Image © Adobe Images

Energy price rises have turned into a headwind for the dollar.

The conventional wisdom is that the dollar benefits from surging oil and gas prices during crisis periods: it's a traditional safe-haven and energy is traded in dollars.

And that was the case at the outset of the Iran war; we saw the dollar advance strongly through the early stages of February, mirroring a surge in crude oil and gas prices.

But, of late, the dollar has cooled and has even managed to lose its war advantage against some currencies, despite oil staying elevated.

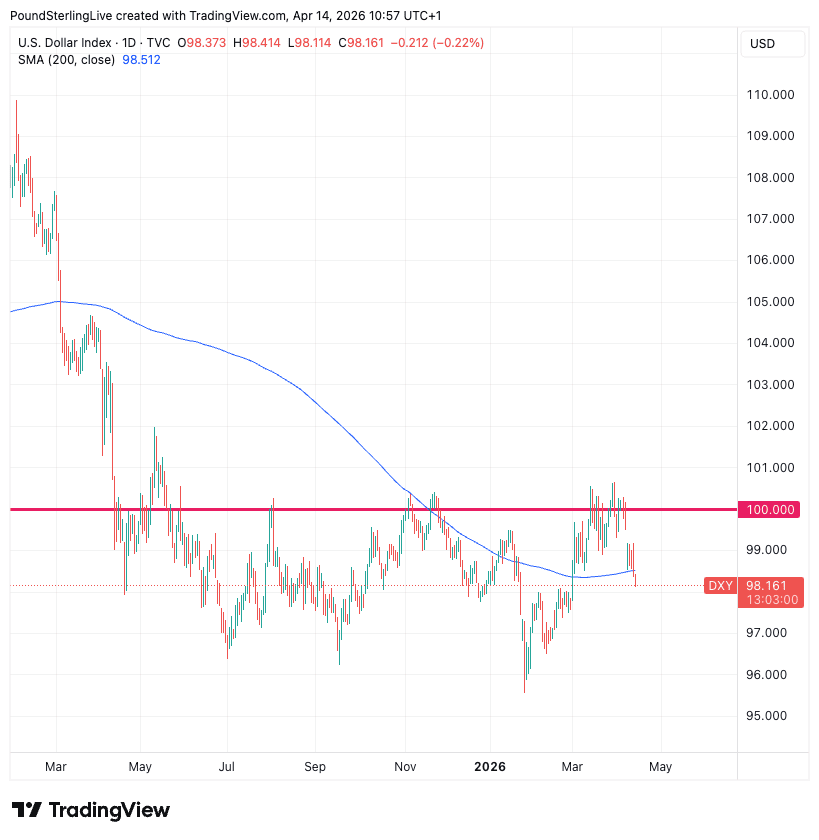

Indeed, GBP/USD is now above pre-war levels.

Currency analysts at Barclays have looked into the situation and find that "the emergence of a path towards the new geopolitical normal in the Middle East has turned energy prices from a tailwind to a dollar headwind."

In a weekly research note, analysts say the dollar index - a measure of broad USD performance - has moved approximately 1.0% lower for every 10% drop in oil since early April:

That's "a somewhat larger beta relative to the response to higher oil prices," they say.

Analysts say the behaviour could be due to stretched dollar longs per our sentiment indicator, or because the FX market is envisaging further energy price normalisation, or a reflection of the dollar's now-sticky risk premium.

"Further geopolitical stabilisation, a shift of focus towards the administration's domestic agenda and new Fed leadership likely imply further softness in the near term, per our new forecasts," says the note.