Image © Adobe Images

Plummeting business confidence underpins UK's economic malaise.

Investment intentions, headcount and revenues at British businesses are all expected to fall, according to a new business survey.

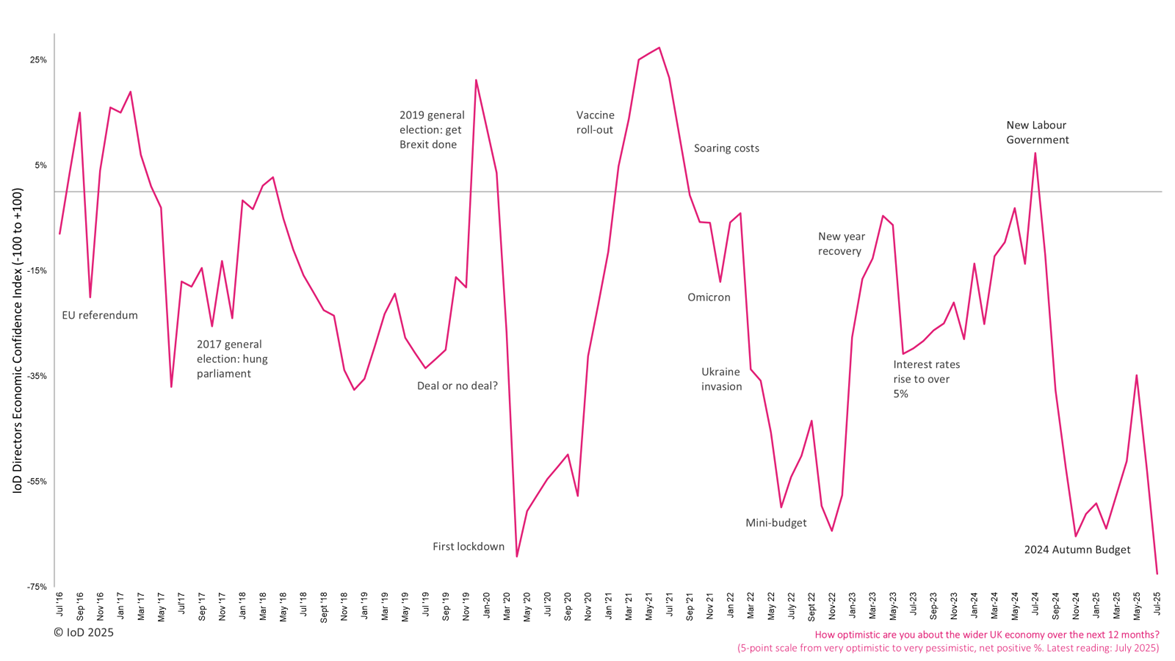

This is according to the latest edition of the Institute of Directors' Economic Confidence Index, which has fallen to its lowest level since inception in 2016 at -72, down from -53 in June.

"UK business leaders have entered the summer with the lowest confidence levels we've seen since our records began in 2016. Companies continue to battle cost increases – particularly arising from the national minimum wage and NI changes – and many are frustrated that while the government has been quick to raise costs for business, it has been much slower to deliver improvements to the wider business environment," says Anna Leach, Chief Economist at the Institute of Directors.

The findings shine a new light on the poor macroeconomic environment in the UK that will ensure the Pound will continue to struggle against the Euro and Dollar.

"The mood surrounding the pound has soured in recent weeks and dovish comments by BoE governor Bailey on the labour market and interest rates put investors on notice for potentially further losses ahead," says Kenneth Broux, a market strategist at Société Générale.

Although the Pound has recovered against the Euro over recent days, and low-volatility conditions during summer could offer further near-term support, headwinds could start to blow again in the Autumn when Chancellor Rachel Reeves delivers the next budget, that is likely to include further tax rises as she seeks to fund the government's staggering expenditures.

"Last year, damaging speculation around tax rises in the lead-up to the 2024 Budget caused many firms to pause investment and hiring decisions – contributing to six months of near-zero economic growth. We're now living with the economic consequences of those tax hikes," says Leach.

Business confidence is below Brexit and Covid levels.

She says the government must urgently calm business nerves by ruling out new taxes.

The IoD's survey showed business investment intentions fell to -27, from -10 and revenue expectations fell to -8, from +8. Businesses headcount expectations fell to -23, from -10, the lowest since November 2024.

The deterioration in employment intentions corroborates evidence elsewhere of growing downside risks to the UK's labour market as companies battle with the additional costs imposed by Reeves in last November's budget when she hiked National Insurance Contribution taxes on businesses.

"Survey respondents widely commented on the need to reduce headcounts in response to higher payroll costs and subdued customer demand," reported S&P Global in their latest PMI survey that covered the July period.

