President Trump says he wants the Bill passed by July 04. Official White House Photo by Abe McNatt.

The Dollar softened at the start of July and analysts see further declines likely in H2 as fears of a U.S. fiscal crisis evolve.

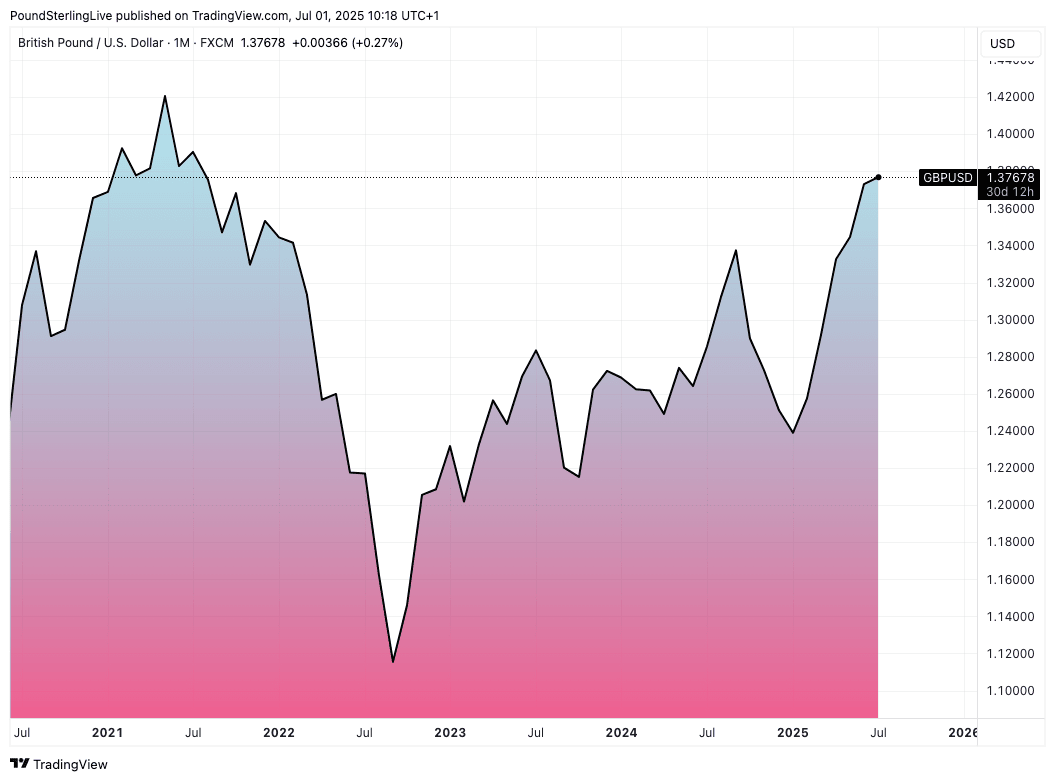

The Pound to Dollar exchange rate (GBP/USD) printed a new high as the second half gets underway, reaching 1.3774, surpassing last Thursday's peak at 1.3725.

"The U.S. currency opened weaker today as well, on persistent concerns tied to fiscal stability ahead of the Senate debate on Trump’s expansionary measures (not fully embraced even within the President’s own party), and given the uncertainty surrounding trade policy management," says Asmara Jamaleh, Economist at Intesa Sanpaolo.

Sterling's advance is almost exclusively a function of U.S. Dollar weakness, and if we look at the UK picture, it is difficult to find any positives for the Pound, meaning GBP/USD is a mere passenger in thrall to external drivers.

"Sterling also opened the week on the rise against the dollar, from GBP/USD 1.36 to 1.37, exclusively on the latter’s weakness, as proven by the fact that it dropped against the euro," says Jamaleh.

Dollar weakness is the overarching FX market theme, with losses resulting from a lengthy list of developments, all of which originate in the White House. For those asking what comes next, the question, therefore, is whether White House policy is about to change anytime soon.

The answer is no: Trump is sticking with his plans to raise tariffs and pass the One Big Beautiful Bill, which will raise the U.S. debt burden by trillions of dollars over the coming years.

Given that these are two key drivers of the Dollar decline, we can expect more USD losses as Trump pursues his key policies.

Above: GBP/USD rises to levels last seen in 2021.

It's the One Big Beautiful Act that is really at the forefront of investors' concerns as we start the second half of a year that has already seen the Dollar lose significant value.

U.S. Senators have convened at the Capitol for a process known as "vote-a-rama", where they will vote and propose amendments to the legislation over what is expected to be many hours.

We know Trump wanted to have the Bill signed by July 04, and Republicans in both Houses of Congress are rushing to deliver for their boss.

