Image © Adobe Images

A busy week of U.S. data will set the tone for the dollar.

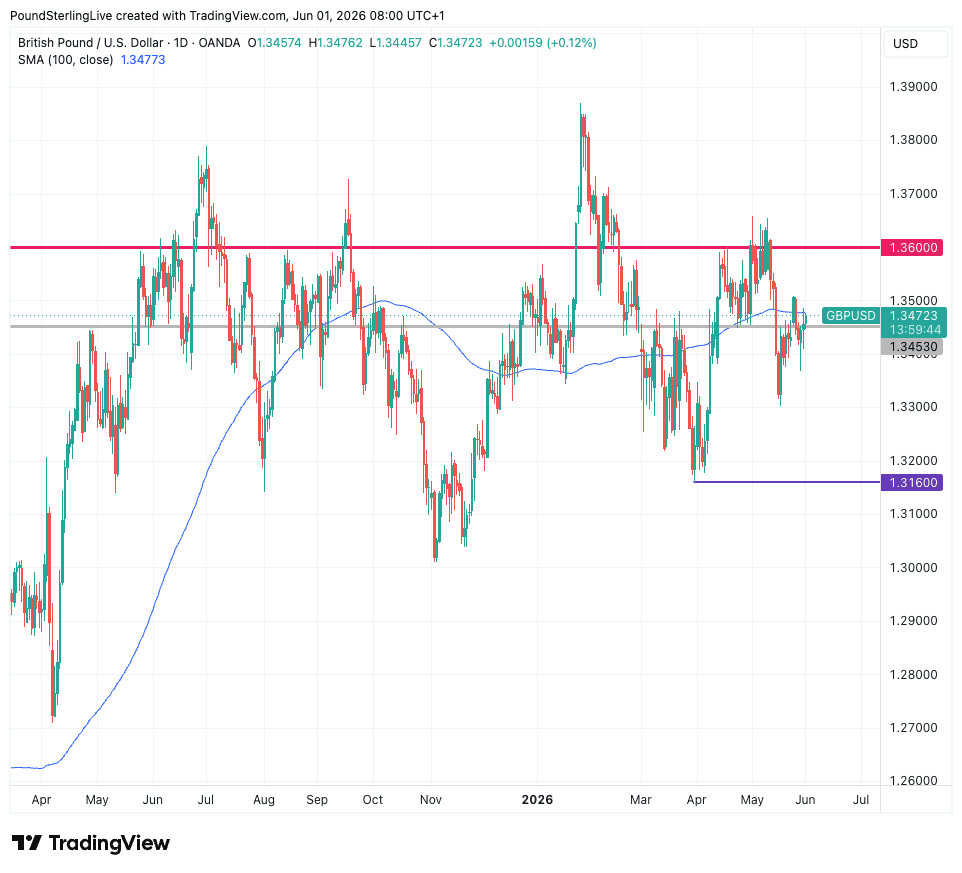

The pound to dollar exchange rate (GBP/USD) oscillates around its 100-day moving average near 1.3480 at the start of a new week that will be characterised by a steady flow of U.S. data:

ISM manufacturing (Mon), JOLTS (Tue), ADP, factory orders and ISM services followed by the Beige Book on (Wed), then Challenger job cuts (Thu).

Friday's non-farm payrolls is the highlight, with the market looking for 93k jobs to have been created in May.

The unemployment rate is expected unchanged at 4.3%, but the risks look lower if the payrolls gains show up on the household side.

The market will be looking for the data to offer fresh signals as to whether or not the Federal Reserve has scope to lower interest rates this year.

The dollar has firmed over recent weeks as solid data and rising inflation rates indicate there's limited opportunity to lower interest rates.

As rate cut bets fade, U.S. bond yields firm, which is, on balance, supportive of the dollar.

The broader structure remains constructive but not outright bullish. Since the April low at 1.3160, GBP/USD has formed a pattern of higher lows, and the recovery from the late-May dip indicates demand remains present beneath the market.

However, every attempt to establish a foothold above 1.3600 has failed, leaving that level as the defining barrier separating consolidation from a renewed sterling uptrend.

The 100-day moving average is also noteworthy because it has flattened significantly over recent months. A flat long-term moving average typically reflects a range-bound market rather than a directional trend, which is exactly what the chart has exhibited since late 2025.

Until either 1.3600 or 1.3160 gives way, the market is likely to continue trading within broad boundaries.

For the coming week, the balance of probabilities points toward continued consolidation with a slight downside bias.

U.S. data aside, risk sentiment will be an important background driver, with eyes on progress in Middle East peace negotiations, given the dollar tends to benefit from setbacks to the process.

Sporadic flare-ups continue in the region, but the market is confident in the direction of travel; overnight U.S. President Donald Trump said talks with Iran over an interim peace deal will "work out well."

For pound sterling, there's no tier-one data to look forward to, although Andrew Bailey, Governor of the Bank of England, is in the frame, with three appearances planned.

He should give an updated view on what the Bank is thinking regarding inflation and the future of interest rates. Here, the message should be that the Bank expects inflation to rise in the coming months, but that it's been encouraged by May's undershoot in the inflation data.

With rate cuts off the table, the UK's yield advantage will persist, and that's supportive of GBP/EUR.

Bailey's scheduled appearances:

Tuesday 2 June (3:00 pm): Oral evidence to the Lords Economic Affairs Committee in Parliament.

Thursday 4 June (4:40 pm): Headline speech at the Investment Association Annual Conference 2026.

Friday 5 June (7:00 pm): "In conversation" with economists Ed Balls and Stephanie Flanders at the 250th Anniversary of Adam Smith's Wealth of Nations event in Kirkcaldy, Scotland.