Image © Adobe Images

Inflation undershoot opens door to dovish Bank of England decision, putting the pound under pressure against the euro, dollar and other currencies.

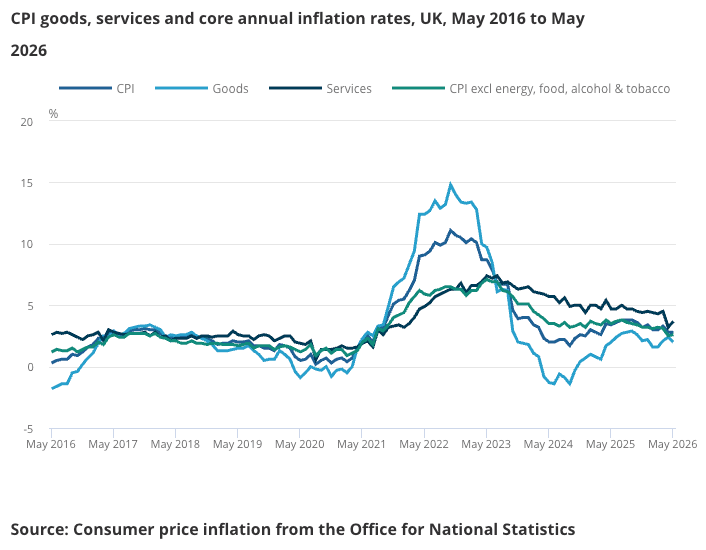

The ONS said CPI inflation held at 2.8% y/y in May; this was lower than a market consensus expectation for 3% and lower than where the Bank of England forecast it would land, as the Bank's April forecast anticipated headline would be 3.3% in May.

The core rate - which strips out goods and energy costs - rose to 2.6%, undershooting the estimate for 2.7%.

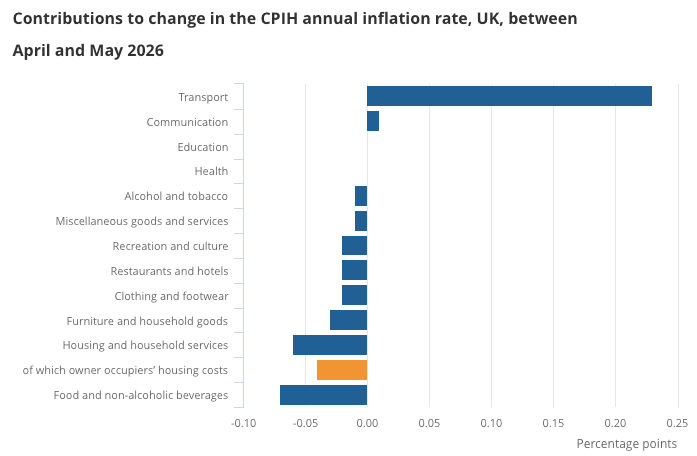

"The underlying picture is relatively simple: upward pressure from higher transport costs (mainly motor fuel and airfares) was offset by falls in inflation almost everywhere else," says Julian Jessop, economist and Senior Fellow at the IEA.