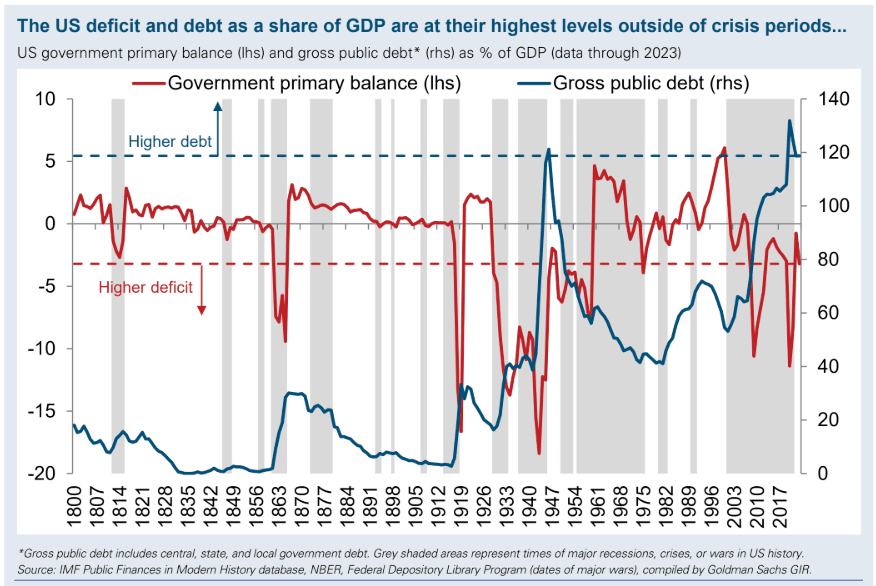

Under a "current policy" baseline, the CBO (via the Committee for a Responsible Federal Budget) estimates $3.94 trillion in total added debt through 2034, comprising approximately $3.25TRN in primary deficits and $0.69TRN in interest.

Image courtesy of Goldman Sachs.

Ex-Trump fan boy, Elon Musk, is so concerned by the debt explosion that he is threatening to start a new political party.

"U.S. fiscal concerns have surged on the back of the Trump Administration’s One Big Beautiful Bill Act, which has helped fuel a sharp rise in long-dated bond yields. But such concerns are nothing new, so is this time really different?" asks Allison Nathan, senior strategist within Global Macro Research at Goldman Sachs.

The Wall Street bank recently asked three big names in finance, academics and histrionics whether the deficit matters: these being Bridgewater’s Ray Dalio, Harvard's Kenneth Rogoff, and historian Sir Niall Ferguson.

"All three believe the answer is 'yes' and make their case for why they think a crisis lies ahead and what it might look like," says Nathan.

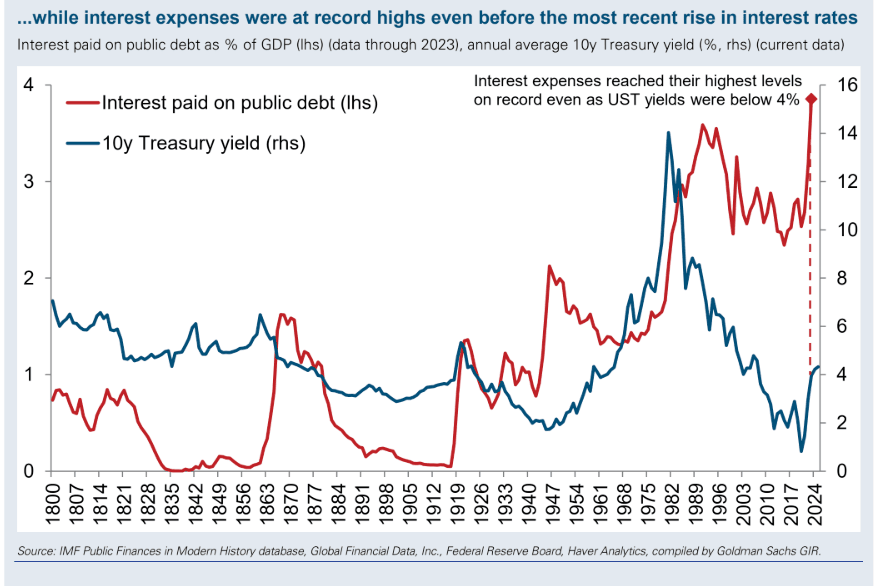

Image courtesy of Goldman Sachs.

They say a crisis is not inevitable, but agree that avoiding it will require the U.S. to significantly lower its budget deficit, especially if real interest rates remain elevated.

"Rogoff and Ferguson are not optimistic that voters and politicians are motivated to make such changes," explains Nathan.

According to Ferguson, "history is ripe with examples of superpowers that have spent more on debt service than defence and subsequently were no longer super or powerful. That’s exactly the position the U.S. is in today."

Analysts often point to the example of Japan in defence of U.S. largess, as the Asian country has historically been able to run significant deficits.

But Goldman Sachs Chief Asia Pacific Economist Andrew Tilton points out that Japan and China can afford to run these deficits because of their high domestic savings, which have allowed both countries to run persistent current account surpluses and accumulate large positive net international investment positions.

The U.S. runs a dual deficit in the domestic budget and the international account (the current account, which reflects America's penchant for importing more than it exports).

Goldman Sachs Head of Global FX, Rates, and EM Strategy Kamakshya Trivedi says he doesn't necessarily think that the U.S. will experience a Gilt-style crisis, though he does expect long-end rates to remain high and the Dollar to weaken further as US exceptionalism continues to erode.

A key point to consider is that as long as the current concerns simmer, the Dollar can continue to fall.

But in the event of a full-blown crisis, we could see the USD reaction function quickly swap, and it starts to benefit from safe-haven inflows. This is because a crisis in the U.S. will hit everywhere hard.

Currencies that don't tend to do well in these scenarios - such as the Pound - will be hammered.

It is also likely that the UK, which also runs twin deficits, would be punished first in a situation where markets are uncomfortable with expanding deficits, so for Pound-Dollar, the road higher is paved with risk.