August could see calmer sailing for the Pound. Image © Adobe Images

August could see some relief ahead of Autumn anxieties over the budget.

A spell of British Pound outperformance could be upon us, offering some relief to those looking to pick up foreign currency.

Gains against the Euro and Dollar are possible as the UK currency unwinds from oversold conditions that built up during the July selloff. "GBP is starting to look oversold," says Valentin Marinov, head of FX strategy at Crédit Agricole.

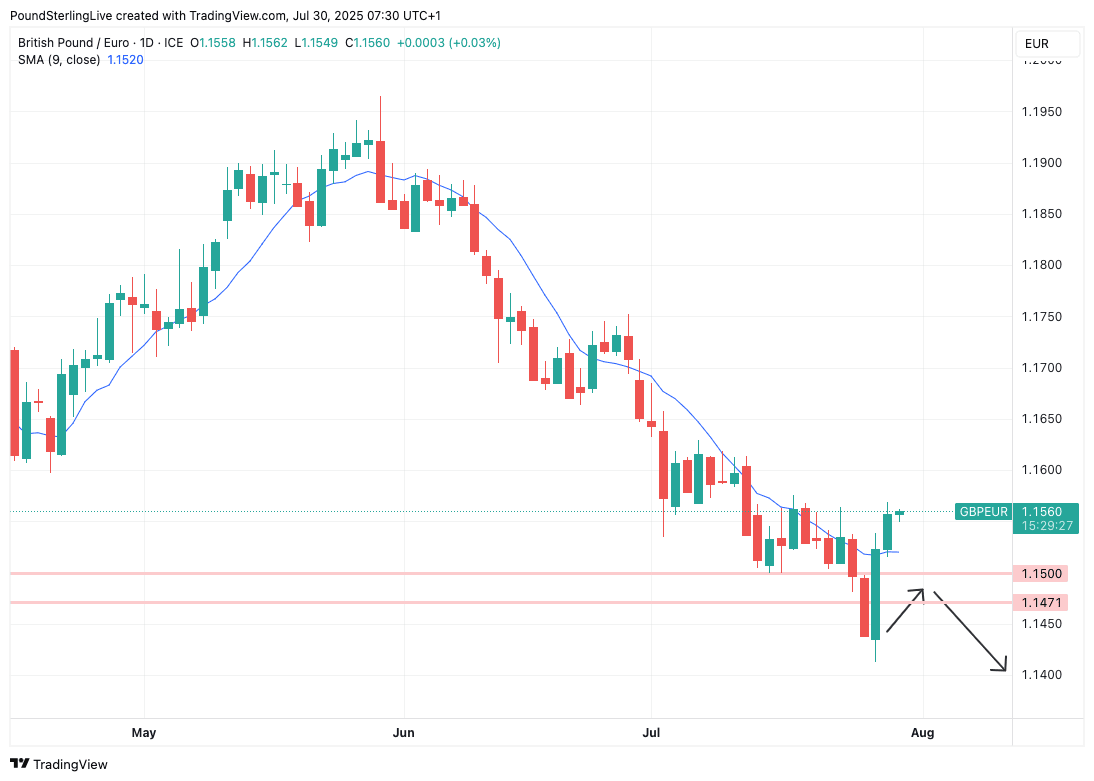

In a note released Monday, Marinov said the Pound was looking particularly cheap against the Euro, and we have subsequently seen the Pound to Euro exchange rate recover to 1.1562 from the week's open at 1.1435 by the time of writing on Wednesday.

