Image © Adobe Images

There's a big technical challenge underway in GBP/NZD.

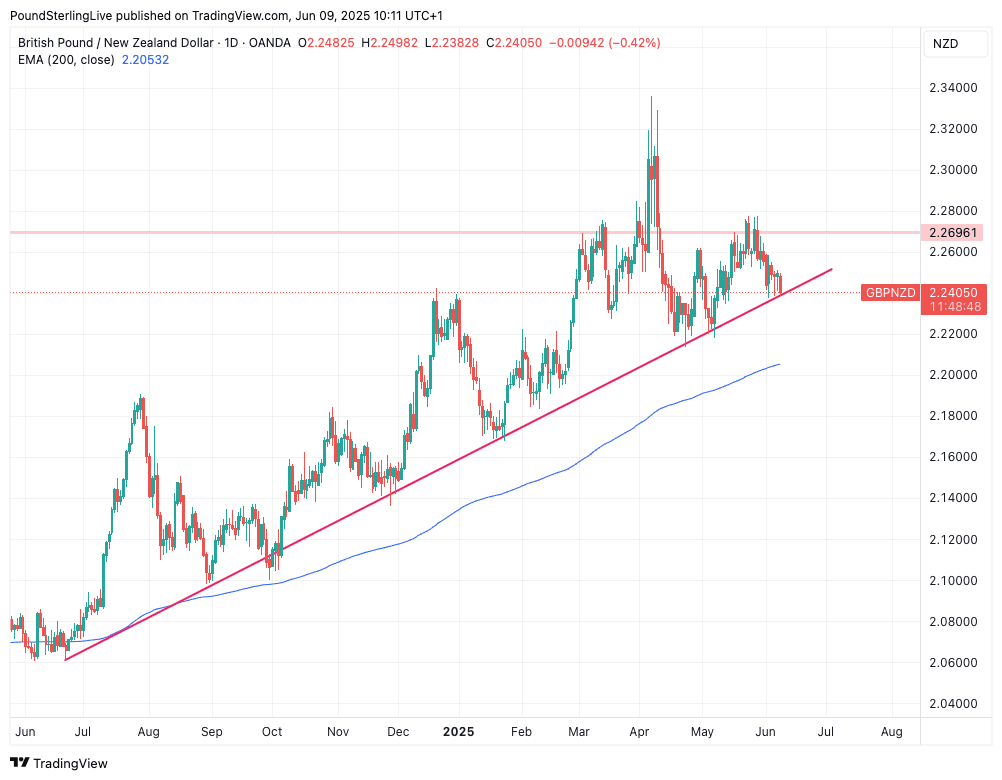

The Pound to New Zealand Dollar exchange rate (GBP/NZD) tests is testing a critical support line that must hold if we are to retain the view that the pair retains an upward bias.

It is that bias that saw the market go as high as 2.31 in April, the strongest level for UK-based Kiwi buyers since prior to the Brexit referendum of 2016.

The inevitable pullback from those highs has been the story since April 09, but we are now at a point where the pullback risks morphing into the confirmation of a more enduring top in GBP/NZD.

Above: GBP/NZD at daily intervals.

A look at the chart shows a multi-month uptrend defined by the red line, which has offered rock-solid support in previous instances of weakness.

We would view a break through and below this line as a signal that a summer of weakness is to ensue for GBP/NZD. We have also placed the 200-day exponential moving average on the daily chart, given that it too has provided solid support.

So a break through the trendline could still see the pair revert to the more solid support of the 200-day EMA.

Only once below the 200-day would we officially call an end to the multi-year uptrend and the start of a downtrend.

We are some way from this point, but it does feel like NZD buyers aren't favoured in the near-term.

It's a quiet week in New Zealand, but UK data is back in focus this week, and Pound Sterling could be bolstered by Tuesday's labour market report that should show wages continue to rise at a clip, meaning inflation will stay elevated over the coming months.

