Image © Adobe Images

A racy rally reaches exhaustion point, but uptrend still intact, RBNZ decision eyed.

The Pound to New Zealand Dollar exchange rate (GBP/NZD) is forecast to pullback in the initial stages of the coming week, but weakness is expected to be short-lived.

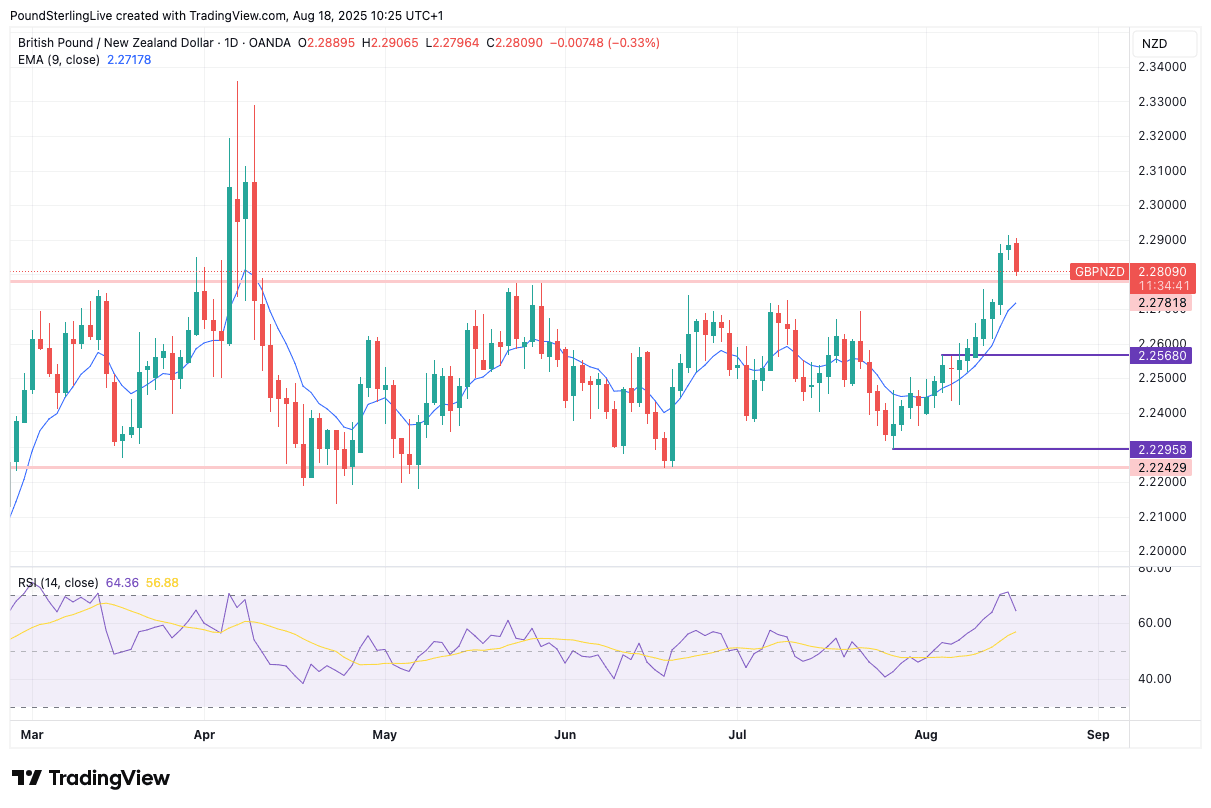

GBP/NZD raced to its highest level in four months last week and leapt above a key resistance point in the process; the ascent was rapid with a near-consecutive run of 15 positive daily closes.

Watching this, we became wary that the rally was at risk of becoming stretched, as on Friday the Relative Strength Index (RSI) breached the overbought 70 line.

The call was for a near-term correction to evolve in order to allow for an unwinding of overbought conditions. On Monday, we see this is happening with the pair down a third of a per cent from the open at 2.2810.

Initial support would likely be the horizontal graphic at 2.2781 that serves as the upper-bound of the 2025 range. If it is a source of support then look for steady buying interest and some sideways consolidation around it.

However, we note that the nine-day exponential moving average (EMA) is lower than this point down at 2.2717, and it might attract sellers in the coming hours.

