- "We worry this is brewing a major problem for the dollar" - Deutsche Bank

- U.S. readies to pass new Bill that will grow U.S. debt pile

- Concerns rise that foreigners are less willing to fund this debt

Above: House Speaker Johnson (right) is to push through new spending plans that will grow the U.S. debt burden. DOD photo by U.S. Navy Petty Officer 1st Class Alexander Kubitza.

Trump will preside over growing debt, which leaves the Dollar at risk.

Nervousness about the sustainability of U.S. debt financing is growing as the Trump administration prepares to implement measures that will increase the U.S. public debt burden, raising questions about who will fund it and how.

A risk is that foreign investors will struggle to absorb the huge supply of debt (bonds) required to fund the growing spending deficits. If this is the case, then negative financial market developments would ensue, scuppering investor sentiment and reinvigorating the "sell America" trade.

"As we approach the passage of a new fiscal stimulus and bigger tax cuts, we may see the SELL AMERICA theme return," says Brent Donelly, an analyst at Spectra Markets, who adds that the "structural USD down trade still makes sense."

House Speaker Mike Johnson is hoping to pass President Trump's "One Big Beautiful Bill Act" through the House next week.

The Bill rolls together numerous Trump objectives, including the extension of tax cuts, and economists point out this means the country will be no closer to shrinking its budget deficit under Trump.

In the UK, we would recognise it as the Budget the government puts forward every year.

The Bill will include measures to raise the debt ceiling by an astonishing $4 trillion, and economists estimate the measures could put the U.S. on course for a fiscal deficit of 6.5% of GDP in the coming years. Even before the new budget is enacted, total U.S. federal debt, now at its highest point since 1946, is on course to rise from about 100% of gross domestic product this year to 117% by 2034.

"Can the U.S. Treasury market continue to absorb increased supply and apparent indifference to rising deficits by the Trump administration? Much of the cost of this bill is merely to extend the status quo and other aspects could easily be crowded out by yields being higher than otherwise would be. That in our view means this development will not prove positive for the dollar," says a note from MUFG, the global investment bank.

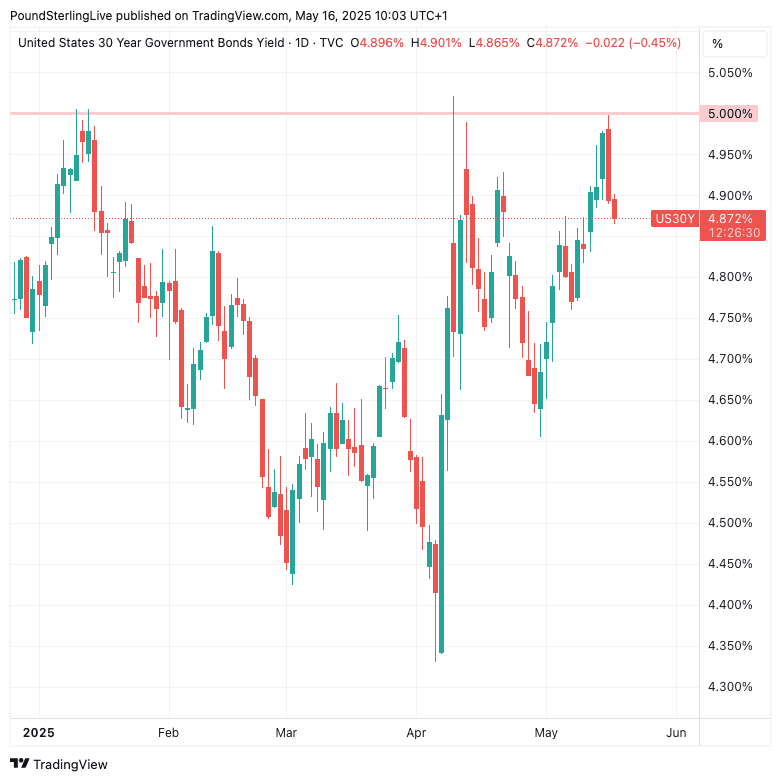

Nervousness is reflected in the rise in U.S. bond yields, meaning investors are demanding greater compensation for holding U.S. debt. This usually reflects investor concerns that inflation will eat away at the value of the bond (more spending = more inflation) and/or that debt is riskier to hold.