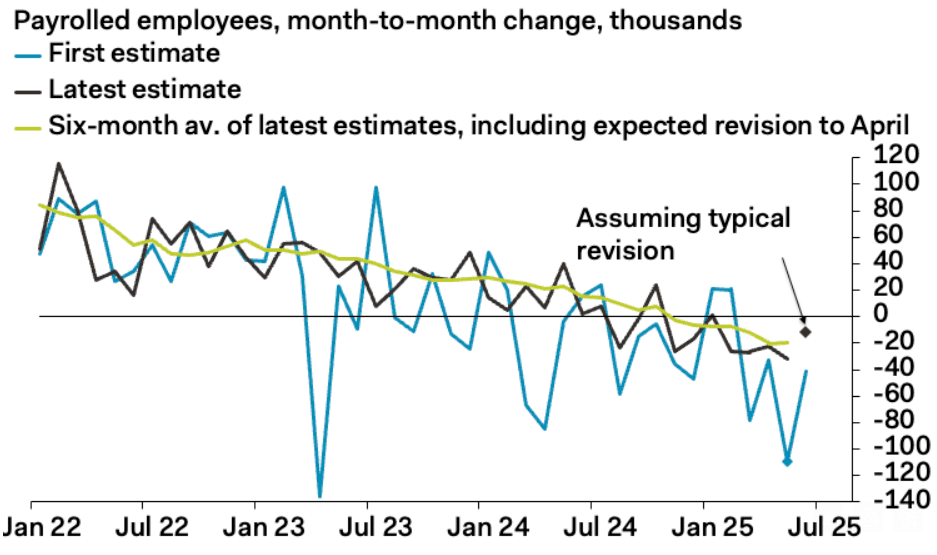

Above: Official data shows UK employment continues to fall.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, compilers of the PMI report, said what is particularly worrying is the sustained impact of the Budget measures on employment.

"The UK data dump over the past couple of days shows an economy running at half pace at the start of summer," says Kallum Pickering, Chief Economist at Peel Hunt.

These data show there is growing scope for the Bank of England to cut interest rates again when it meets next week. However, for the Pound and financial markets, it will be the guidance on what comes next that will matter.

Business surveys overwhelmingly blame Chancellor Rachel Reeves' tax raid on employers for falling employment rates. Picture by Kirsty O'Connor / HM Treasury.

If the Bank signals it will cut by more than the additional 50 basis points of cuts expected in the next six months, then the Pound can come under renewed pressure.

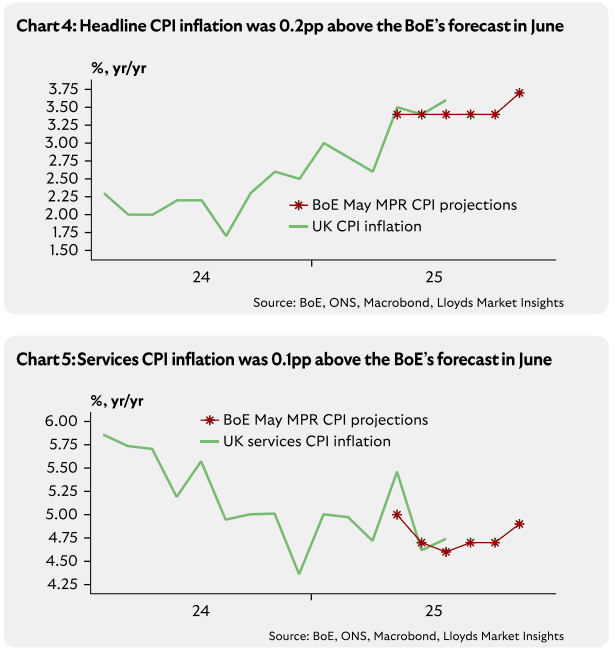

More cuts would be warranted given the travel in UK economic data, particularly the labour market. However, inflation remains stubbornly high, with food inflation surging again and all signs suggesting the Bank's long-predicted fall in inflation is still some way off.

The British Retail Consortium said on Thursday that food inflation has risen 4% year on year, and could reach 6% by Christmas.

Food inflation is particularly instrumental in forming consumer views on the outlook for inflation, which means it can set overall inflation expectations higher. This is something the Bank of England is particularly wary of, as elevated inflation expectations beget further inflation.

Images courtesy of Lloyds Bank.

This would argue against cutting rates too deep and too soon, for risk of completely shooting its own credibility.

In fact, economists at Pantheon Macroeconomics, the independent researcher, think there is only one more interest rate cut to come from the Bank of England owing to inflation persistence.

"Structural changes, principally deanchored inflation expectations and greater real wage resistance are supporting wage growth and price inflation for given slack in the economy," says Robert Wood, Chief UK Economist at Pantheon Macroeconomics.

The combination of deteriorating growth and elevated inflation creates an economic phenomenon known as stagflation. It is a difficult environment for central bankers to navigate as they are unable to provide support via lower interest rates for fear of stimulating inflation.

Higher interest rates would normally tend to support the Pound, however, poor economic growth means this might not be likely, particularly if the poor economy means the Treasury doesn't collect as much tax as was expected.

This would lead to more borrowing and increasingly regular episodes of bond selloffs as investors are unwilling to lend to the UK.

For the Pound, the ultimate risk is a fullblown UK debt crisis, which becomes increasingly likely as long as the country stays on its current trajectory.