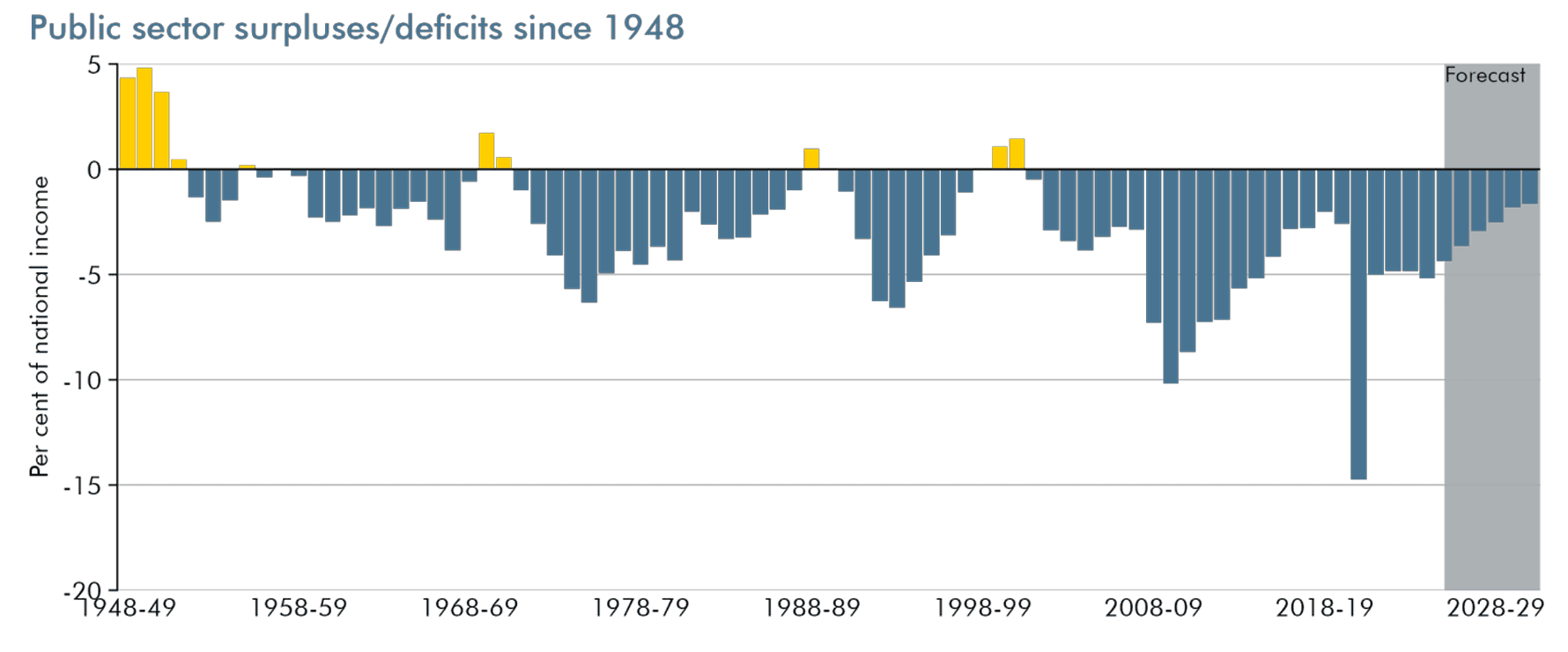

Above: UK budget deficits. The fiscal rule means that the forecast element must be shrinking.

The experience of Keir Starmer and Rachel Reeves in July 2025 shows there is no appetite in Labour's parliamentary party for making any cuts in welfare at all.

Underscoring tight fiscal constraints is Burnham's recent commitment to keep the triple lock uplift to the state pension and give pensioners a tax cut, by carving out a special personal allowance that rises to ensure pensioners don't pay tax on pension incomes.

The State Pension is the single biggest component of the UK's welfare system: it consumes 45% of the welfare budget and additional pension benefits consume a further 10%. That's 55% of the welfare budget that is ring-fenced to expand year-on-year.

Burnham has also reiterated he wants the biggest council house building programme of the "post-war period."

When asked how it will be funded, he says by reining in unregulated rents that inflate the housing benefit bill.

Markets will severely test that answer when given from a position of power.

Sterling and Gilts Are the Pressure Valves

"Burnham’s clear preference for an expansionary fiscal stance, higher taxation and larger gilt issuance present a downside risk to markets," says Matthew Ryan, Head of Market Strategy at Ebury.

The constraints facing Burnham are two-fold: a market that will only lend at increasingly elevated rates and a tax burden that's already at post-war highs.

There are severe constraints on the revenue and borrowing side of the ledger, meaning the pound and gilt markets will quickly show discomfort with unfunded and unrealistic policy announcements.

UK bond yields already trade at a premium to other G7 country peers, which means markets continue to see an unhelpful inflation, borrowing and spending setup in the UK linked to politics:

Above: The UK government is paying a premium to borrow money, with economists saying that's due to elevated political risks associated with the country.

The good news is that Burnham has already shown a propensity to row back on previous commitments. For instance, he once said the government shouldn't go 'in hock' to bond markets, but during the campaign he admitted that he would have to respect the fiscal rules i.e. show the restraint to keep markets on side.

He also abandoned plans to compensate so-called WASPI women, which would have cost billions.

Burnham's newfound fiscal discipline will nevertheless be tested when he comes under pressure to throw his fellow Labour MPs some policy red meat: for left-wing politicians, that's inevitably always increased social spending.

For the pound, that's a risk for the coming months and years.

Comments on WASPI women have attracted attention: compensating them will cost billions.

The reality is there's no additional money, and an Andy Burnham administration will need to throw red meat at his left-leaning constituency to build some momentum when he takes over.

Pound-Euro Can Still Respond to Thursday's Vote: CICB

We report that a Burnham win will not come as a surprise to markets, but seasoned FX veterans at CIBC Capital Markets think there is still some volatility to be had on the event.

Noah Buffam at CIBC Capital Markets said in a preview note, out last week, that although it "appears well priced at this point," it's not entirely priced.

He notes that a 10% drop in Kalshi odds in favour of Burnham on June 11 translated into an approximate 10 pip move in EUR/GBP.

"This suggests that a win for Burnham could lead to 20 pips of upside in EUR/GBP, with 80 pips of downside on a loss," he says.