Above: Fed Chair Powell's guidance will be important for USD direction this week. File image of Jerome Powell. Source: Federal Reserve.

The pound can extend its rally against the dollar in an important week for both currencies.

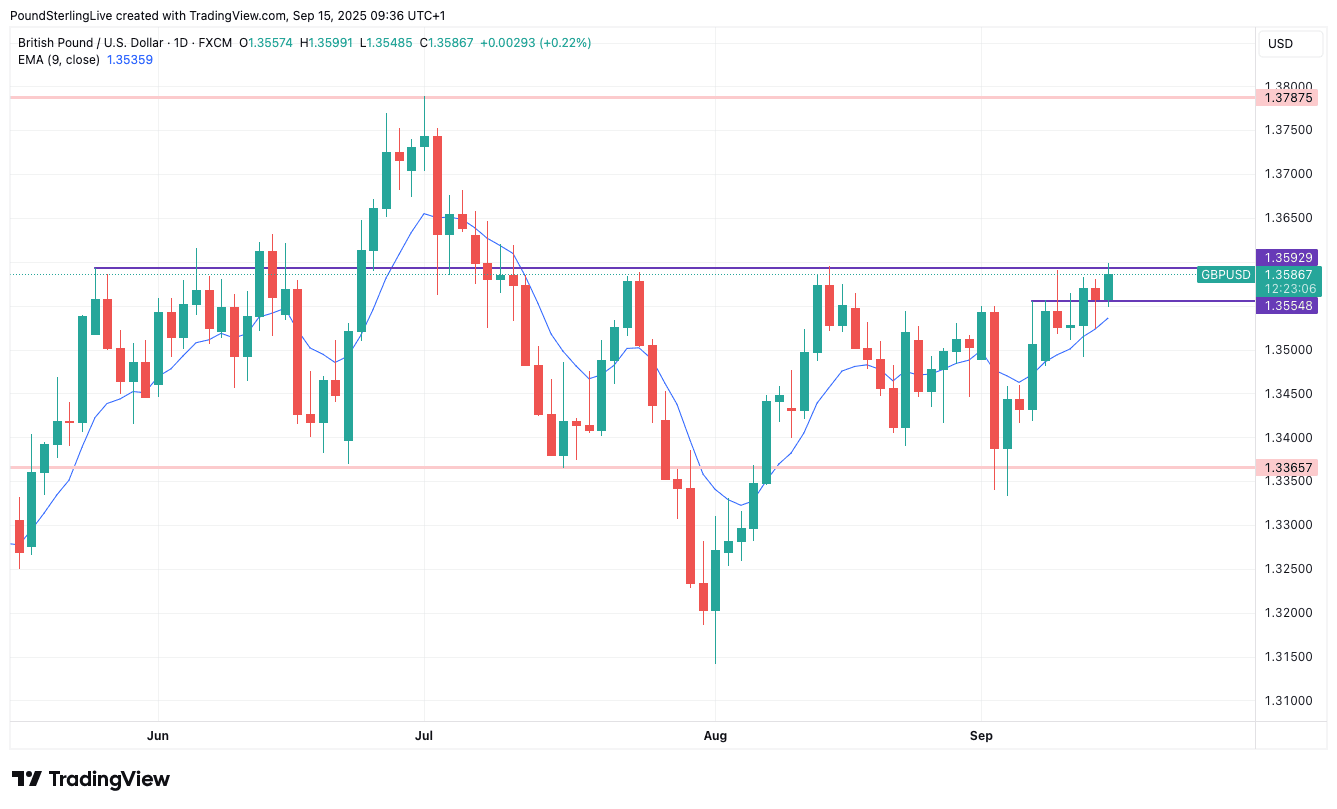

The pound to dollar exchange rate (GBP/USD) enters a pivotal week with some positive momentum thanks to expectations for a Federal Reserve rate cut on Wednesday, putting a test of 1.3594 and then 1.3631 in scope for the coming days.

Having fallen sharply at the start of September, GBP/USD has steadily recovered and has since moved above the monthly open (at 1.3489) as it became clear the Fed was approaching the start of a new cutting cycle.

Gains take the pair to 1.3590 at the time of writing on Monday, placing it above the nine-day exponential moving average (EMA) at 1.3529, which advocates for further near-term gains on a technical basis. (Set your automatic order here).

1.3590 is an interesting point in the recovery as it forms the top of a range that goes all the way back to May. Sure, the pair has traded above here previously, but only for nine days, suggesting the air is pretty rarefied in these climes.

Simply put: this is a notable resistance zone that could scupper the rally if this week's UK data falls on the wrong side of expectations and the Federal Reserve strikes a 'hawkish' tone.

It's a big week for the UK, with a central bank decision on Thursday which will be preceeded by inflation and labour market data, to be followed by retail sales and public finance figures.

