Burnham following his victory. Image still courtesy of BBC.

The British pound steadies on Friday in the wake of Andy Burnham's win in Makerfield.

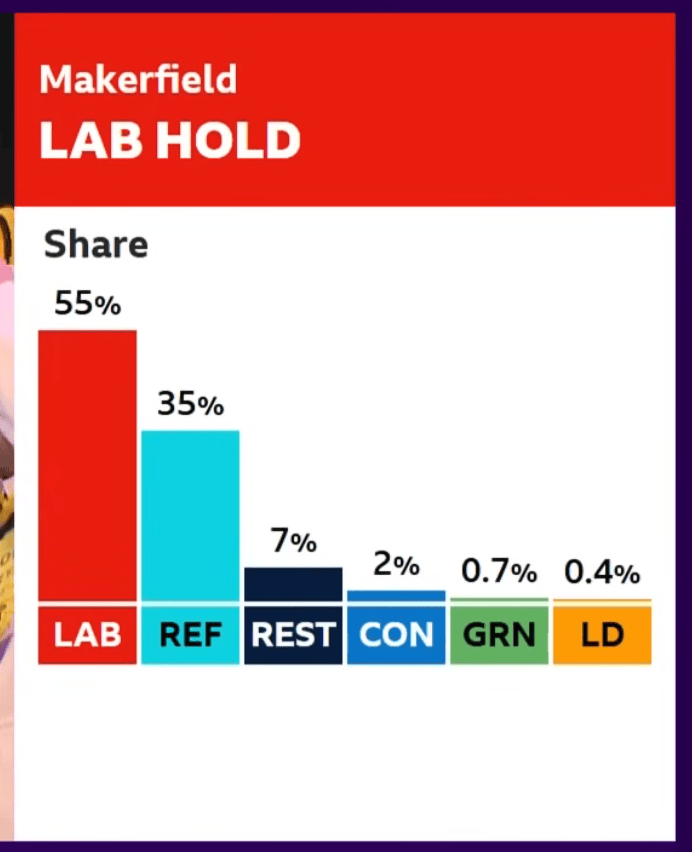

Burnham won with more than 50% of the vote and a 10% swing in Labour's favour, something political pundits say will give him the confidence and mandate to quickly evict Keir Starmer from Downing Street.

UK assets were well-positioned for Burnham's win, meaning the result itself is a non-event for the pound which has already had a busy week, what with the Bank of England decision, an inflation release and the first Federal Reserve decision under Chair Kevin Warsh.

But politics could yet deliver some FX market volatility.

"Andy Burnham winning the Makerfield byelection wasn't a surprise, but a majority of 9,231 is much bigger than most expected. That means he has the momentum to challenge Starmer," says Sam Hill, Head of Market Insights at Lloyds Bank.

What Markets Want

Markets would prefer a quick and painless coronation for Burnham, which would require Starmer to read the room and realise his time at the top is over. It would also require Wes Streeting - another stated challenger - to accept he doesn't have a chance.

Once Burnham is installed, the market preference would be that he governs along a similar fiscal trajectory to which he inherited, i.e. follows the contours of the previous budget and respects the fiscal rules.

Choosing a Chancellor who is committed to these rules would also be preferable, keeping the door open to Rachel Reeve staying in her job.

Under such a scenario, the pound would be more responsive to the domestic economic pulse and evolving expectations for Bank of England interest rate changes.

"Positioning (as I understand it) is for Burnham not to seek a fresh national mandate so markets are assuming he is hemmed in by internal politics on one side, and fiscal constraints on the other," says Simon French, Economist at Panmure Liberum. "So to some extent on the big macro questions about the borrowing envelope, tax footprint, and inflation a Burnham administration would be continuity to Starmer - so relatively little to reprice."

But Burnham Won't Sit Still

Burnham presiding over the status quo is therefore the market's preferred way forward for the UK.

The only problem is that Burnham was elected, and will be selected by his MP peers, to lead the country with a radically different agenda.

The Labour Party of Keir Starmer is unpopular with voters, so he will believe he must try to do things differently, and that's where the risks lie for the pound and UK assets.

Burnham has, over recent years, argued that the government should borrow more to fund social projects and defence. He has argued that taxes must be raised.

But these spending commitments will come up against the constraints of a market that might not want to lend him more money; already, the UK pays a premium to borrow when compared to its peer G7 nations.

The tax burden is at post-war highs, meaning there's likely to be severe friction to further tax hikes that could end up significantly under-yielding against what was expected.

