Image © Adobe Images

The Pound is the month's best-performing G10 currency.

The Australian Dollar has yielded further ground to the Pound and looks at risk of sliding further.

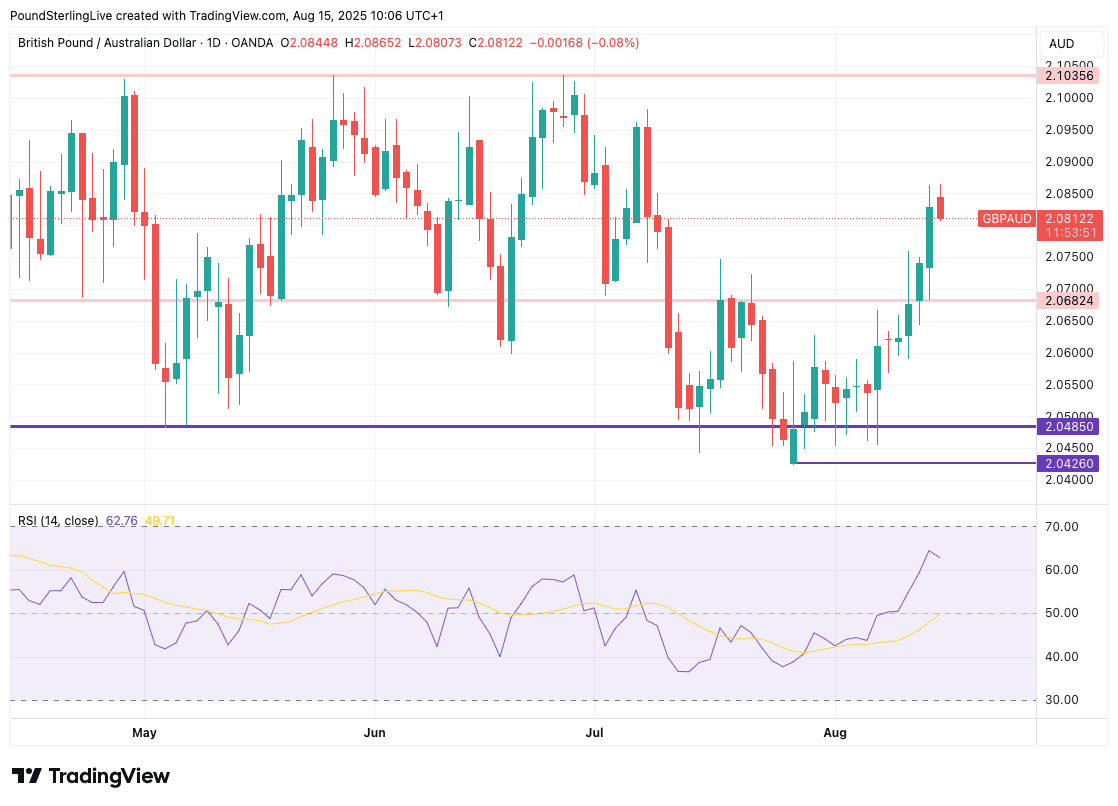

Following a consensus-beating UK GDP report released Thursday, the Pound to Australian Dollar exchange rate (GBP/AUD) rose to 2.0850, completing a breakout of a mini range that had trapped the pair for much of July.

"Sterling climbed to 1-month highs versus several major peers this week, including USD, EUR, CAD and AUD," says George Vessey, Senior FX Strategist at Convera. "Domestic data has led to a hawkish repricing of Bank of England policy expectations, whilst global risk appetite remains upbeat – helping the UK currency via the yield and sentiment channels."

"The pound continues to excel in G10 month-to-date," says Kenneth Broux, a strategist at Société Générale. "The pound continues to defy traditionally bearish seasonals in August... after stronger than forecast UK 2Q GDP. Flattered by government consumption, the economy expanded 0.3% qoq."

GBP/AUD is lifted above 2.0682, which forms the top end of a consolidation range that set in through late July. The move above here lifts the exchange rate back into the broader 2025 range, where we see the next target as being the range top at 2.1035.

Momentum is on the Pound's side, with the Relative Strength Index (RSI) point higher and now residing at a bullish reading of 62.

"For the time being, we think the GBP can outperform against peers on a total return basis thanks to its attractive carry proposition. Risks stemming from the dire fiscal situation and potential FX-rates decoupling in the future make us more cautious in our outlook, however," says Constantin Bolz, an analyst at UBS Switzerland AG.

The Pound's rally was triggered last week by the Bank of England's interest rate cut that came with the provisio that further cuts were not guaranteed at this stage, on account of the UK's elevated inflation rates.

The repricing away from further rate hikes has naturally bolstered Sterling.

At the same time, the Australian Dollar found the Reserve Bank of Australia's Tuesday decision unhelpful; the Bank delivered a cut but adopted a distinctly more 'dovish' tone that indicated it was open to further cuts.

The Aussie was meanwhile unable to capitalise on news that domestic employment rose 25k m/m in July, a solid increase, that met consensus expectations.

This marks a welcome return to growth after a run of softer-than-expected outcomes, including only +1k in June (revised down a from +2k).

"The trend of employment growth in recent months is still relatively soft, with the 3-month average up only 8k," points out George Tharenou, Economist at UBS.

The RBA will likely feel its softer turn on Tuesday is justified by signs that the labour market remains lacklustre and unlikely to present the kind of wage growth required to drive inflation higher.

For AUD, this suggests lower interest rates in the future, which diminishes its carry attractiveness. (Carry is where investors borrow where interest rates are low and divert it to where interest rates are higher, to pick up a profit on the increased yield.)