Official White House Photo by Daniel Torok.

Dollar headwinds will build again when the new tariff regime starts to show up in the data.

The August 01 tariff deadline has arrived, and countries that failed to reach a new agreement with the U.S. will be tariffed well above the global 10% baseline.

Canada's non-USMCA compliant goods will be tariffed at 35%, although this is expected to come down as negotiations will continue.

Countries with high rates are Switzerland (39%), Taiwan (20%), Israel (15%), South Africa (30%), Venezuela (15%) and Sri Lanka (20%). Cambodia, Malaysia and Thailand get a 19% rate, and Laos and Myanmar are at 40%.

With these final confirmations, Yale University's Budget Lab says the effective tariff rate levied by the U.S. will be 18.4%, the highest since 1933.

The overall U.S. price level in the U.S. should rise by 1.8% as opposed to the counterfactual of unchanged tariff settings.

"Inevitably this cost will likely start to show up much more clearly in the inflation data," says a note from MUFG Bank following the August 01 announcement.

Yale's Budget Lab says the average U.S. household income loss from tariffs should amount to about $2,400. However, some good news for a highly indebted U.S. government in that it should raise between $2.8trn and $2.3trn in tariff revenues.

Markets and the U.S. Dollar have largely ridden out the initial shocks associated with Trump's tariff announcements, on the basis they have not yet shown up in the data in any material fashion.

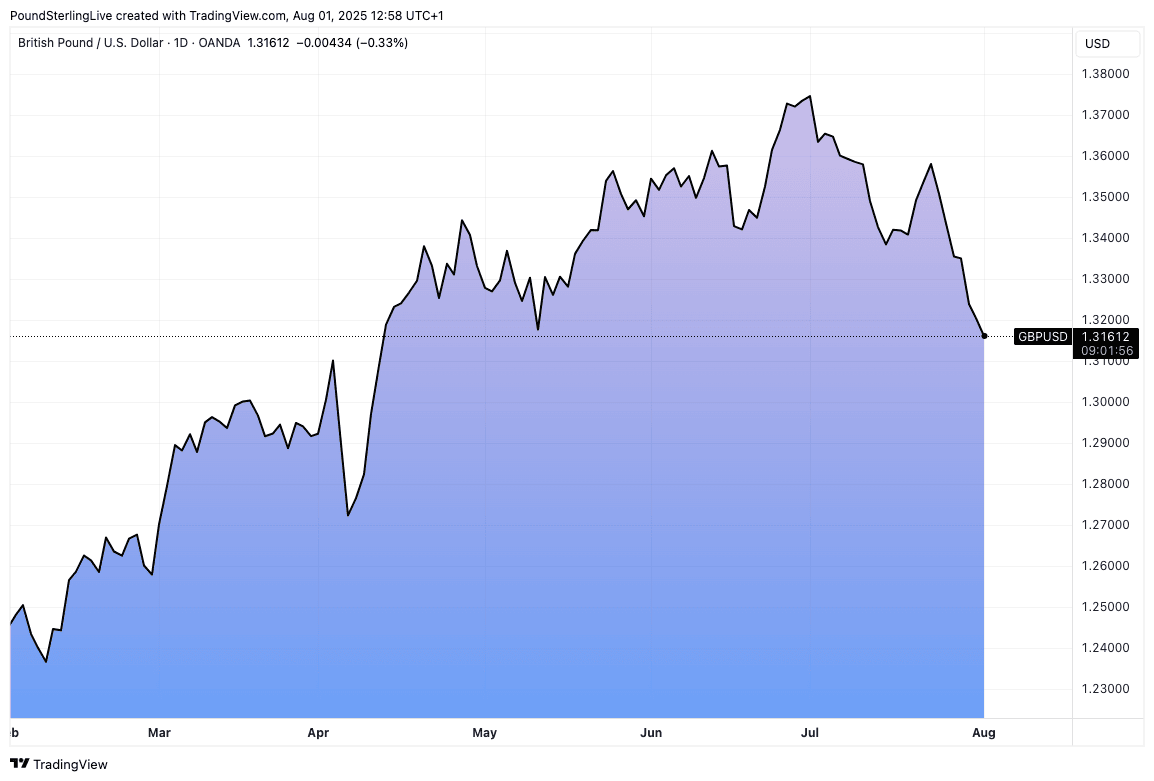

Above: Fading tariff uncertainty has weighed on GBP/USD.

But, MUFG's assessment is that this is because U.S. businesses and foreign exporters 'front ran' the tariffs by surging imports ahead of their implementation.

This provides a cushion. However, economists say this will ultimately fade and some negatives will show up in the data.

"We believe the recent data flow reflects more the ability of US companies to avoid tariffs and that there’s no such thing as a free lunch and hence negative implications still lie ahead," says MUFG.

The Dollar underperformed all its G10 peers in the first half of the year as investors positioned for a negative tariff impact on the economy. But by July the conclusion reached by markets was that tariff uncertainty was coming to an end, allowing the Greenback to recover some of the previously lost ground.

However, although tariff rate uncertainty has ended, the real-world impact of these decisions is still yet to show up.

The Dollar's rebound can extend if tariffs prove benign and no surprises emerge. However, if the true impact of these historic measures has been merely delayed, not cancelled, then the Dollar will begin to feel the strain again.

"While the dollar sell-off in April included a degree of shock and surprise that won't be replicated now, we would still conclude tariffs as ultimately dollar negative over time as it hits real growth, lowers real yields and will encourage portfolio diversification. More domestic-demand orientated policies in Europe and China will also help undermine the dollar," says MUFG.

A big question going forward, however, relates to whether the FX market reaction function of H1 will continue into H2, specifically will the Dollar fall if tariffs start to have a negative impact?

That the USD fell in H1 surprised forecasters who thought it would rise as classic demand for 'safe havens' - of which the USD is considered - rose as global and U.S. growth took a hit.

Markets have reacted poorly to the August 01 tariff announcements, with risk sentiment deteriorating and stocks falling. However, the Dollar is rising, which suggests the classic 'risk off' reaction to tariffs is boosting the Dollar.

So, we could see a scenario where tariffs are once again good for the Dollar and the recent rebound evolves into a more durable rally.