Image © Adobe Stock

But that window for gains could soon shut.

The Euro is under pressure as markets anticipate another French political crisis that will likely see Prime Minister Francois Bayrou fall on September 08, when the National Assembly will deliver a confidence vote on his government.

With the main opposition parties indicating they will vote against the government, efforts to lower France's national debt will be put on ice again while President Emmanuel Macron scrambles to cobble together another government, raising concerns amongst investors about the wisdom of lending money to the French government.

"Sterling for the time being manages to capitalise on the poor euro momentum," says Mathias Van der Jeugt at KBC Bank.

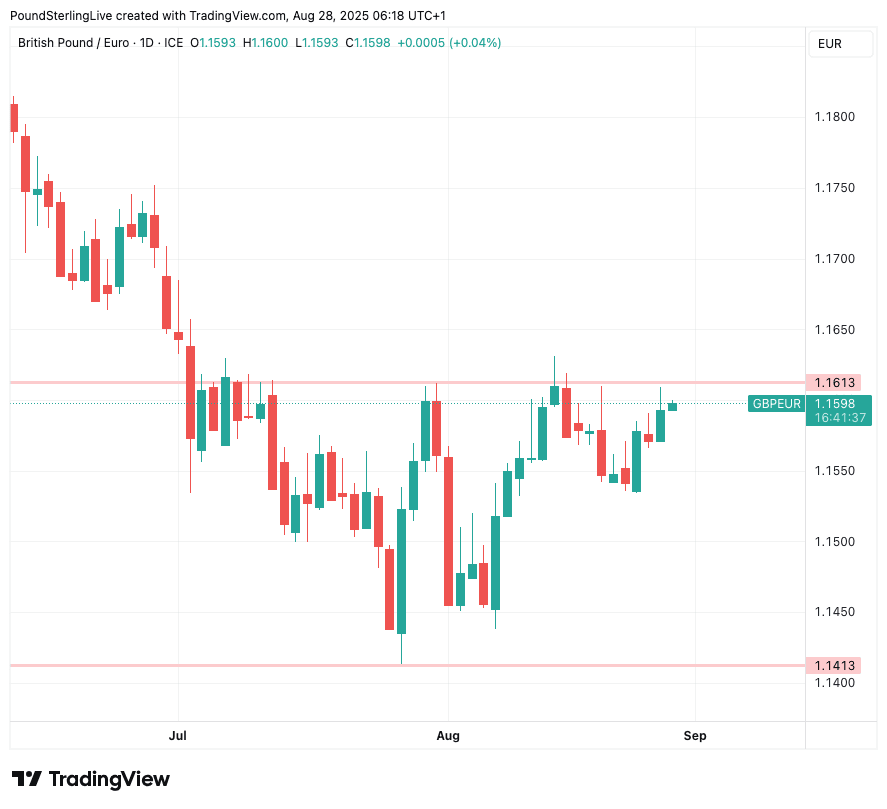

The Pound to Euro exchange rate (GBP/EUR) is back to 1.16 amidst the uncertainty and is looking to next test an important technical resistance area at 1.1613, ahead of a potential move to 1.1650.

Francesco Pesole, FX Strategist at ING Bank, says a test of 1.1630 remains possible, "even though our longer-term view is less optimistic on GBP given the possibility of a dovish rethink of BoE cuts later in the autumn."

Analysts say France won't trigger a full-blown crisis for the Euro similar to that seen during the 2010s, but it's creating enough uncertainty to allow euro buyers to book transfers at better rates. (Tools to do this can be found here).

For now, investor concerns are more apparent in French stock markets which have come under pressure this week, and in bond markets, where yields on French debt are rising faster than they are elsewhere.

Above: GBP/EUR at daily intervals shows gains are relatively contained.

