Prime Minister Carney's new economic initiatives could help turn the tide in CAD's favour. Picture by Simon Dawson / No 10 Downing Street.

The Canadian Dollar is having a rotten year, but is it time for the tables to turn?

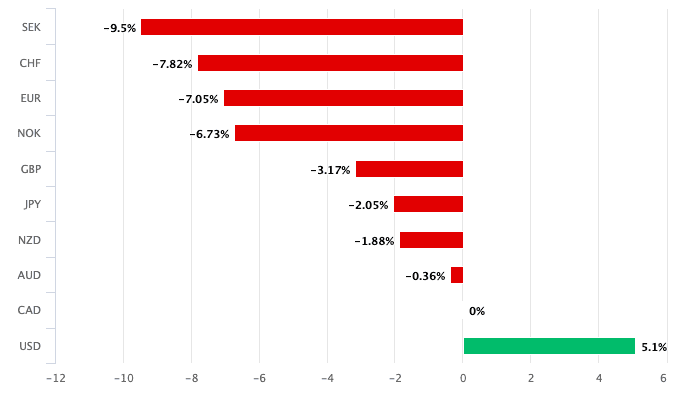

The Canadian Dollar is primarily being weighed down by the U.S. Dollar's ongoing slide, showing that having a bad neighbour can drag down the value of the whole neighbourhood.

The two North American currencies are firmly occupying the bottom two rungs of the G10 scoreboard, confirming that in the current epoch, what's bad for the U.S. Dollar is bad for its northern neighbour.

"The greenback—the primary determinant of the loonie’s value," says Karl Schamotta, market strategist at Corpay, confirming that the outlook for the U.S. unit will determine whether the Canadian Dollar will begin to reclaim lost value against its peers.

Schamotta, who works for one of the world's biggest payment firms, thinks this could be the case. In a market note released on July 09, he explains that the U.S. Dollar should "find its footing in the coming months."

The Dollar's selloff in 2025 has been a particularly difficult one to argue against, but there are some factors that suggest that it's time to put the selloff on ice.

Schamotta thinks hopes for aggressive Fed easing will be disappointed, which would imply interest rate markets will evolve in favour of USD strength. This would be particularly pertinent should foreign exchange markets begin to refocus on the interest rate differential between various economies and blocs.

Also, "shifts in hedging behaviour among real-money investors outside the United States run their course," says Schamotta. Foreign investors have been selling Dollars as part of the process of purchasing FX market products that protect their investment against further Dollar weakness.

This behaviour makes USD weakness a self-fulfilling prophecy. If the hedging demand fades, so too will that important source of momentum.

A major source of U.S. Dollar weakness this year has been President Donald Trump's tariffs, as investors see import tariffs as being negative for the domestic economy.

However, the Dollar has shown itself relatively sanguine to this week's barrage of tariff headlines, leading some to suggest tariffs are losing their ability to drive USD weakness much further.

Analysts at Royal Bank of Canada meanwhile point out some additional near-term drivers to consider:

1. U.S. Tariffs were a legitimate surprise in April. Now they are a refresh.

2. Dollar positioning is radically different than in April

3. U.S. rates are selling off on the announcement (in April they were rallying)

4. U.S. short-end rates are paring back from four cuts (April) to now two cuts expected end-2025, keeping US$ hedging costs elevated

5. U.S. economic data has been positively surprising recently

6. U.S. Stocks are once again outperforming

None of this is to say tariffs won't be bad for the economy: of course they might, and some economists we follow point out that it would be foolish to think otherwise. After all, they are still yet to be implemented.

But we could certainly be entering a spell of USD recovery, which would benefit the CAD greatly.

Also, there are some reasons to be more constructive on the Canadian Dollar due to supportive idiosyncratic developments.

"The outlook for the Canadian economy has turned far more optimistic in the past few months as last year’s Bank of Canada cuts have translated into an easing in financial conditions," says Schamotta.

He adds that Prime Minister Mark Carney is pursuing a series of spending initiatives and competitiveness-boosting measures, and effective US tariff rates have declined from the levels threatened in early February.

"Market participants have pushed rate cut expectations further into the autumn months in the belief that the Bank of Canada will avoid pushing rates further below neutral levels in the near term," adds Schamotta.

Should interest rate differentials start to play an increasingly important role in FX, then CAD would stand to benefit, particularly against currencies belonging to central banks that are looking to accelerate the pace they cut rates.