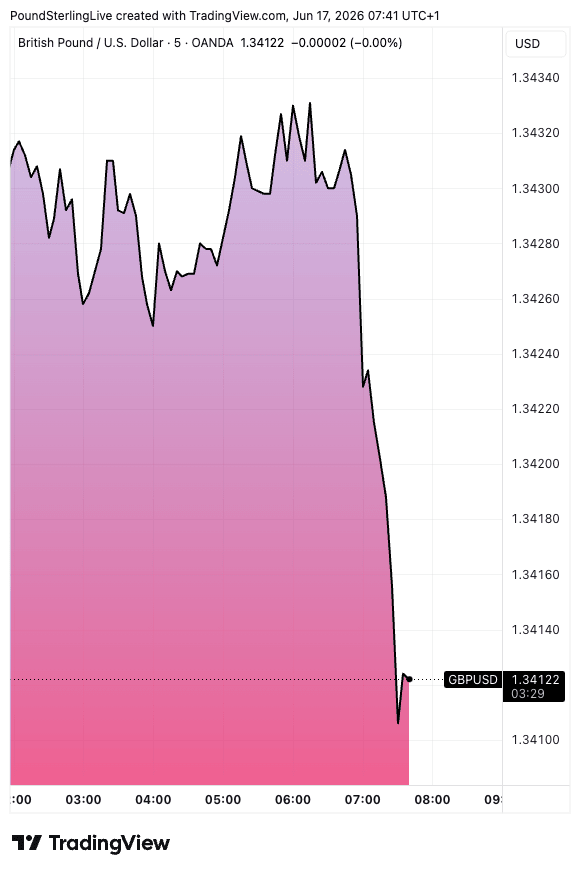

There was a discernible reaction across the sterling strip: the pound-to-dollar exchange rate fell to 1.3415 from 1.3430, and the pound-to-euro pairing fell to 1.1559 from 1.1565.

That confirms the market's initial reaction is that inflation trends are consistent with a growing belief the Bank of England won't be required to raise interest rates in response to the Middle East conflict.

"Altogether, the sting from the Iran conflict looks less than markets initially assumed. The peak in CPI could end up well below what we saw last year. This could give the BoE some pause for thought. Indeed, it could buy the MPC more time to assess the risks around so-called second round effects," says Sanjay Raja, Chief UK Economist at Deutsche Bank.

However, there's one segment of the data that could yet cause some caution on the MPC: services inflation jumped from 3.2% to 3.7%.

That's a sizeable increase that could have implications for the interest rate outlook because the Bank is particularly interested in what services inflation does: headline inflation won't durably fall to the 2.0% target unless services deflate.

Rising service numbers also hint that firms are responding to the energy shock by raising their own prices, something the Bank of England won't welcome.

The pound might have been even lower were it not for that services reading.

Nevertheless, there's enough evidence building that the inflationary shock caused by the war will land on the lower end of estimates, much to the relief of households and businesses, although it's disappointing for those wanting a stronger pound.

"MPC hawks are still likely to point to long lags in pass-through, and with the PPI input price index rising 8.7% y/y it is obviously the case that pipeline cost pressures are elevated. But for now the combination of wholesale energy prices falling in response to the US-Iran deal alongside downside CPI outturns versus forecast looks likely to embolden Bailey with his existing strategy of holding off rate hikes," says Sam Hill, Head of Market Insights at Lloyds Bank.

The Bank will also note the recent sharp fall in oil and gas prices due to building hopes the Strait of Hormuz will reopen to shipping as early as Friday.

A decline in energy prices could herald a more forceful disinflation trend that could allow discussions of Bank of England rate cuts to re-enter the conversation.

For the pound, that resets us to where we were prior to the Iran conflict: the charts show GBP/EUR trended in the late-1.14s and GBP/USD towards 1.32.

That's not a forecast, rather it's a reminder that falling interest rate expectations tend to correlate with a lower pound, particularly when the market senses the Bank of England has more cutting to do than the rest.

That's a line of thinking that could re-emerge in H2.

GBP Front-running the Bank's Thursday Decision

The pound's weakness post-inflation release could well be the foreign exchange market resetting levels ahead of Thursday's Bank of England decision.

Traders will read the data as being consistent with a 'dovish' decision and guidance; Huw Pill might find himself alone in voting for a hike and the Bank might emphasise with greater confidence that holding rates is optimal in light of the data and developments in the Middle East.

That would look like a central bank moving away from a potential 'insurance' hike, and it would allow it to more easily slip back into guiding towards rate cuts later in the year.

For the pound, that would pose a headwind, and we're seeing the adjustment happen ahead of the decision: if the falls happen today, Thursday's market moves might be more subdued.