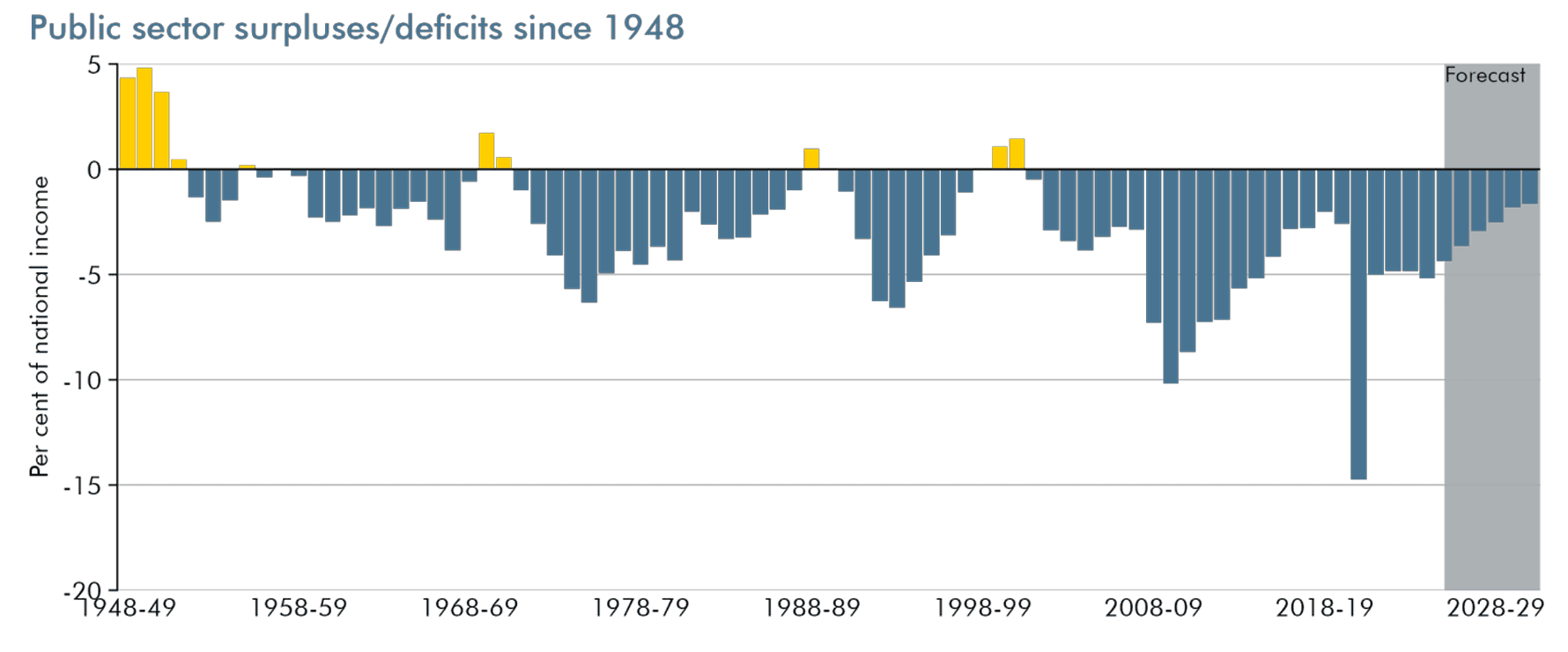

The chart above tells the story: in order for the government to meet the fiscal rules, debt must start to fall in the forecast period. In order to achieve that, the government must preside over an increase in the tax burden (which the current budget plans ensure will happen) and spending reductions.

That's a reality that 'Burnhamism' must contend with. Try to fight it, and the market becomes nervous.

Political Tensions for the Pound

Burnham's political momentum is therefore likely to run into the static and unyielding cliffs of Britain's strained finances.

Testing them and pushing against the market could ultimately trigger a bond market strike, where lenders are less willing to lend, pushing bond yields unsustainably higher and the pound lower.

Time and again we have seen little warning shots of such an event: most famously under Liz Truss, but more recently under Starmer when he tried and failed to reduce the welfare bill.

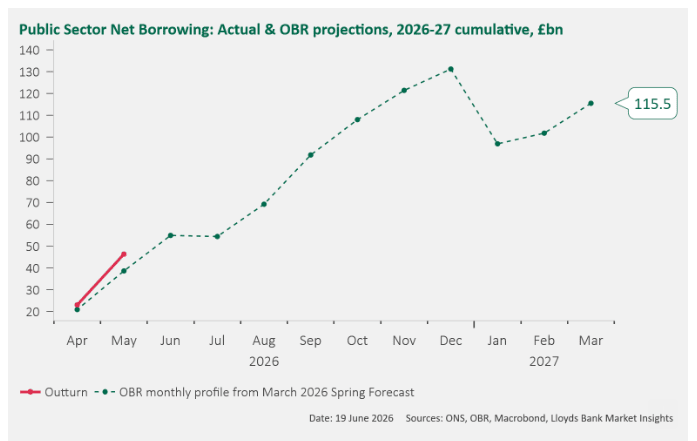

Above: The current year's borrowing is already running ahead of forecast. Image: Lloyds Bank.

Worst-case Forecast Scenario: A Significant GBP Decline

The undercurrents are not favourable to a radical spending and borrowing agenda.

For the pound sterling, a radical left-wing economic agenda that entails higher spending and borrowing would be a severe impediment. Under a worst-case scenario, the pound-to-euro rate could fall well below the 1.11 level that is widely held to be a long-term range floor.

The pound-to-dollar exchange rate could retreat to as low as 1.20 under a scenario where the dollar is strengthening under a more hawkish Federal Reserve regime and the market is punishing fiscal indiscipline in the UK.

What Might Burnhamism Look Like?

Burnham argued in a speech at the IFS that Britain is stuck in a low-growth trap and that restoring public control over key services would lower long-term costs for the state, while past deregulation, privatisation, austerity and Brexit weakened control over public finances.

In the speech, he framed his economic framework as "rolling back the 1980s" through public ownership of buses, more social housing, control of public investment and an industrial strategy.

Tax: The consistent theme is moving the burden away from earned income and onto property, land and wealth, on the view that land and property in Britain are comparatively undertaxed. He's aid he will:

- Restore a 50p top rate above £125,140

- Raise capital gains taxes to equate with income tax bands

- Enact a council tax revaluation to raise council taxes in the South

- Introduce a land tax

Borrowing: In last year's New Statesman interview, he triggered alarm, saying Britain had "got to get beyond this thing of being in hock to the bond markets."

He has since walked this back: he told ITV he "never said you can just ignore the bond markets."

He said Labour's budget constraints "will stay in any context."

If he genuinely keeps the fiscal rules, the radical agenda (council house-building, public ownership, regional investment) has to be entirely tax-funded, which immediately constrains ambition and shifts the burden onto borrowing.

With the tax burden at post-war highs, it invites the question of whether "Burnhamism" is deliverable at scale at all.