Image © Adobe Images

The British pound suffered a setback Tuesday after data show the UK economy struggling this June.

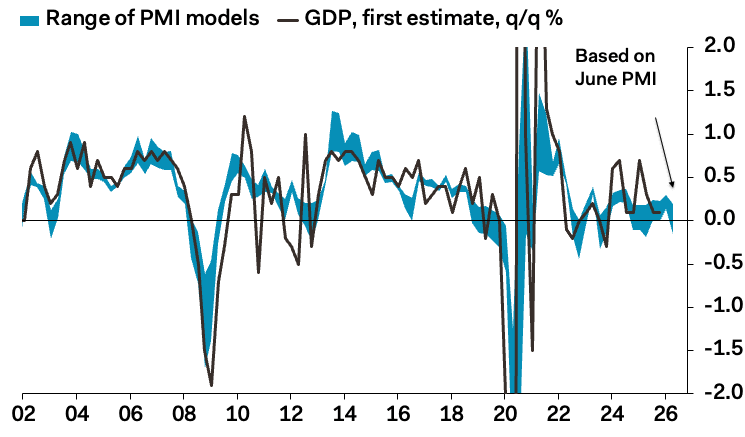

June's PMI survey data undershot expectations and indicated that the economy contracted for a second consecutive month.

S&P Global's services PMI fell to 48.7 from 49.3 in May, undershooting expectations for a recovery into growth territory at 50.1. Manufacturing is still growing, although the result of 53.1 undershot expectations for 53.5.

The composite PMI - which balances the data to give a representative reading of the wider economy - came in at 49.4, down from 49.7 and below the 50.6 estimate.

A PMI below 50 indicates contraction.

"A disappointing June ‘flash’ PMI indicates that the economy contracted for a second successive month, albeit at only a 0.1% rate and merely flat-lining over the second quarter as a whole," says Chris Williamson, Chief Business Economist at S&P Global Market Intelligence.

According to Pantheon Macroeconomics, translating the PMI into a growth forecast indicates that June's PMI in isolation is consistent with quarter-to-quarter GDP growth of 0.1% in Q2, down from 0.5% in Q1.

On paper, this disappointment should present a headwind for the pound, and there was a tick lower in both GBP/USD and GBP/EUR following the releae of the numbers, although the move is relatively contained, suggesting sterling has its eyes on political developments.

Indeed, politics will be important for the economy going forward: does the removal of Keir Starmer and the ascendency of Andy Burnham turn business and household confidence for the better?

Or does Burnham reach for the tax and borrowing lever to pursue his policy aims, thereby stifling the public sector?

These are the relevant questions for the economy and pound going forward, which might suggest the pound sees today's PMI numbers as being dated, even if they are the most timely of the major monthly economic prints.

Implications for Interest Rates

The PMI report found inflationary pressures are elevated, with businesses saying the energy shock and supply squeeze from the war in the Middle East are exacerbating existing cost pressures from government policies.

"These higher costs, combined with subdued business growth expectations for the year ahead, have caused employment to continue to fall at a worryingly high rate," says Williamson.

This underscores the dilemma facing the Bank of England: on one hand, inflationary pressures are set to stay uncomfortably high, but on the other, the employment situation continues to deteriorate, which can be partly remedied with lower interest rates.

The competing forces should encourage the Bank to maintain interest rates at current levels, which means current market expectations for a hike can recede.

If that's the case, the pound will find interest rate expectations could prove a headwind.

"The PMI's signal of slowing growth and sticky price pressures supports our call that rates will remain on hold this year, rather than hiked once as the market is currently expecting," says Rob Wood, Chief UK Economist at Pantheon Macroeconomics.