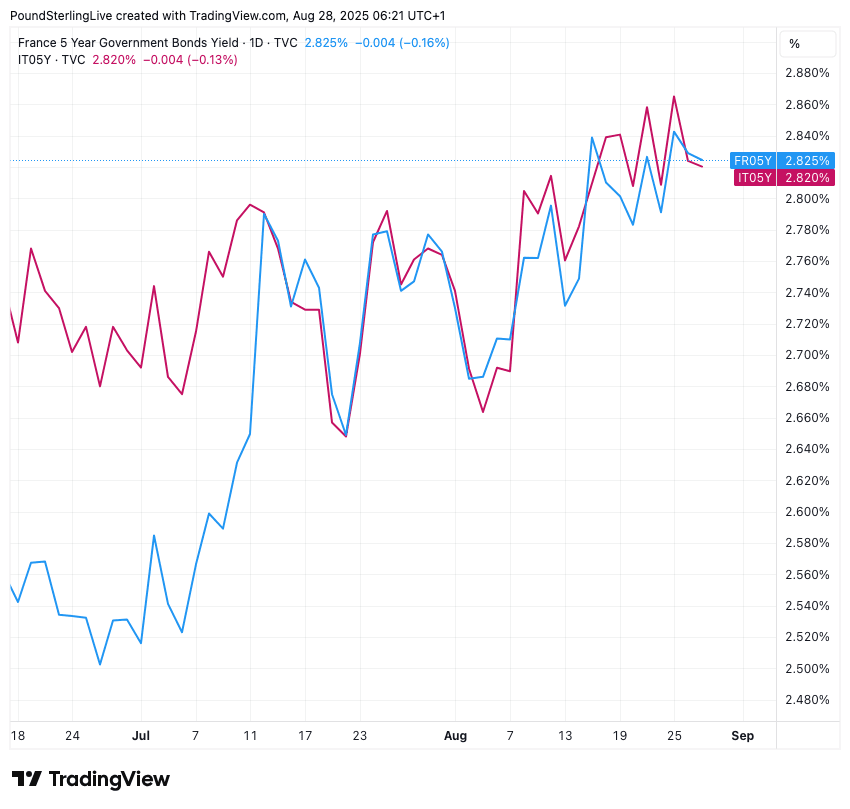

In fact, the interest rate paid by French bonds to investors is about to surpass that of Italy.

"I bet that within a fortnight, our debt will be costing more than Italy's," said France's finance minister, Éric Lombard on Tuesday.

Some French bond varieties, including the 5-year, already trade higher than their Italian counterparts. The gap between the important 10-year tenors of Italy and France is now down to just 5.5 basis points.

Above: French 5-year bond yields have already caught and surpassed its Italian equivalent.

Although losses in the Euro are still contained for now, analysts agree, should the cost of French debt rise beyond a certain threshold, Euro losses could accelerate.

"Wider European sovereign spreads still correlate with a weaker euro, even if the relationship is less significant than it was before Mario Draghi’s 'whatever it takes' intervention," says Kit Juckes, Head of FX Research at Société Générale.

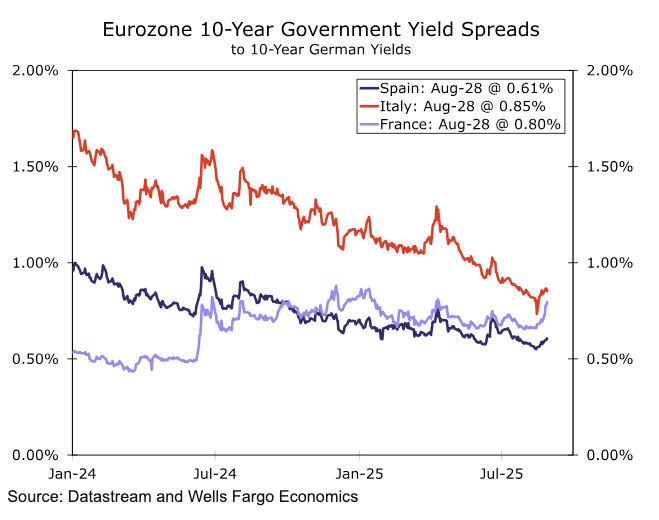

The difference between French and German debt yields is the more important benchmark to watch from a currency perspective, as it gives an indication that the premium on French debt is increasing relative to the safe-haven German bond:

Image courtesy of Wells Fargo.

