Image © Adobe Images

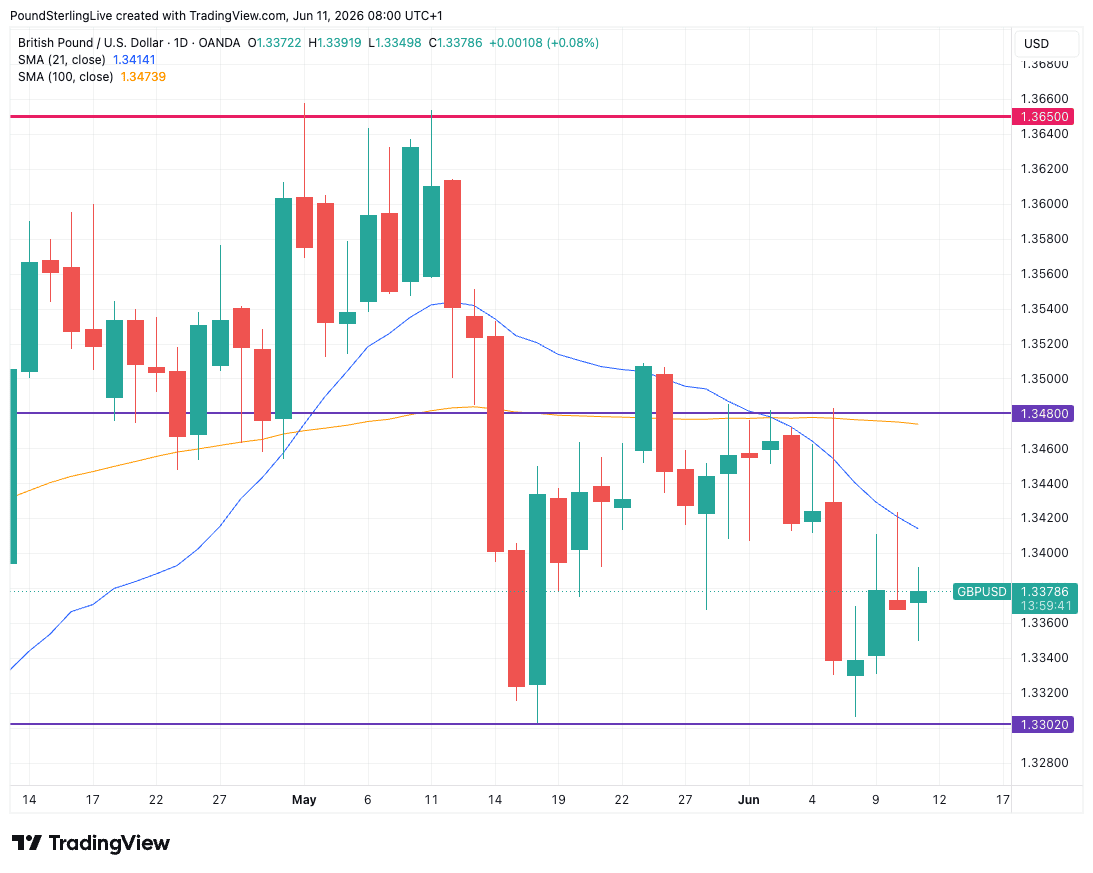

This week we've seen GBP/USD consolidate above 1.3320 and there are signs it could go higher.

The pound-to-dollar dropped notably last week in the wake of a run of stronger-than-expected U.S. data, and this week's U.S. inflation data met expectations at 4.2% y/y and confirmed inflation is running well ahead of the Federal Reserve's target of 2.0%.

Despite inflation being well above the Fed's 2.0% target the USD was softer after the report's release, because:

1) The market was primed for a stronger reading, given last week's run of above-consensus data

2) Core inflation was actually softer than expected at 0.2% (down from April's 0.4%).

3) Big rises in monthly inflation a year ago will drop out of the headline data in the coming months which will provide a solid ceiling for headline inflation in the coming months

Given this, it's hard to argue that U.S. inflation is running out of control, which challenges the building narrative that the U.S. dollar's cyclical powers are returning.

"There's really no sign - whatsoever - that U.S. inflation is overheating. That has implications for the Dollar," says Robin Brooks, Senior Fellow at the Brookings Institute.

"Just imagine what'll happen to inflation when the war ends and oil prices fall. I think markets are wrong to price hikes for the Fed. Very wrong," he adds.

Evidence that the inflation shock is contained will encourage the new Chairman of the Federal Reserve, Kevin Warsh, to defend the notion that rates should remain on hold.

Pushback against market bets for at least one hike before year-end would prove a headwind for the USD.

"In the scenario where Warsh continues to guide the market toward prolonged Fed rate hold or announces unorthodox changes

to the Fed, we would expect knee-jerk USD weakness to buckle the uptrend," says this month's just-released FX monthly note from TD Securities.

"Looking ahead, the likelihood of a longer period on hold has risen, but the balance of risks still tilts toward easing later this year as growth slows. Diminishing fiscal support and a weak real income backdrop are likely to weigh on household spending in the second half," says a note from the UBS Chief Investment Office.

On the charts, GBP/USD is now looking better supported in the wake of the above macro shift and sterling appears better insulated against downside.

A climb back towards the flat 100-day moving average at 1.3480 now becomes a feasible bet.

Geopolitics Flare-up Underpriced

What could challenge GBP/USD resilience is the situation in the Middle East, where there's a definite sense that the temperatures are rising again.

The U.S. and Iran have increased attacks over the past ten days and Thursday sees U.S. President Donald Trump warn he is ready to significantly ramp up strikes, and even take the important Iranian oil loading terminals on Kharg Island.

That escalation is a reflection of the President's growing impatience with Iran to agree a peace deal.

Despite threats to strike Iran tonight, oil prices are proving relatively well-behaved, which is keeping a lid on the dollar.

Is this a sign that key markets are getting their oil from elsewhere and the Strait doesn't matter as much as it used to? Or is it a sign of an impeachable belief that the conflict will end and the Strait reopen?

The risk is that traders are complacent and mispricing another flare-up which would send oil and the dollar higher and weigh on the GBP/USD.

"Markets aren’t buying into Trump’s threat. That could backfire," says Mathias Van der Jeugt at KBC Bank.