Image © Adobe Images

But weakness is to be short-lived as it's still unwise to bet against the GBP/NZD uptrend.

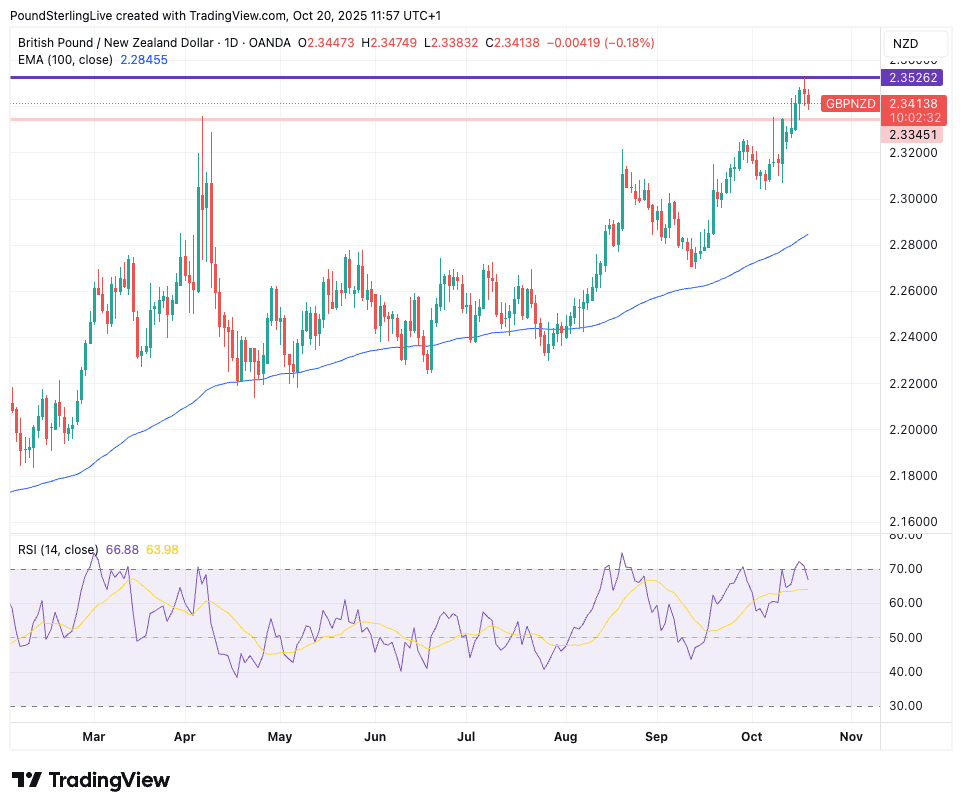

Pound to New Zealand Dollar exchange rate (GBP/NZD) can give back some recent gains in the coming hours and days.

This is our assessment after the pair reached overbought conditions again last week, leaving us expectant of a retreat in the coming days as those conditions to unwind.

Last week saw the pair rise to a new post-2015 peak at 2.3526, consistent with GBP/NZD enjoying one of the more consistent and enduring trends in global FX during 2025.

The sauce for this latest move was another flare-up in U.S.-China trade tensions, a perennial feature of the geopolitical landscape in 2025 that is particularly risky for the kiwi.

After all, the Kiwi, like its mate the Aussie, is a Pacific currency that is linked to China to the extent it is treated as a G10 currency proxy to the world's second-largest economy.

Nevertheless, U.S. President Donald Trump said over the weekend that another 100% increase in import tariffs on Chinese goods, which he threatened days earlier, was not sustainable.

He is also still booked to meet Xi Jinping, China's President, in South Korea later this month. In preparation, another round of Chinese and U.S. trade negotiations are set to kick off in Malaysia this week.

So, despite the volatility-inducing headlines, the wheels are still in motion towards a U.S.-China trade accord, which is ultimately supportive of the NZD.

GBP/NZD's retreat to 2.3415 reflects the associated improvement in sentiment and a further unwinding of overbought conditions could take the pair lower to 2.3345, a level that previously acted as a technical resistance barrier.

However, weakness should be shallow and short-lived as the pair remains in a firm uptrend that's simply too strong to bet against at this juncture, and fresh multi-year highs beckon over the coming weeks.

Some NZD strength at the start of the week can be attributed to quarterly inflation data, which advanced 1.0% q/q in the third quarter (0.9% consensus), which marginally lowered market-implied expectations for further RBNZ interest rate cuts.

(This matters, as the RBNZ's proactive approach to cutting interest rates is a major driver of NZD underperformance).

Year-on-year, Kiwi inflation stands at 3.0% said StatsNZ, which puts it at the upper end of the RBNZ's target range.

That being said, the market might look through the headline as some of the strength in inflation was driven by one-offs. In fact, measures of core inflation - that subcomponent that really matters - continued to ease.

Core inflation fell to its lowest level since June 2021. Economists continue to expect the RBNZ to cut the OCR by 25bps at its next meeting in November, following the 50bp cut this month.

This should keep the NZD under pressure.