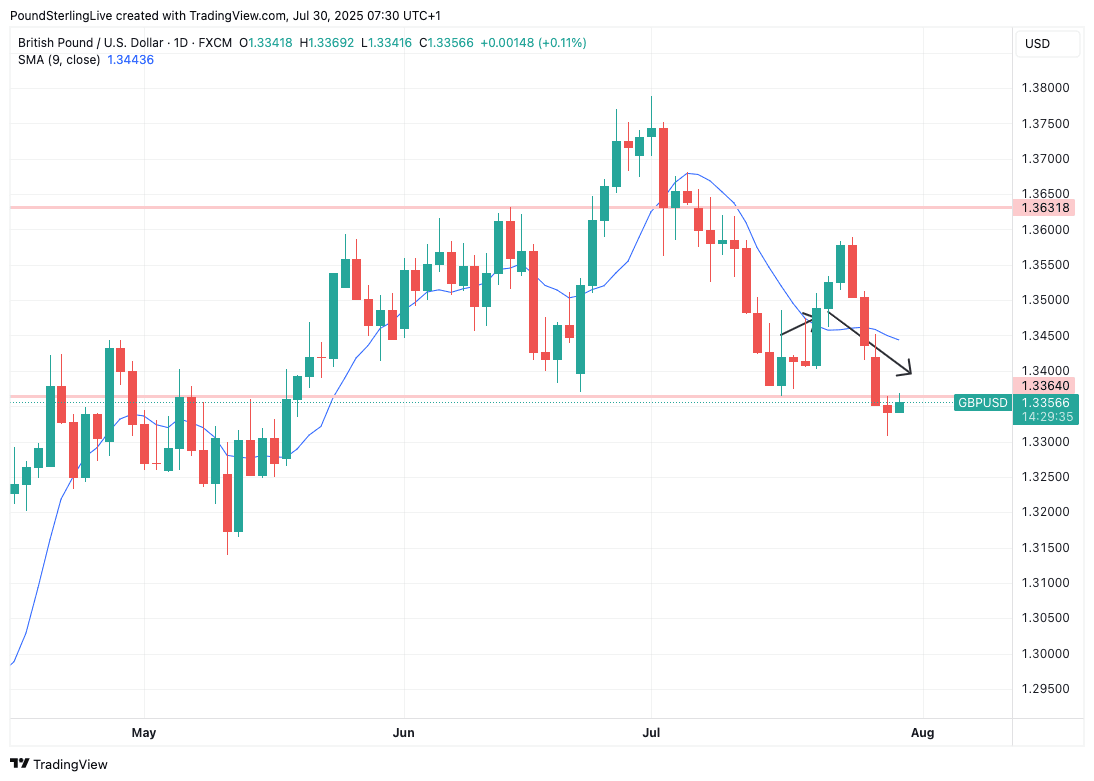

The Pound to Dollar exchange rate remains under pressure though, dropping to 1.3348 from the week's open at 1.3419.

Much will depend on what the bigger Dollar does now that U.S. trade tensions have faded, but it's worth noting the Pound is withstanding the current USD rebound better than the EUR and other currencies.

Strategists at Wall Street bank Morgan Stanley say in a recent note that they retain a bullish stance on the Pound, and "think GBP/USD can continue to rise."

Morgan Stanley thinks Sterling can benefit from the "highest carry-to-volatility in the G10." 'Carry' refers to the UK's high interest rates relative to elsewhere, which attract foreign inflows of capital, particularly when volatility is low.

Money markets show that expected market volatility in August is set to be lower than in recent months, partly on account of summer trading conditions and also easing global trade tensions, meaning the carry trade can perform well.

When carry is in demand, so too is the Pound.

Above: GBP/EUR performance and annotations made at the start of the week, showing the rebound to have been bigger than we predicted.

"With the next UK CPI not until August 20, that opens up a window for carry-seeking investors to add longs, fueling GBP support," says Morgan Stanley.

Weighing on the Pound during June and July was a build-up in bets that the Bank of England would need to cut interest rates again on numerous occasions. The market is now fully priced for two more cuts this year, whereas this was not assured just a month ago. It also looks like a final rate cut is priced in for early 2026.

The repricing has weighed on the Pound given the market is again starting to trade on interest rate differentials following the tumultuous resetting of U.S. trade and policy by President Donald Trump in H1.

"UK rates markets are almost fully pricing in a 25bp rate cut, followed by another two rate cuts by the end of 2026. The view is thus close to our own expectation for a terminal bank rate of 3.5% next year. We therefore believe that many BoE-related negatives are in the price of the GBP and do not expect the currency to extend its recent downtrend," says Crédit Agricole's Marinov.

Above: GBP/USD with our Week Ahead annotations, showing the pair is behaving as we predicted.

August therefore presents a window of potential calm for the Pound, but volatility in the currency could start rising again the closer we get to the Autumn budget.

The budget is currently slated for early November, but the Treasury will start airing its plans well in advance. These can cause jitters in UK money markets given growing concerns about the UK's debt profile.

We have seen periods where bonds and the Pound sell off in tandem, the classic tell-tale sign of debt worries, most recently when Keir Starmer abandoned plans to save money on welfare and Chancellor Rachel Reeves broke into tears in the House of Commons.

For now, though, this underlying tension is glossed over by the smoother summer waters. Those with GBP payment requirements should make the most of the calm sailing.