Above: File image of Stephen Miran.

Stephan Miran's growing influence puts a weaker Dollar at the centre of the White House's agenda.

The Trump administration appears fully committed to a weaker dollar, which suggests the currency's slide is here to stay.

Following in the footsteps of Nixon, Reagan and Bush Jr., Trump is the latest in a line of Republican presidents intent on bolstering U.S. industry by targeting its expensive currency.

His dedication to the devaluation of the Dollar was confirmed on August 08 when he nominated Stephen Maran to fill a vacated seat on the U.S. Federal Reserve's Board of Governors.

"The nomination of Stephen Miran, an outspoken advocate of a weaker currency, to an open seat on the Federal Reserve Board signals that Washington remains committed to a policy of dollar depreciation," says Stéfane Marion, an economist at National Bank of Canada.

Miran was Senior Strategist at Hudson Bay Capital and currently serves as Chairman of the Council of Economic Advisers, which advises the White House on economic policy; his fingerprints are visible all over the Administration's policy on international trade.

He believes that the Dollar's overvaluation has hollowed out U.S. industry, and he advocates tariffs as a tool to not only rebalance global trade, but to drive Dollar devaluation.

"The U.S. administration is trying to tackle the overvaluation of the dollar as part of the reset in the global trading system to put American industry on fairer ground vis-à-vis the rest of the world," says Kenneth Broux, a strategist at Société Générale.

Writing for his old employer, Hudson Bay Capital, Miran says a persistently overvalued dollar distorts the global trading system by reducing the competitiveness of U.S. exports and subsidising imports:

"The strong dollar has contributed to the deindustrialisation of large parts of the United States and persistent trade deficits."

This misalignment is said to encourage unsustainable global imbalances, where surplus countries benefit from artificially cheap exports to the U.S., while the U.S. absorbs excess global demand at the expense of its manufacturing base.

"The current configuration of the global system rewards nations that peg their currencies or engineer undervaluation," he says.

Miran says a weaker dollar must become an explicit policy goal, not merely a by-product of monetary policy or market forces:

"A necessary condition for restoring balance to the global trading system is a managed decline in the value of the U.S. dollar."

He argues currency adjustment is an indispensable mechanism to support structural trade rebalancing and to enable the re-industrialisation of the American economy:

"Dollar depreciation is the least disruptive tool available to boost net exports and reduce reliance on fiscal transfers or industrial subsidies.

"A recalibrated dollar, in combination with industrial strategy and supply chain resilience, forms the foundation of a more equitable global order."

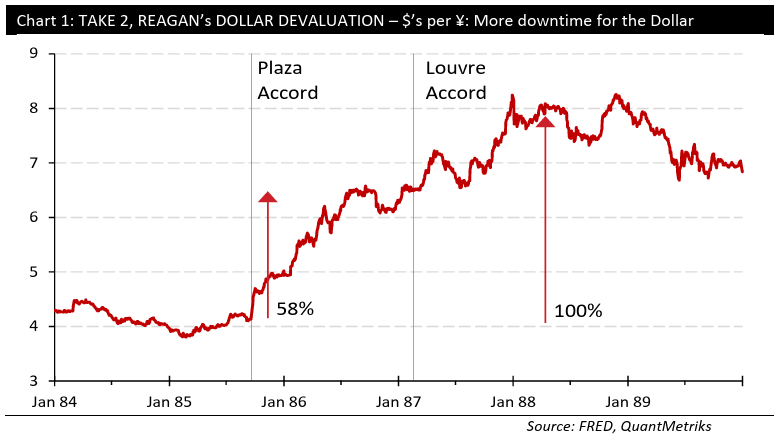

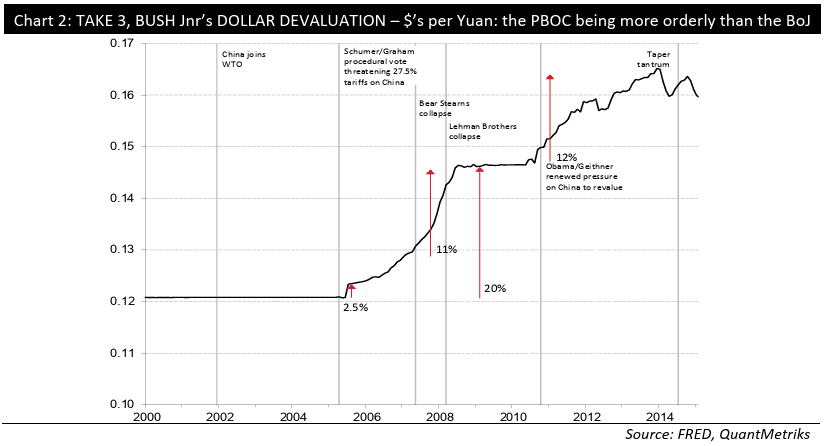

This puts the Trump White House on course to oversee the fourth orchestrated devaluation of the Dollar, the previous three being conducted by Republican predecessors:

- Nixon in 1971, who suspended gold convertibility and imposed tariffs.

- Reagan in 1985, who engineered the Plaza Accord to force coordinated dollar weakening, largely centred on the Japanese Yen.

- Bush Jr. in the early 2000s, when the target was China.

"Japan & then China were confronted with the imposition of 30% tariffs on goods exported to the U.S., unless each in their time, acted to make the trade playing field less uneven. What we know as FACT is on both occasions, the real & present threat of tariffs saw 11-hour agreements to allay them. And the fact was simple enough to capture in a mere soundbite, Japan & then China each in their respective times, agreed to devalue the Dollar," says Dr. Savvas Savouri, an economist at QuantMetriks.

Trump, returning in 2025, is replicating this playbook via tariffs and protectionist rhetoric.

U.S. Treasury Secretary Scott Bessent is active in the devaluation game, this week triggering a USD/JPY depreciation after stating that the Bank of Japan is "behind the curve" in addressing inflation and that further interest rate rises were required from Japan.

"Bessent just called out the BOJ that they are behind the curve, and rightly so," says Le Shrub, a pseudonymous market commentator and seasoned investor known for running the Shrubstack Substack.

Above: File image of Scott Bessent, centre. Official White House Photo by Daniel Torok.

He points out that the U.S. has a 4.5% base rate with 3% inflation, meanwhile Japan has a 0.5% rate with 3% inflation.

"I'm with Bessent on this one. You can argue all you want whether the Fed should cut 50bps or 150bps, but the BOJ is seriously taking the mick here!"

The White House wants a stronger Dollar, and they are working hard at delivering it, with the majority of the readjustment to come against the Yuan and Yen.

Yet, this broader USD downtdraft will lift all other currencies: for its part, QuantMetriks forecasts a high in GBP/USD at 1.70 within the 2025-2029 horizon, with EUR/USD peaking at 1.21.