Foreign exchange analysts say that when the spread between German and French bond yields rises to 90 and above, the Euro could react more forcefully and declines become more acute.

However, the crisis should be shorter-lived and the financial market more contained than it was in December 2024, when the previous government of Michel Barnier was ejected over similar circumstances.

The Barnier episode provided markets with a template to work from, meaning current uncertainty is less severe. Less uncertainty = less pressure on the Euro.

"Given the absence of generalised fiscal uncertainty across the Eurozone region, we also do not expect the latest French developments to have a long-lasting impact on the euro over the medium-term," says Nick Bennenbroek, an economist at Wells Fargo.

This should mean the Pound's window to advance against the Euro should be short-lived.

Analysts also point out that markets are already prepared for a worst-case scenario of the government failing, meaning the crisis could already be in the price of the Euro.

"We also note the 'bad outcome' is already a base case, which means the market impact is more likely to happen now - if at all - rather than on September 8," says Daniel Tobon, an analyst at Citi.

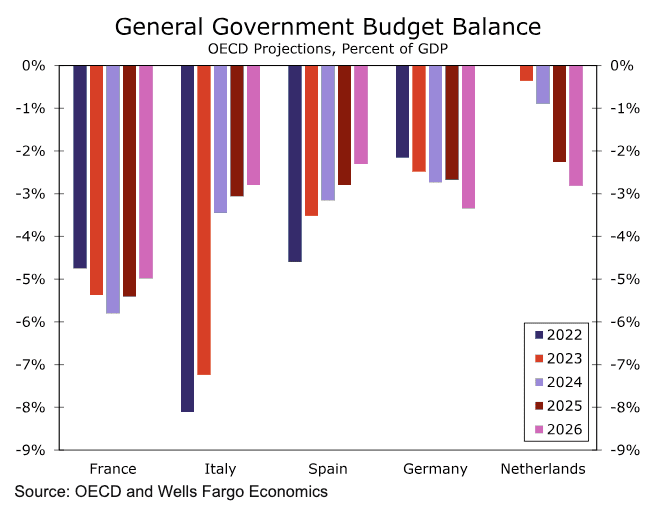

Above: France simply hasn't made the progress on reducing debt that other European countries have made. Image courtesy of Wells Fargo.

France's national debt reached a record €3,346 billion at the start of 2025, placing it as the third highest in the Eurozone, behind Italy and Greece.

Recent developments, including budget overshoots and political challenges, have exacerbated the situation, leading to a projected increase in the total French debt level to around 126% of GDP by 2030 from 113% at present.

In 2024, France's annual budget deficit was 5.8% of GDP, according to Eurostat data. This figure is significantly higher than the European Union's mandated limit of 3% of GDP for member states' budget deficits

Prime Minister Bayrou want to rein in debt by raising taxes and cutting spending in the 2026 budget. This plan aims to achieve €43.8BN in savings, but this is too much for opposition parties to stomach, and is why the budget is stuck in the National Assembly.

By calling a confidence vote, Bayrou seeks to pressure the opposition by conveying to French voters how unserious they are about grappling with the country's problems.

With Bayrou likely to depart, Macron will have to appoint a new Prime Minister, reappoint Bayrou, or call a new election.

"Expectations appear to be leaning towards the appointment of a new Prime Minister, perhaps by offering some budget concessions to opposition parties in exchange for their support," says Bennenbroek at Wells Fargo.

"A new round of elections would of course provide a more extended period of volatility," he adds.