One analyst warns USD strength won’t last forever.

The Fed cut rates by 25bp and signalled QT ends on 1 December 2025, with MBS prepayments to be reinvested into Treasury bills Fed statement.

Dollar supported by a hawkish tone – Powell stressed the Fed is not on a preset path and a December cut is not a done deal, with market pricing for December easing dropping to about 16bp.

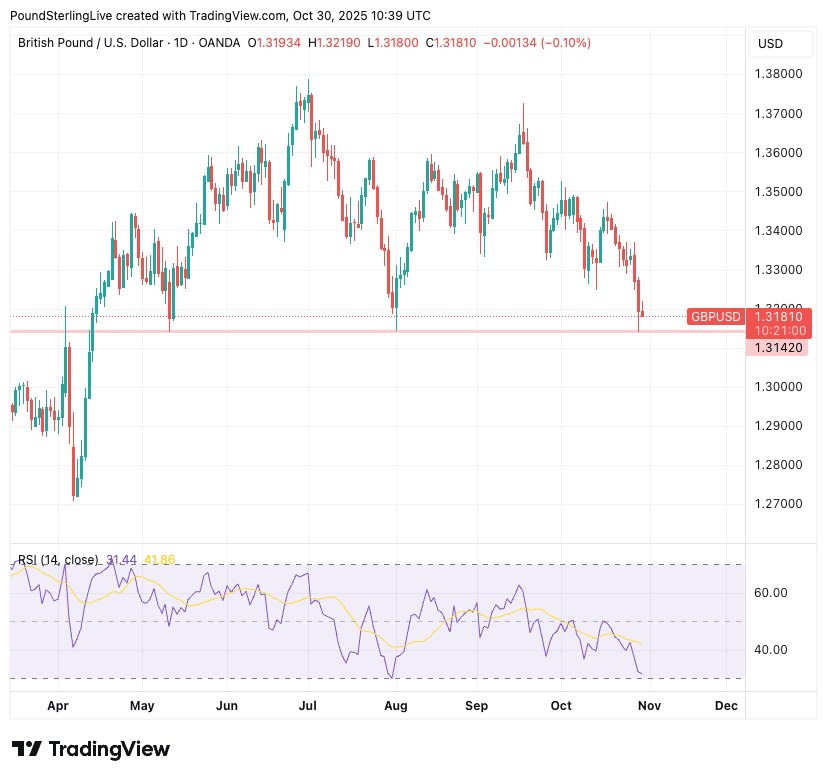

GBP/USD fell 0.60% on the day of the cut, sliding to 1.3142 at a significant support area read more.

The Big Surprise

The Federal Reserve delivered the widely expected 25bp cut and confirmed the balance sheet runoff will stop on 1 December 2025, with reinvestment into T-bills thereafter.

The message was more hawkish than markets anticipated – Powell said policy is data dependent and a December reduction is not pre-committed, which helped the dollar hold gains.

"The surprise was the extent to which Powell pushed back on expectations of a follow-up cut in December," says a reaction note from Lloyds Bank.

Driving the point home later in the Q&A part of the press conference, he added there was a "growing chorus now of feeling like maybe this is where we should at least wait".

For readers with near-term USD needs, it can pay to sanity-check pricing against market levels → request a quick dealing-desk quote to see if you can capture a better rate while momentum favours the dollar.

Tactically

GBP/USD is approaching oversold territory as the Relative Strength Index nears the 30 line, implying scope for a short-term rebound or consolidation to unwind stretched conditions. If you are executing during this window, a competitive quote can meaningfully improve all-in outcomes → compare with our desk.

Valuation

Survey of 30+ bank forecasts suggests GBP/USD is undervalued – if consensus plays out, a steady recovery into year-end is likely download report. If you are budgeting for transfers, locking a firm quote while spreads are favourable can reduce slippage → get a quote.

Tactical and medium-term outlook

TD Securities: “USD can hold on to recent gains for a little longer in the absence of US data and increased market focus on fiscal and electoral problems elsewhere. Structurally, however, the macro backdrop supports a USD decline, driven by US convergence to global growth and rates, waning safe-haven appeal, and rest of the world's outlook holding up.”

What’s next

Thin US calendar – with GDP delayed by the shutdown, focus turns to weekly jobless claims and any surprise fiscal headlines.

Fed cuts may keep the dollar firm near term – but with positioning stretched and GBP/USD near support, a tactical pause or bounce is plausible before the next trend move.