Above: The 30-year bond yield is elevated.

The 30-year Treasury bond is back near 5.0%, which represents a multi-year 'line in the sand' for this long-dated debt. The ten-year is also rising, although it is still some way below the year's peak near 4.8%.

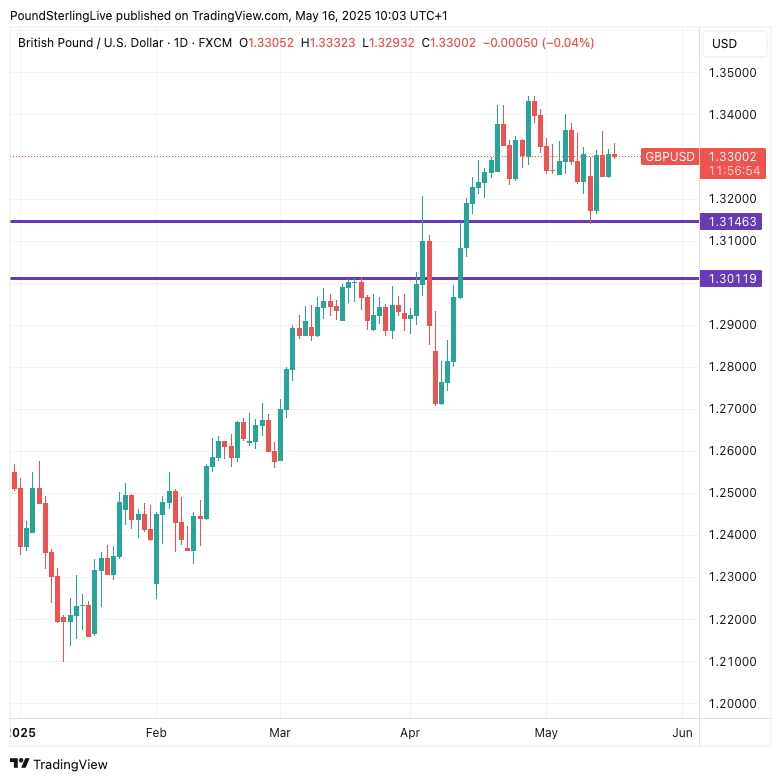

The Dollar has recovered through May, but the recovery has stalled even as bond yields rise, which would traditionally drive USD gains.

The stalled USD allows the Pound to Dollar exchange rate to reinforce support at 1.3146 and keeps open the prospect of further gains to 2025 highs.

Above: GBP/USD at daily intervals.

Expect more focus to fall on U.S. debt dynamics as the "One Big Beautiful Bill Act" makes its path through Congress, which can keep the U.S. Dollar nervous.

George Saravelos, Global Head of FX Research at Deutsche Bank, says in a new research note that because the U.S. budget deficit is expected to continue growing, the current account deficit won't be solved by raising import tariffs.

The current account is effectively the U.S. bank balance with the rest of the world, and it is in deficit because strong domestic consumption means that the U.S. needs to be a net importer to satiate the demand.

This would typically leave the Dollar lower, but demand for U.S. assets, including debt, means the U.S. can sell enough of those assets to foreign owners to fund its deficit.

Saravelos points out that for the current account deficit to close, the fiscal deficit must also close, as this would effectively diminish domestic demand for foreign imports.

However, the U.S. is moving forward with fiscal plans that will increase the deficit, necessitating that the U.S. continue to find willing foreign buyers to purchase its debt.

As long as this happens, the Dollar can stay supported, but the big risk is that concerns about the U.S. debt outlook undermine demand.

"We have been arguing over the last few months that the market is reducing its willingness to fund US twin deficits. This is arguably entirely reasonable given the expressed US desire to reduce them. But actions speak louder than words: the newsflow over the last few days aligns with the opposite outcome. We worry this is brewing a major problem for the dollar and potentially the US bond market too," says Sarvelos.