Credit : ILO/Apex Image. Source.

The pound-to-dollar exchange rate outlook is looking increasingly bearish as the Fed narrative shifts.

The dollar rose after producer price inflation (PPI) smashed through expectations to signal inflationary pressures are intensifying in America's economy.

April PPI rose by an eye-watering 1.4% m/m in April, nearly tripling the 0.5% figure the market expected. Core PPI, which strips out the effects of fuel and food, rose 1.0% m/m versus 0.3% expected.

"PPI just dropped a bombshell," says Naeem Aslam, CIO of Zaye Capital Markets. "This hawkish wake-up call is crushing Fed rate cut odds, igniting a powerful USD rally across the board."

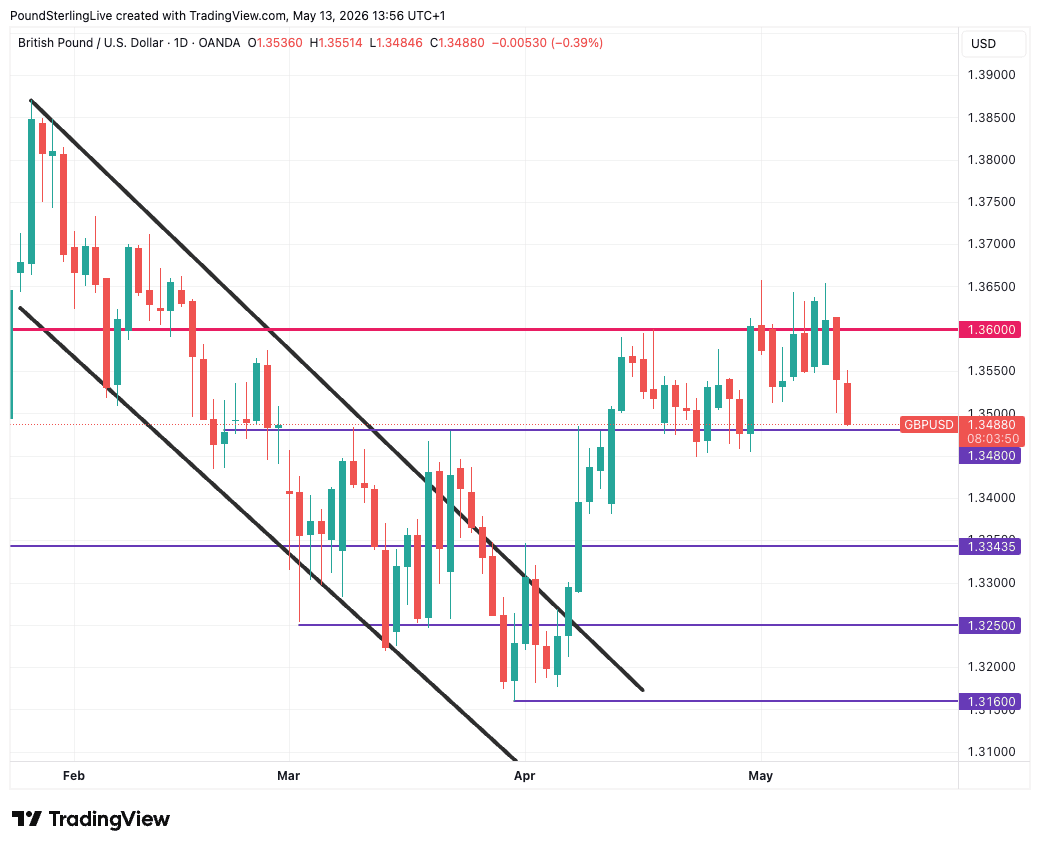

Above: GBP/USD tests the bottom of the recent range.

PPI is the inflation facing America's factories and is often considered a harbinger of what's to come for the more well-known CPI measure of inflation.

In the words of Chicago Fed President Goolsbee, "we have an inflation problem in this country."

The odds of a rate hike at the Federal Reserve this year have risen, and as one FX market strategist notes, this could represent the market regime shift that boosts the dollar.

"The most interesting regime shift for markets and macro traders will be if the market starts to price in Fed rate hikes. This will light a fire under the USD and FX and bond market volatility," says Brent Donnelly, analyst at Spectra Markets.

The pound-dollar conversions slid to 1.3493 in the wake of the PPI figures, extending a decline that followed the release of CPI inflation data just 24 hours earlier.

Headline CPI rose to 3.8% year-on-year in April, driven by surging energy prices linked to the Iran conflict and disruption through the Strait of Hormuz, which has tightened global oil supply and pushed fuel costs higher.

Core inflation surprised to the upside at 2.8%, confirming it to be truly stuck above the Fed’s 2% target.

It's hard to see how the market can hold onto the sanguine view that the Fed can afford to sit around and watch as price pressures burn hotter.

For the dollar, the setup is becoming increasingly constructive.

Analysis from Pantheon Macroeconomics, finds that although "inflation data are uncomfortably hot for the FOMC right now" it's probably still too soon for the Fed to panic.

"With the tariffs now fully passed through to consumer prices, rent inflation set to cool substantially, and the labor market no longer generating much inflation pressure, we think the run-rate of the deflator will slow."