Image © Adobe Images

The British Pound's short-term uptick will draw in the sellers, say strategists.

"We have even been asked if GBP is now a more attractive long against USD than EUR is, but I'd rather see this as a potential opportunity to sell GBP at better levels," says Kit Juckes at Société Générale. "An EUR/GBP break below 0.86 for the first time since late June would be hard to resist."

A EUR/GBP break below 0.86 equates to a GBP/EUR test above 1.1630, a level that Juckes thinks is particularly attractive to sellers.

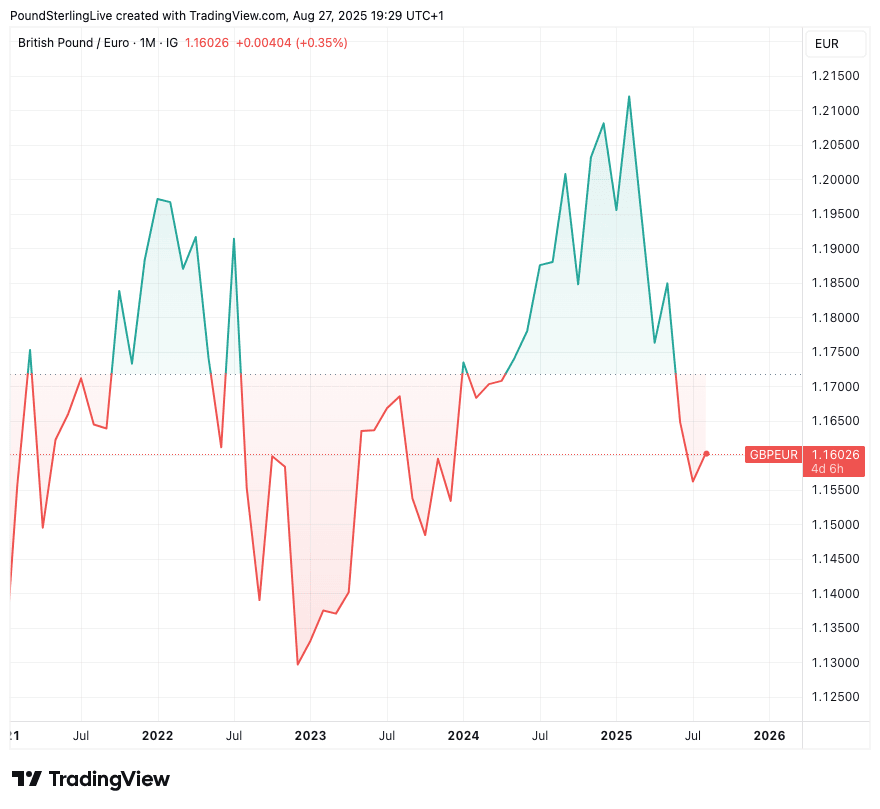

Having been as low as 1.1413 in late July, the Pound to Euro exchange rate has steadily recovered to 1.16 over the course of August, and could realise further gains in the coming days, particularly with renewed concerns about French politics.

France's government on September 08 faces a confidence vote in the National Assembly, and should the outcome trigger a market-unfriendly result, the door is held ajar to further Euro weakness.

However, currency analysts are looking through the noise and warn that this isn't a game-changing moment for the Euro, which will benefit from improving ex-France economic growth and the mighty backstop of the European Central Bank.

At the same time, the Pound's calm late-summer trade will be tested when Parliament reopens and market focus tilts to the November budget. (If you are concerned about future currency movements, lock in today's rate for use at a future date, or put in an order to nab any beneficail moves, learn how).

"As the UK Government prepares to increase taxes, inflation remains persistently higher than in the rest of Europe and growth remains anaemic, short GBP against the rest of Europe is an attractive long, medium and short-term trade," says Juckes.

The UK's high interest rates and a period of relative market calm have helped the Pound 'melt up' against the Euro through August, and strategist Francesco Pesole at ING says the balance of risks remains tilted to the upside for the pair in the short term.

He explains that the 'hawkish' repricing in Bank of England rate expectations has helped Sterling's cause. The shift takes the shape of a recalibration in expectations that followed the Bank's August 07 decision.

Above: After two years of gains, GBP/EUR has entered a period of weakness.

Markets now see less than a 50% chance of another cut before year-end, whereas another cut was a sure-fire bet at the start of the month.

To be sure, some economists still see November as a 'go', but last week's above-expectation inflation print suggests those betting for a pause will carry the day.

Normally, 'hawkish' repricing is a supportive development for the Pound and means the currency can eke out some gains against the Euro and other major currencies in the coming days and weeks.

However, the horizon for outperformance doesn't extend all the way to November, where the budget poses a significant risk.

The UK's deficit now stands at 5.7% of GDP, which is the 3rd highest among 28 advanced European economies. Total public debt stands at 94% of GDP, the 6th highest among advanced economies.

Unlike the U.S. and Eurozone countries, the UK has a small and open economy and financial system, that means it will get tested by bond markets before its peers. It can't afford to play loose with its finances.

It's for this reason that a smorgas board of tax hikes are being considered by the UK government, which should further weigh on growth and undermine the attractiveness of UK assets.

This could set the Pound up for a difficult final quarter to the year and underpins why some see recent gains as an invitation to sell.