The nine-day is important for our Week Ahead Forecast model: while above it, the short-term trend is higher. But, any significant divergence away from the nine-day EMA also signals overbought conditions and we would anticipate short-term weakness to allow spot to reconnect.

Another scenario worth considering is that the gravitational pull of the 2025 range, as identified by the linear red tramlines in the chart, works its magic.

Here, the recent rally is a mere reversion into the range that was subject to a bit of overshoot, but an eventual continuation of the range ensues. Under such a scenario, levels below 2.2781 play out over the coming weeks.

However, for now, we think the upside momentum has been reestablished and think there is potential for the pair to establish itself at higher levels. The highs at around 2.30 are targetted in this scenario.

The Reserve Bank of New Zealand is expected to cut the OCR by 25 basis points to 3.0% on Wednesday.

Presently, markets see a 50/50 chance of another cut in November. With August 'in the price' of the NZ Dollar, it is how the thinking about November shifts that will deliver a currency market impact.

It is in the guidance where potential surprises lie: any firmer commitment to a cut in November and beyond - in whatever form that communication might be delivered - would likely weigh on the Kiwi.

However, should the central bank indicate it considers itself at the end of the cycle, NZD would receive a boost on the day.

An outright 'bullish' outcome for the NZD would be a decision to hold interest rates midweek. "There’s a decent case to remain on hold at this meeting and see how the economy progresses over the rest of the year," says Kelly Eckhold, an economist at Westpac.

He notes that Kiwi inflation is nearing 3.0%, which is way above the RBNZ's target, and the economy is not exactly desperate for further assistance.

UK Inflation and PMIs

The GBP/NZD rally was ignited by the August 07 Bank of England policy decision and guidance update. To recap: the Bank cut rates, but it was clear the Monetary Policy Committee (MPC) was hesitant to guarantee further cuts. This prompted the market to slash the odds of a final cut for the year in November.

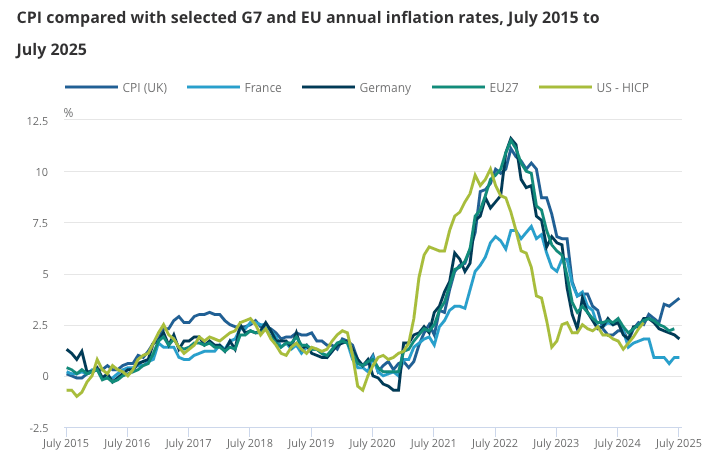

That repricing raised UK bond yields, which mechanically lifted the Pound. The Bank's coolness towards cutting rates rests with the country's still-high inflation levels, and Wednesday should see this situation confirmed.

UK CPI inflation is due for release and a figure of 3.7% y/y is anticipated, which puts inflation far too high to justify the ongoing easing stance the Bank is pursuing.

Should inflation beat expectations, then GBP can rally. However, we are wary of a situation whereby inflation smashes expectations. This wouldn't be good for GBP as it suggests inflation is a real problem that risks destabilising UK bond markets and killing economic growth.

Thursday's PMI data will also be of interest as it will give the first real insight into how August is going for the economy. Last month's release disappointed and resulted in GBP weakness, confirming that it is an important event for the Pound.

So too will be Friday's retail sales as this will give an indication of how consumers are holding up. There are risks that the rising inflation rates we are seeing will weigh on the economy, which would be a negative for the Pound.

Nevertheless, we think GBP/NZD weakness will be relatively shallow at this juncture as the data will unlikely materially shift the Bank of England's thinking that it might be prudent to leave interest rates steady for the remainder of the year.

There are no data points of market consequence out of New Zealand this week.