The consensus looks for the two ONS measures of wages to read at 5.5% in April, implying little change from March. Anything above this would be considered inflationary (high wages = higher prices charged by businesses and higher domestic demand, both of which put pressure on prices).

On balance, this should bolster UK bond yields and the Pound.

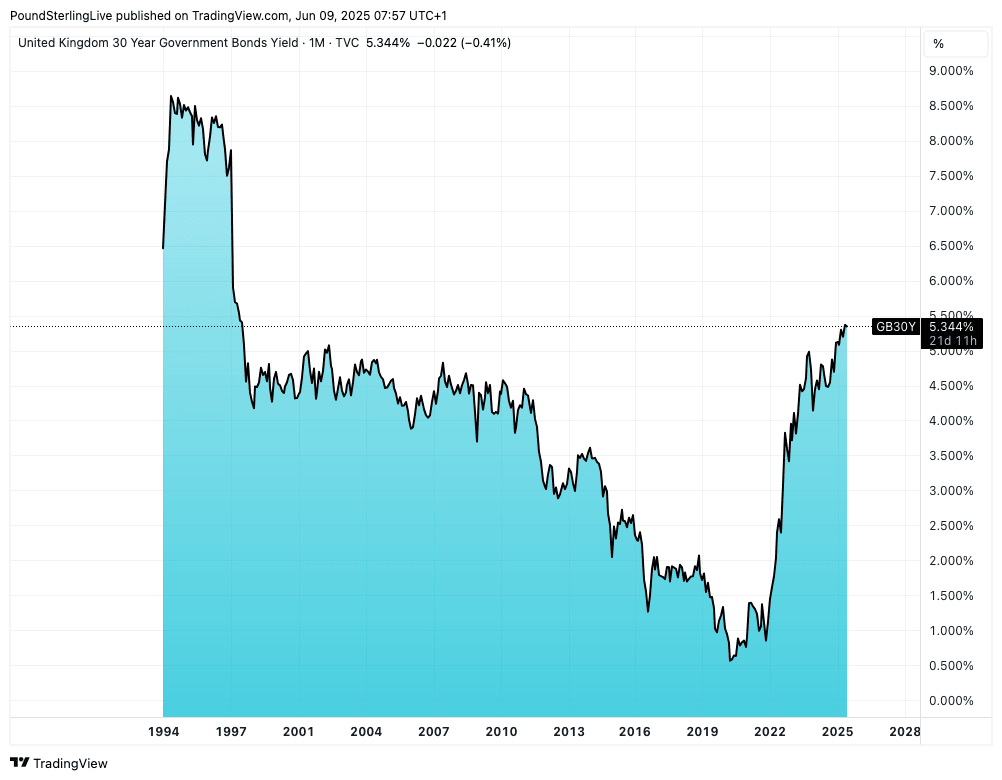

The critical interplay between the Pound and bond yields comes into sharper focus on Wednesday when UK Chancellor Rachel Reeves presents the government's spending settlements for the coming three years in the Spending Review.

Above: Long-term UK borrowing costs are now at their highest level since 1998. Shown: the UK 30-year bond yield.

This is not a budget, and taxes will therefore not be changed. However, it will be a test of credibility for the government, in which markets must remain convinced the UK's debt dynamics remain sustainable.

If doubts grow, UK bond yields risk rallying as investors demand greater compensation for buying and holding long-term UK debt. (A bond is what the government issues when it borrows. The yield is the 'interest rate' the bond pays investors. Higher yields imply investors want a bigger payoff for holding that debt, usually to account for inflation and any fears about the future sustainability of domestic finances).

Typically, the Pound tracks UK yields higher, as foreign investors snap up the higher returns that the UK offers. But, in times of elevated uncertainty (think Liz Truss), yields and the Pound go separate ways, potentially signalling a broader confidence crisis in the UK.

We think the odds of such a negative outcome happening this week are low, which means the Pound should easily navigate Wednesday. However, the warning to readers is that any mishaps by Reeves will be severely punished by the market, which would leave the GBP/NZD exchange rate at risk of a deep pullback.