Image © Adobe Images

The New Zealand Dollar is expected to remain under pressure in the months ahead as ANZ warns that rate cuts in early 2026 could cap any sustained gains.

Economists at the Australian and New Zealand banking giant say the Reserve Bank of New Zealand (RBNZ) is likely to "keep the OCR unchanged for the remainder of this year" before embarking on a cautious easing cycle once inflation has clearly moderated.

As a result, near-term NZD/USD direction is anticipated to be driven more by offshore events, particularly U.S. dollar dynamics, than by domestic data surprises.

"Markets are in a holding pattern on the Kiwi," says ANZ in a report released August 14, "with global risk sentiment and USD swings likely to dictate the next significant move."

ANZ's baseline scenario sees NZD/USD trading within a broad 0.58 to 0.62 range over the coming months, reflecting a balance between supportive commodity prices and lingering rate-cut expectations.

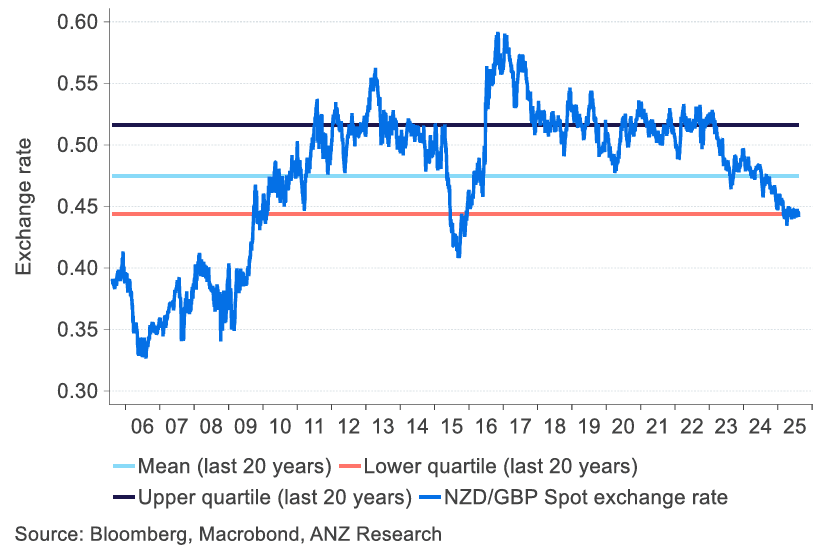

In cross-currency terms, ANZ highlights that GBP/NZD remains well-supported as diverging monetary policy paths and stronger UK growth expectations continue to favour sterling.

NZD/GBP is seen trading to 0.4460 by year-end, and NZD/EUR to 0.5170.

Above: NZD/GBP long-term.

Against the euro, NZD/EUR is seen staying under pressure unless eurozone growth disappoints materially.

"We expect relative growth trends to keep EUR/NZD supported near current levels in the short term," the strategists write.

ANZ economists say the timing of the first OCR cut of 2026 will depend heavily on the path of non-tradables inflation, which remains sticky at present.

"Domestic inflation pressures are still too high for the RBNZ to contemplate near-term easing, but we see scope for rate cuts from early 2026," says ANZ.

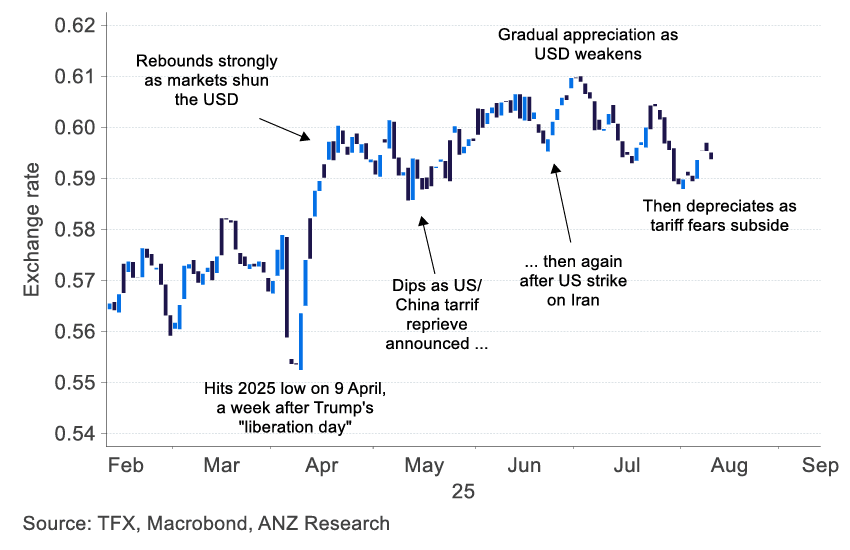

Above: NZD in 2025. Recent Kiwi price action: NZD/USD over the last 6 months – light blue bars on days the NZD fell, and dark blue bars on days it rose.

Analysts caution that a softening in global dairy prices or weaker Chinese demand could see NZD/USD retest the lower end of its range sooner than anticipated.

On the upside, ANZ sees scope for the Kiwi to benefit if U.S. inflation slows more quickly than expected, prompting the Federal Reserve to signal a dovish shift.

"Fed rate expectations remain a key swing factor and any acceleration toward a cutting cycle could narrow NZ-U.S. yield differentials in the Kiwi’s favour," says the bank.

However, this scenario would likely produce only a modest rally unless it coincided with an improvement in global risk appetite.

The research note also flags seasonal patterns, noting that the NZD has a tendency to underperform in August and September before stabilising into the final quarter.

The RBNZ's next policy meeting and forthcoming GDP figures are seen as potential catalysts for local market volatility, though ANZ does not expect them to shift the broader trajectory.

"Absent a major shock, we think the Kiwi will continue to muddle through, with global developments doing most of the heavy lifting," says ANZ.