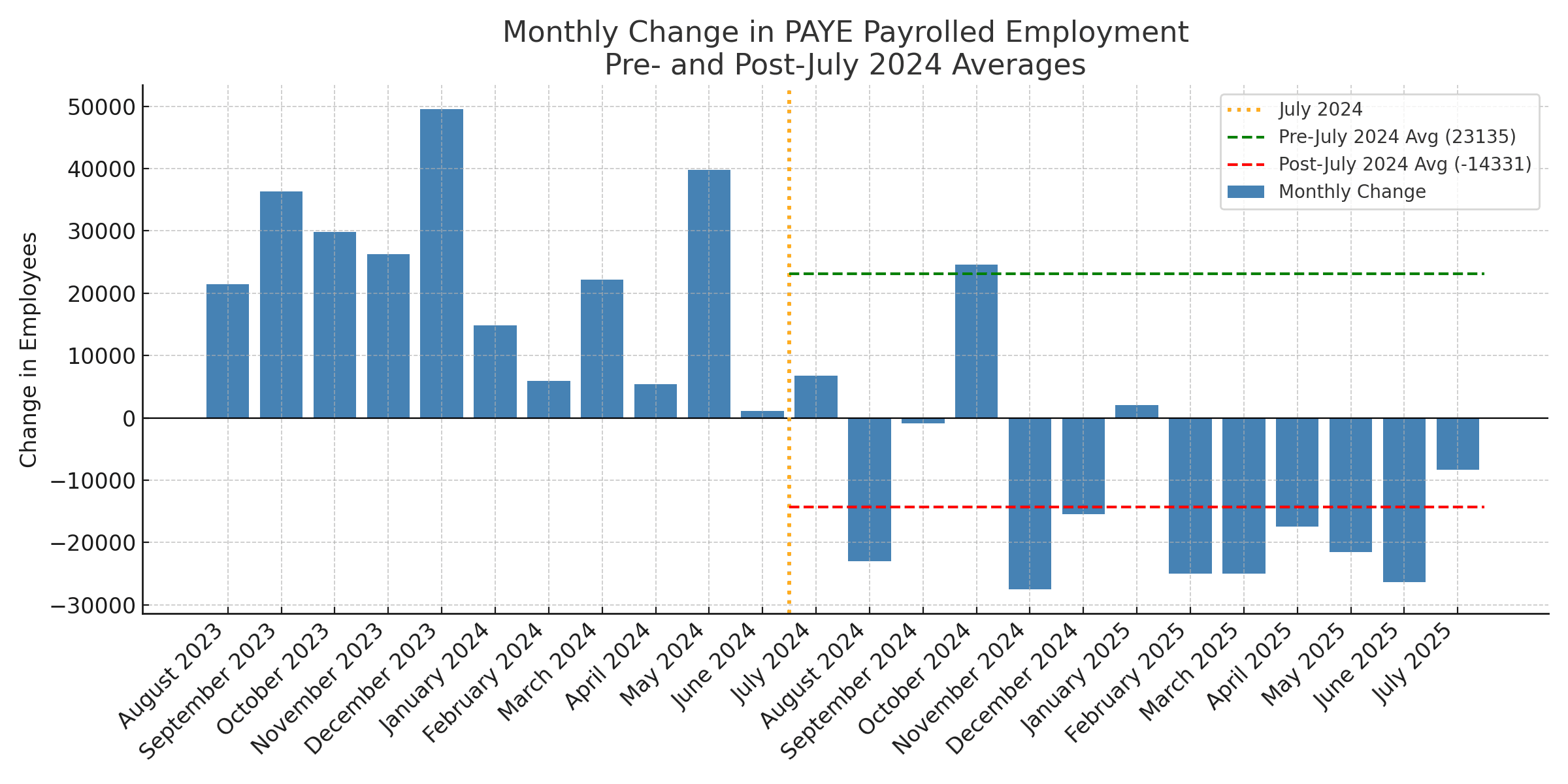

Tuesday's labour market statistics will likely show a further deterioration in payrolled employment and slowing wage pressures, all of which should lean on the pound as it would encourage the market to raise odds of a future Bank of England interest rate cut.

The key number to watch will be average earnings, which are expected to rise by 4.7% y/y; anything below here can weigh on the pound and anything above can give it a boost.

However, given that the UK's employment data has become highly unreliable, we imagine any GBP reaction will prove limited, with markets storing their gunpowder for the following day's inflation print.

On Wednesday, UK CPI inflation for August is expected to remain steady at 3.8%, in line with the Bank’s forecast, yet still well above the 2% target.

The inflation data follows the release of the Bank of England's inflation expectations survey on Friday, which saw a worrying pickup in medium-term (the 5-year ahead expectation), which rose 0.2ppts to 3.8%. This suggests the public sees no hope of the Bank of England reaching the 2.0% target for the remainder of the decade.

Above: Jobs are being lost, according to the PAYE measure of employment.

High inflation expectations beget inflation-creating behaviour amongst workers and businesses, which is why the Bank will worry about these numbers.

Given this, it's little wonder that there won't be a rate cut on Thursday. Instead, the question becomes whether the Bank thinks it is appropriate to cut in November.

Market pricing shows investors don't expect a November rate cut either, owing to the direction of travel in inflation; the Bank of England's Governor Andrew Bailey recently said there is "now considerably more doubt about exactly when and how quickly we can make those further steps" on cutting rates.

This should mean Thursday's rate decision offers minimal fuel to fire up rate bets, ensuring UK short-term interest rates remain well supported relative to those in the U.S., where interest rates should be cut midweek.

Indeed, it is the Federal Reserve that ultimately holds the keys to future direction in Sterling-dollar.

The Fed should kick off the next round of rate reductions with a 25 basis move on account of the economy's deteriorating labour market. Although inflation is higher than the Fed would like, there has not yet been any worrying evidence that tariffs are pushing up prices in a worrying fashion.

This means the Fed will be inclined to respond to a run of soft labour market figures, hoping that rate cuts can support employment.

For the dollar, the beginning of a new cutting cycle should imply weakness.

It is for this reason that GBP/USD can steadily climb and test the 2025 high at 1.3787 later in the year.

Risks to the view is Federal Reserve guidance that implies further rate cuts cannot be assured on account of inflation. Here, the dollar could unwind recent weakness and that resistance zone we spoke above earlier comes into play, pushing GBP/USD below 1.3555 again.