Image © Adobe Images

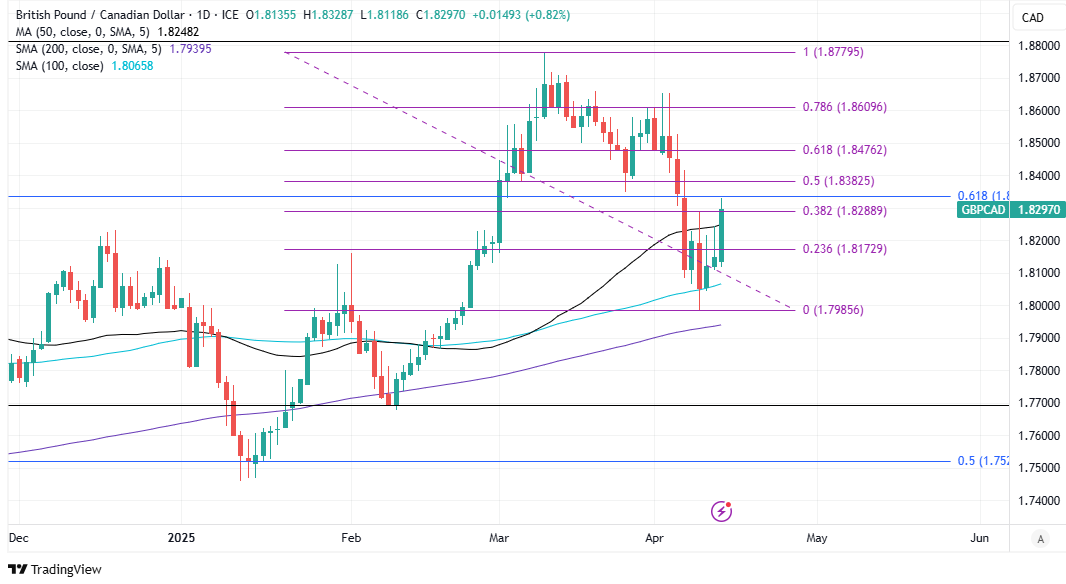

The Pound to Canadian Dollar rate rose back in the direction of post-Brexit highs last week, from near two-month lows, but is now approaching a series of resistances spanning the gap between 1.8338 and 1.8814 on the charts, some of which could slow, hinder or perhaps even halt the rally up ahead.

GBP/CAD fell back near two-month lows around 1.80 last week as the US Dollar fell against all of its advanced economy counterparts amid an exodus from American stock and bond markets, which favoured current account surplus jurisdictions such as the Euro Area, Switzerland, Japan and Canada.

The pair has recovered off its lows since the White House announced a reduction to its global reciprocal tariff to 10% and a 90-day delay to its implementation, while also raising the US levy on imports from China to a potentially market-closing 145%, in a policy move that brought only short-lived relief to US assets.

“We think that any USD moves will take precedence over CAD fundamentals,” says Noah Buffam, a strategist at CIBC Capital Markets. “CIBC Economics is calling for a 25 bps cut from the BoC this week, against consensus and market pricing.”

Above: GBP/CAD shown at daily intervals with Fibonacci retracements of various downtrends indicating possible areas of technical resistance. Click for closer inspection.

Monday’s rally in GBP/CAD was accompanied by co-movement with GBP/USD in the European morning hours, suggesting the intraday bid was part-funded by a Canadian Dollar that often goes unnoticed by many as a stalwart source of support for Sterling.

However, much about price action in the Loonie up ahead likely depends on the trajectory of the broad US Dollar, Tuesday’s inflation report from Canada and Wednesday’s Bank of Canada interest rate decision. Consensus sees Canadian inflation unchanged around 2.6% year-on-year.

“Market bets for a cut have softened slightly but still reflect 8-9bps of anticipated easing. A hold and cautious outlook—policymakers will want a lot more clarity on tariffs, I think—may give the CAD a little more upward momentum,” says Shaun Osborne, chief FX strategist at Scotiabank.

“Net CAD shorts held by speculative, real money and institutional investors remain a sizeable USD20bn or so, suggesting some sizeable short-covering demand for the CAD could yet emerge in the event of a deeper slide in the USD,” he adds in a Friday look at the week ahead.

Above: GBP/CAD shown at monthly intervals with Fibonacci retracements of various downtrends indicating possible areas of technical resistance. Click for closer inspection.

Meanwhile, UK inflation figures out on Wednesday will be sure to impact Sterling one way or the other, while Tuesday’s employment data will likely be ignored due to its diminished credibility and lack thereof.

“Both pieces of data present downside risks to sterling,” says Chris Turner, global head of markets and regional head of research at ING. “For this week, the sterling story could be driven more from the macro side.”

The Pound underperformed last week as the Sterling bond market came under pressure alongside US Treasuries before both markets stabilised on Monday, however, the risk is that both Gilts and the Pound suffer on Wednesday in the absence of further meaningful progress on the inflation front.

This is in large part due to the Chancellor’s dogmatic adherence to a now-toxic set of self-imposed ‘fiscal rules’ - themselves being archaic relics of the European Union membership era - which risk leading HM Treasury into further spending cuts and economy-sabotaging tax increases later this year.