Image © Adobe Images

The Pound is forecast to stay under pressure against the Dollar in the coming days on a potential reversal in FX market drivers.

The Pound to Dollar exchange rate (GBP/USD) starts the new week in the red at 1.3625 amidst soft investor sentiment that market commentators say is linked to renewed trade tensions.

U.S. President Donald Trump said overnight that the U.S. would add an additional 10% tariff on any country aligning with "the anti-American policies of BRICS."

The warning comes as the U.S. finalises trade deals with a number of partners, while the U.S. is expected on Monday to begin informing other trade partners of the tariffs it has settled on. They will be implemented from August 01.

"The 90-day US tariff pause began on 2 April and is set to expire on Wednesday, leaving markets uncertain about what comes next. Trump announced on Sunday that the higher tariffs are set to take effect on 1 August, but countries without a bilateral deal will be notified by the 9 July deadline," says Shane Strowmatt, an analyst at LGT, the private bank.

"I am pleased to announce that the UNITED STATES TARIFF Letters, and/or Deals, with various Countries from around the World, will be delivered starting 12:00 P.M., Monday, July 7th," said Trump on his Truth Social platform.

Those partners lucky enough to be at the negotiating table, will be told that "if you don’t move things along, then on August 1 you will boomerang back to your April 2 tariff level," said U.S. Treasury Secretary, Scott Bessent.

So on one hand we have the potential for trade issues to be settled, which investors would welcome, but on the other hand, Trump's warning about BRICS shows the issue will never truly be settled.

Indeed, the President will almost certainly continue to threaten fresh tariffs throughout his second term as it is clear he sees it as an important policy tool.

But there is something interesting to observe on Monday: the Dollar is actually higher despite of the uptick in trade-related uncertainty.

Usually, the U.S. currency would be leading the losses on such news, as markets see tariffs as being detrimental to consumers and businesses, meaning they would likely trigger a slowdown in the economy.

That the Dollar is higher, and the Pound lower, might suggest that we cannot expect the clear-cut FX market relationships that dominated H1 to persist in H2.

The Dollar also entered the new month heavily oversold on some metrics, with positioning against it now at elevated levels. It has also traditionally outperformed during periods of stock market weakness, as it is a traditional 'safe haven' asset, alongside the Yen and Swiss Franc.

If this long-held relationship with risk reestablishes, regarless of it being caused by tariffs, the scope for meaningful recovery in the Dollar will build, opening the door to further GBP/USD weakness.

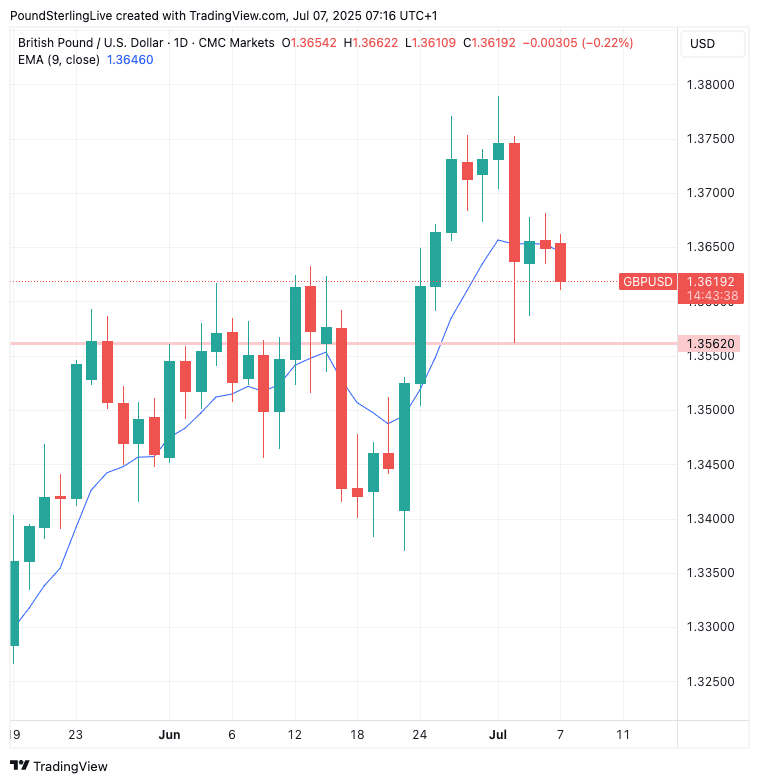

From a technical perspective, the GBP/USD is capped by the nine-day exponential moving average, which is the line in the below chart:

Above: GBP/USD at daily intervals.

While below the nine-day EMA we would look for further losses to 1.3562, which is last week's low. A break above here would mean a retest of 1.3750 becomes possible again.

For now, we see 65-35% odds that the lower level is tested before the upper level in the coming week.

We're in for a quiet week on the data release front, with neither the U.S. or UK offering much of interest. This means last week's above-consensus U.S. economic data prints will linger unchallenged in investor minds.

A strong set of data, including the all-important monthly jobs report, suggested the odds of a Federal Reserve rate cut later this month are close to 0%. This has helped the Dollar of late, and if odds for cuts over the remainder of the year fall further, the currency can find more support.

Pound Sterling meanwhile faces strengthening domestic headwinds, with last week seeing a breakdown in sentiment towards the UK on renewed fears the country's debt was becoming unsustainable.

The big red down candle is visible in the above chart, and the scale of the selloff alone is enough to be a direction changer.

Although Chancellor Rachel Reeves remains in her position, something that calmed markets that were worried she might be fired, it doesn't change the material facts of the case: The UK is massively in debt and that debt is only going to grow.

Reports over the weekend suggested tax rises were inevitable. With the tax burden being at post-war records, it means the likelihood those tax increases realise significantly higher revenues for the government are vanishingly small.

Instead, higher taxes from here are likely to shrink the tax base and slow the economy, meaning the Pound will continue to face significant risks in the coming months as fears about the outlook crop up on an increasingly regular basis.